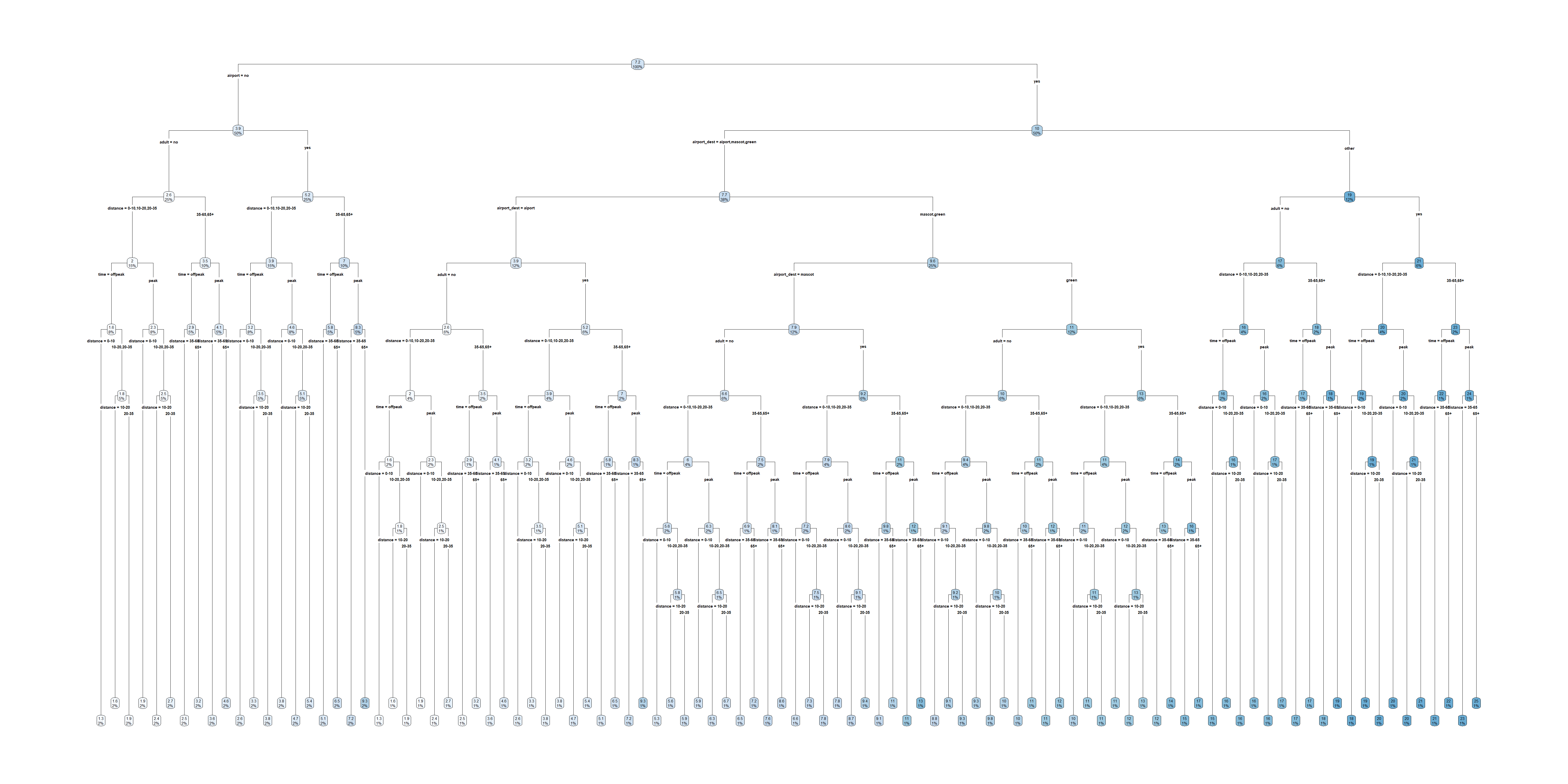

graph TB

A{Is it peak hour?}

A-->|Yes| B[Peak Hour]

A-->|No| C[Off-Peak Hour]

B--> D{Distance?}

D-->|0 - 10 km| E[$3.79]

D-->|10 - 20 km| F[$4.71]

D-->|20 - 35 km| G[$5.42]

D-->|35 - 65 km| H[$7.24]

D-->|65+ km| I[$9.31]

C--> J{Distance?}

J-->|0 - 10 km| K[$2.65]

J-->|10 - 20 km| L[$3.29]

J-->|20 - 35 km| M[$3.79]

J-->|35 - 65 km| N[$5.06]

J-->|65+ km| O[$6.51]

Tree-Based Methods

ACTL3142 & ACTL5110 Statistical Machine Learning for Risk Applications

Trees in a nutshell

Decision trees are a simple, easy to interpret, and popular method for both regression and classification tasks. They can be used to make predictions, but also simply as “data exploration” to understand a data set better.

They make predictions by partitioning the predictor space into a number of simple regions, and making a constant prediction within each region. The set of splitting rules can be summarised in a tree. “Stand alone” tree models are rarely particularly accurate, but they form the basis for more accurate (and complex) methods like random forests and boosting.

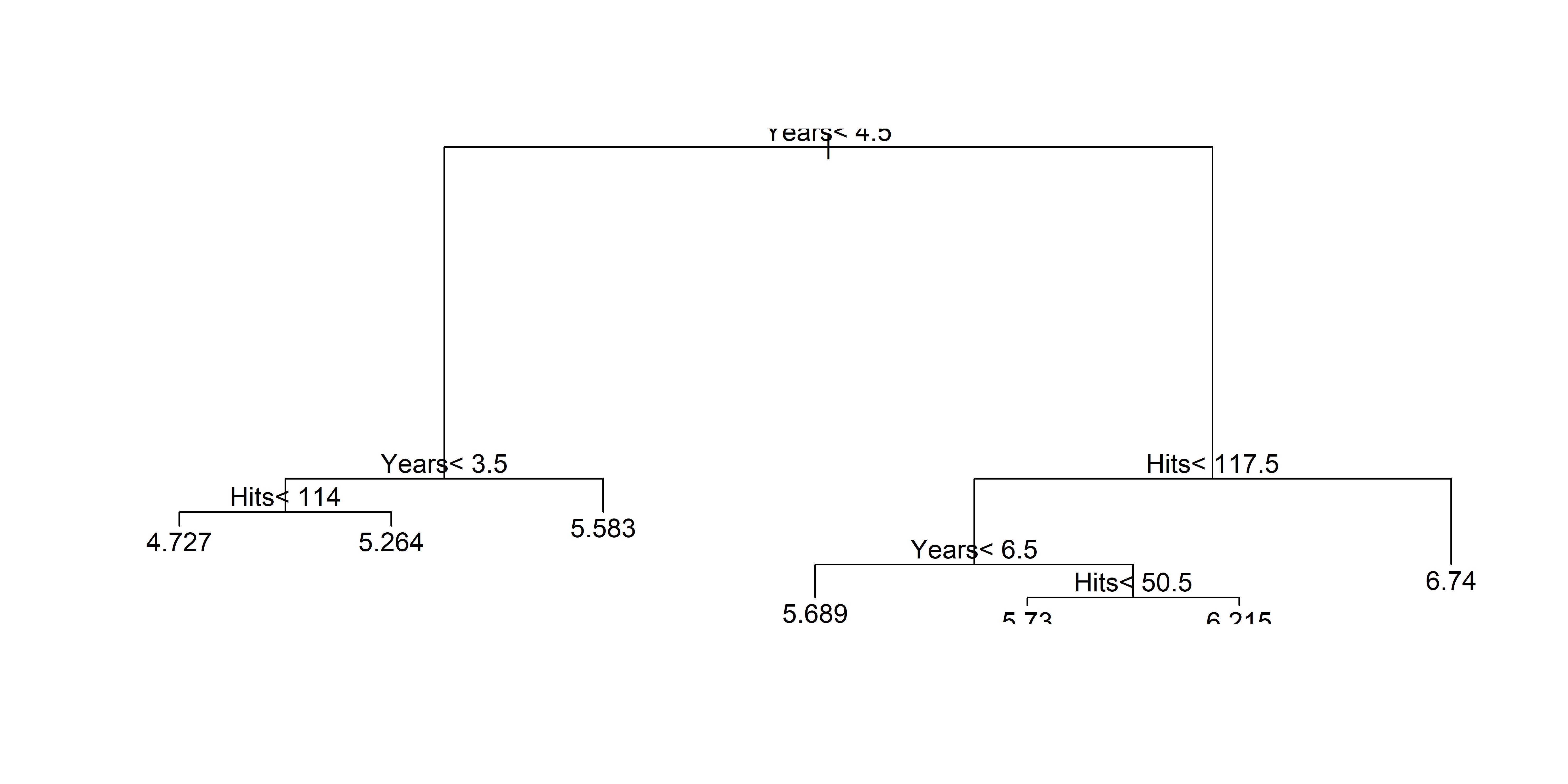

Fit a basic tree

n= 263

node), split, n, deviance, yval

* denotes terminal node

1) root 263 207.153700 5.927222

2) Years< 4.5 90 42.353170 5.106790

4) Years< 3.5 62 23.008670 4.891812

8) Hits< 114 43 17.145680 4.727386 *

9) Hits>=114 19 2.069451 5.263932 *

5) Years>=3.5 28 10.134390 5.582812 *

3) Years>=4.5 173 72.705310 6.354036

6) Hits< 117.5 90 28.093710 5.998380

12) Years< 6.5 26 7.237690 5.688925 *

13) Years>=6.5 64 17.354710 6.124096

26) Hits< 50.5 12 2.689439 5.730017 *

27) Hits>=50.5 52 12.371640 6.215037 *

7) Hits>=117.5 83 20.883070 6.739687 *

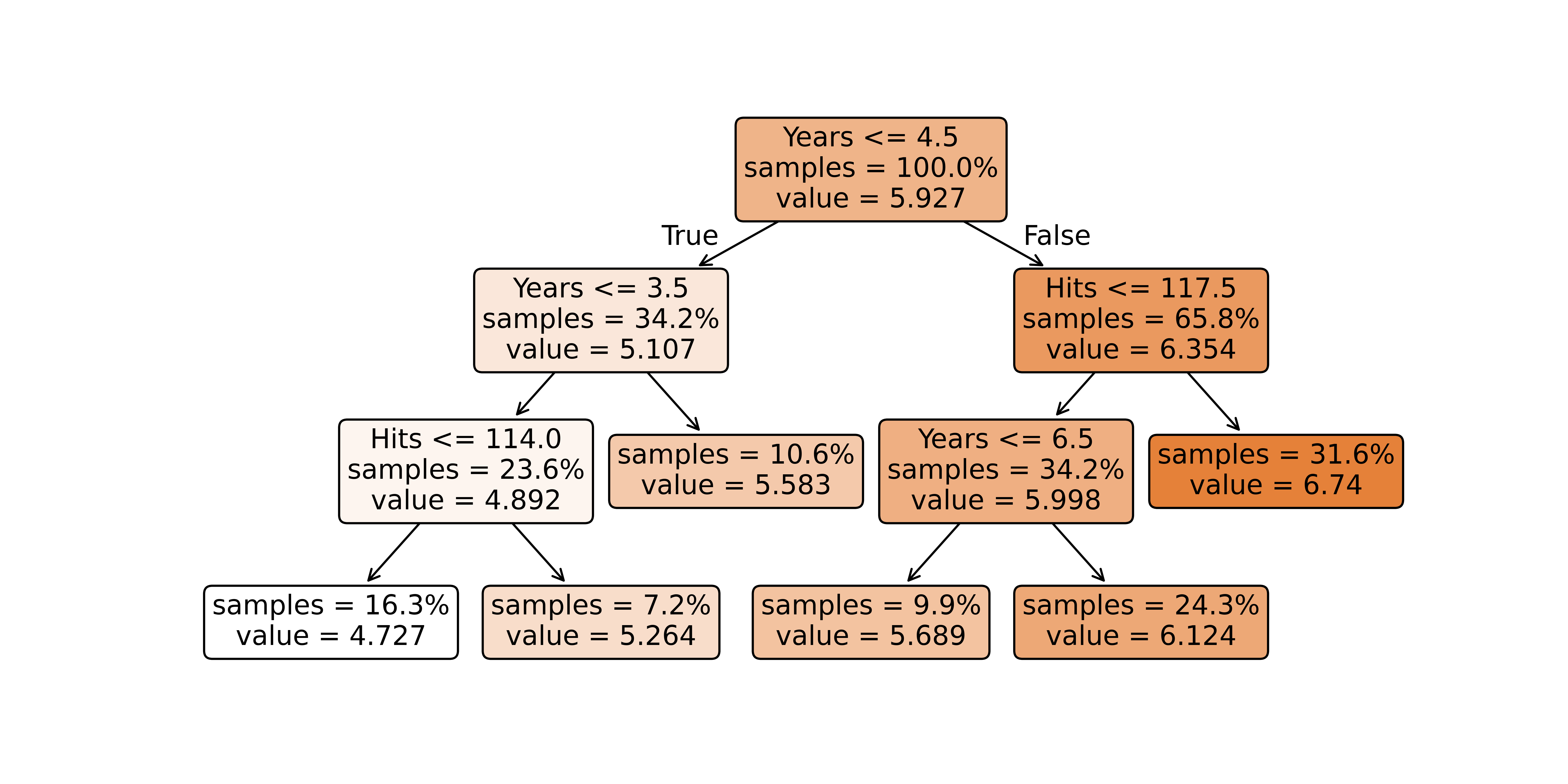

X = hitters[['Years', 'Hits']]

y = np.log(hitters['Salary'])

tree = DecisionTreeRegressor(min_samples_split=20, min_samples_leaf=10, max_depth=3, ccp_alpha=0.01)

tree.fit(X, y);

print(export_text(tree, feature_names=['Years', 'Hits']))|--- Years <= 4.50

| |--- Years <= 3.50

| | |--- Hits <= 114.00

| | | |--- value: [4.73]

| | |--- Hits > 114.00

| | | |--- value: [5.26]

| |--- Years > 3.50

| | |--- value: [5.58]

|--- Years > 4.50

| |--- Hits <= 117.50

| | |--- Years <= 6.50

| | | |--- value: [5.69]

| | |--- Years > 6.50

| | | |--- value: [6.12]

| |--- Hits > 117.50

| | |--- value: [6.74]Nicer plots for decision trees

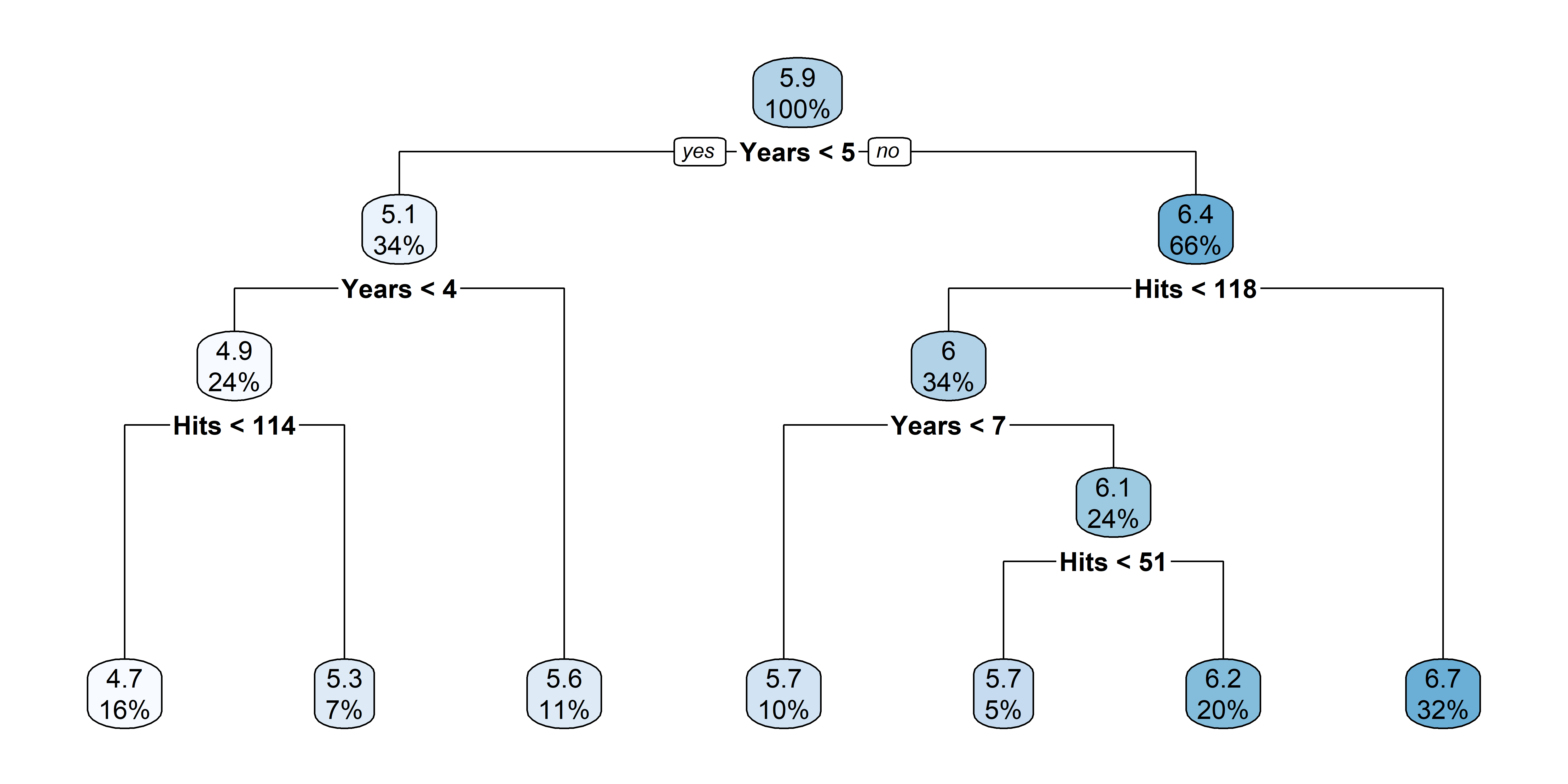

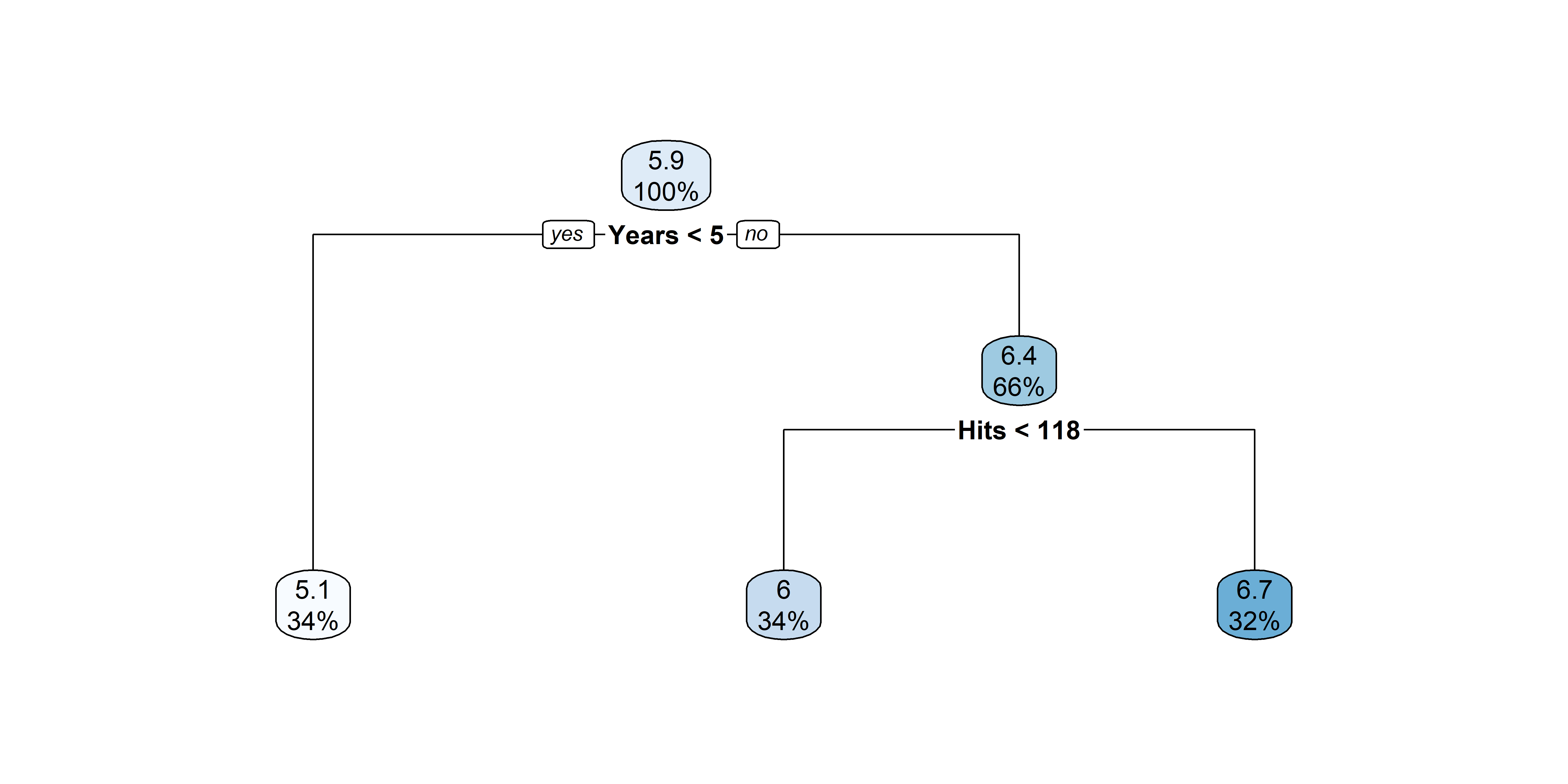

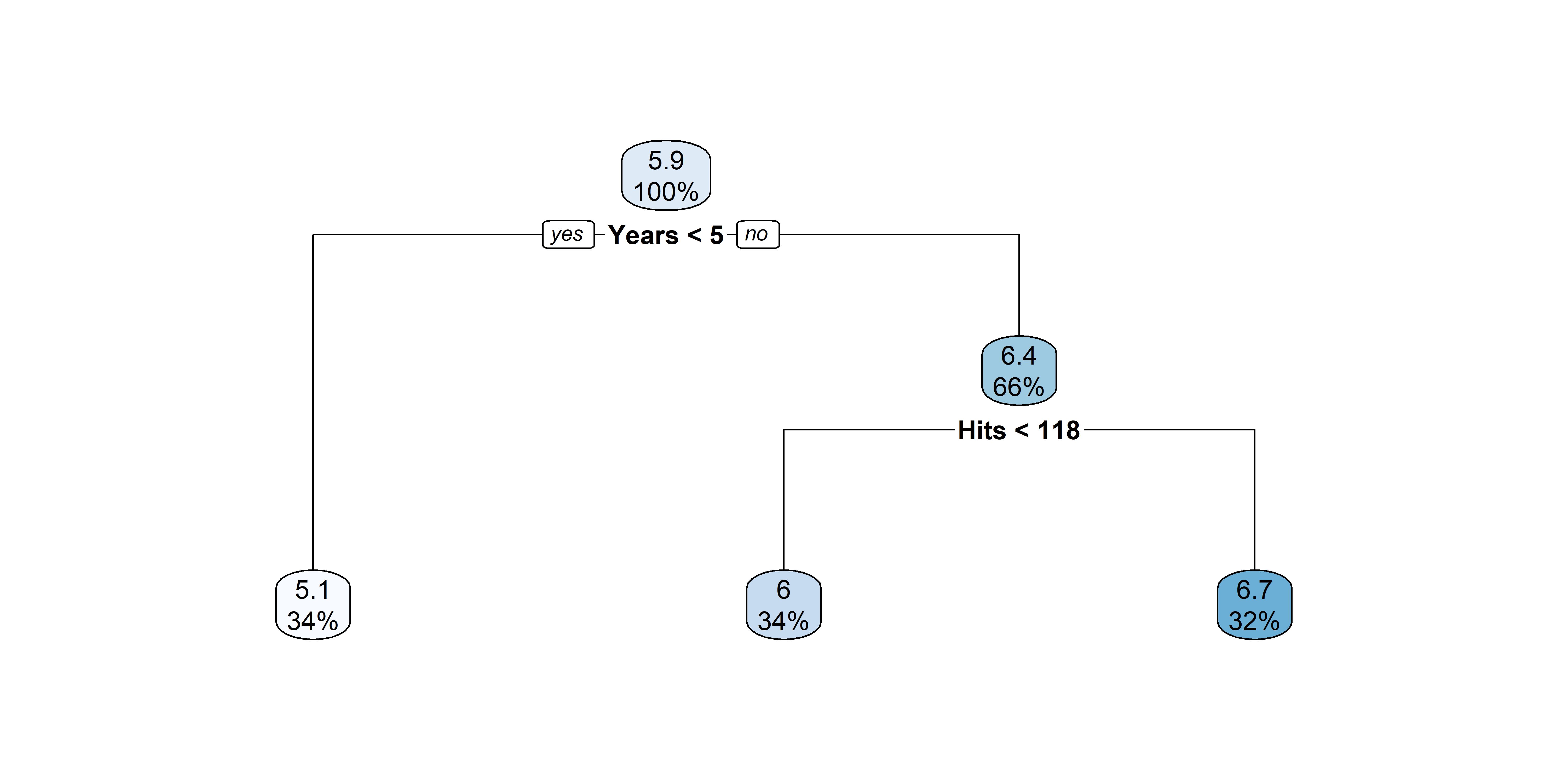

After pruning that tree

Tree Terminology

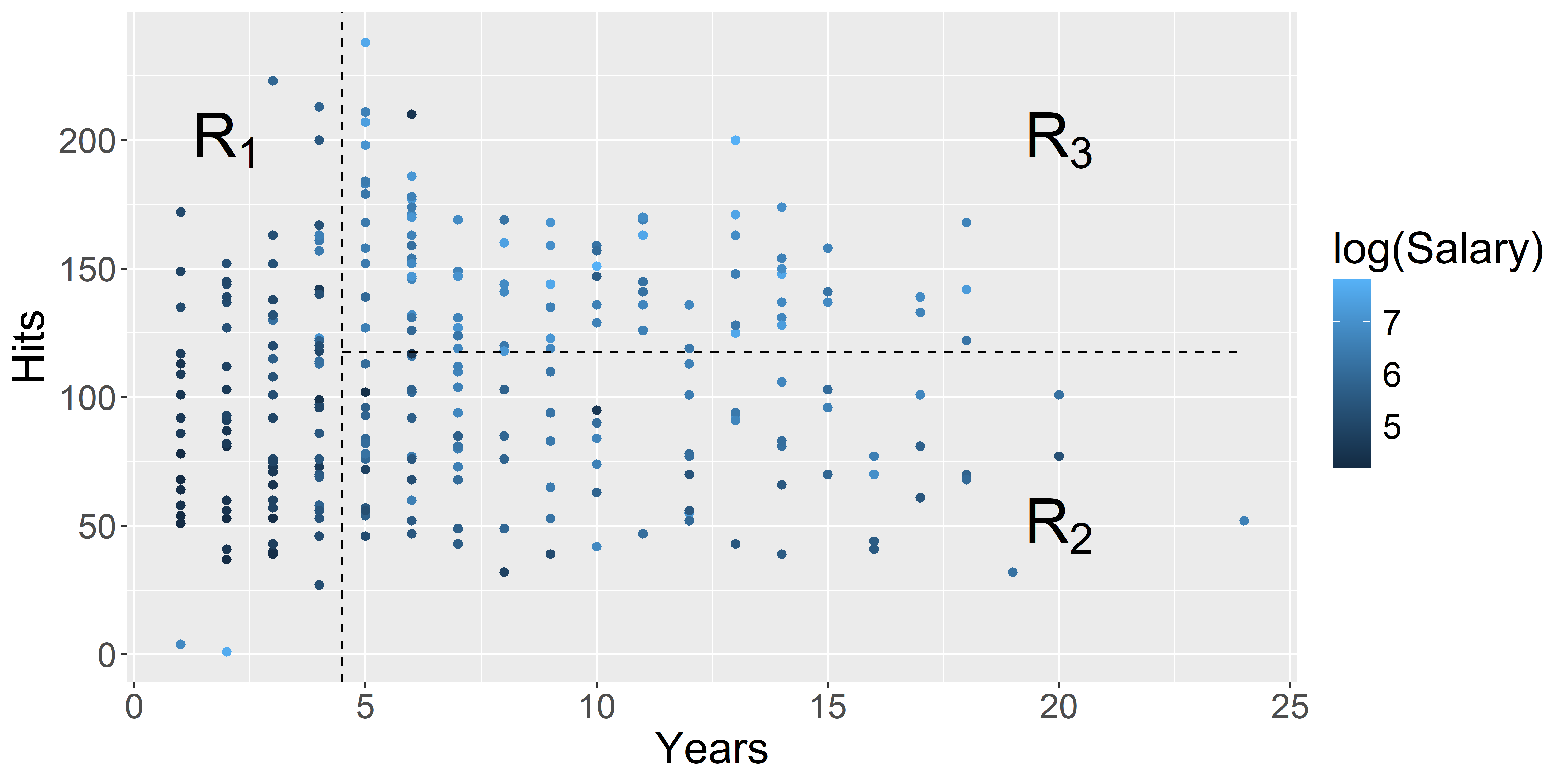

Regions in the predictor space

Code

ggplot(Hitters, aes(x = Years, y = Hits, colour = log(Salary))) +

geom_point() +

geom_vline(xintercept = 4.5, colour = "black", linetype = "dashed") +

annotate("segment", x = 4.5, xend = 24, y = 117.5, yend = 117.5, colour = "black", linetype = "dashed") +

annotate("text", x = 2, y = 200, label = "R[1]", parse = TRUE, size = 10) +

annotate("text", x = 20, y = 50, label = "R[2]", parse = TRUE, size = 10) +

annotate("text", x = 20, y = 200, label = "R[3]", parse = TRUE, size = 10) +

theme(text = element_text(size = 20))

Discussion

Decision trees: summary

- Decision trees are simple, popular, and easy to interpret.

- They are not the most accurate method, but they can be great to understand the data.

- They do form the basis for more accurate and complex methods like random forests and boosting.

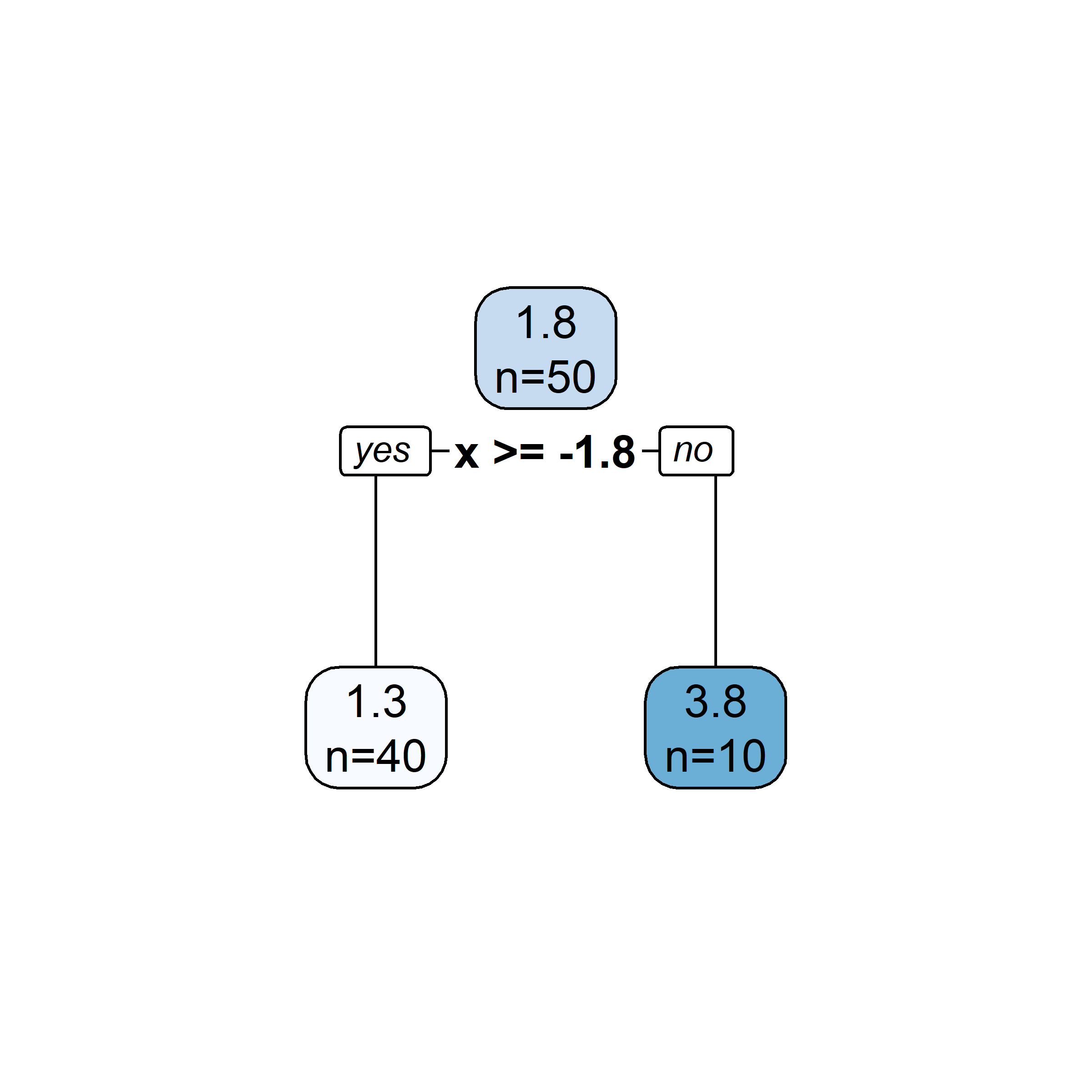

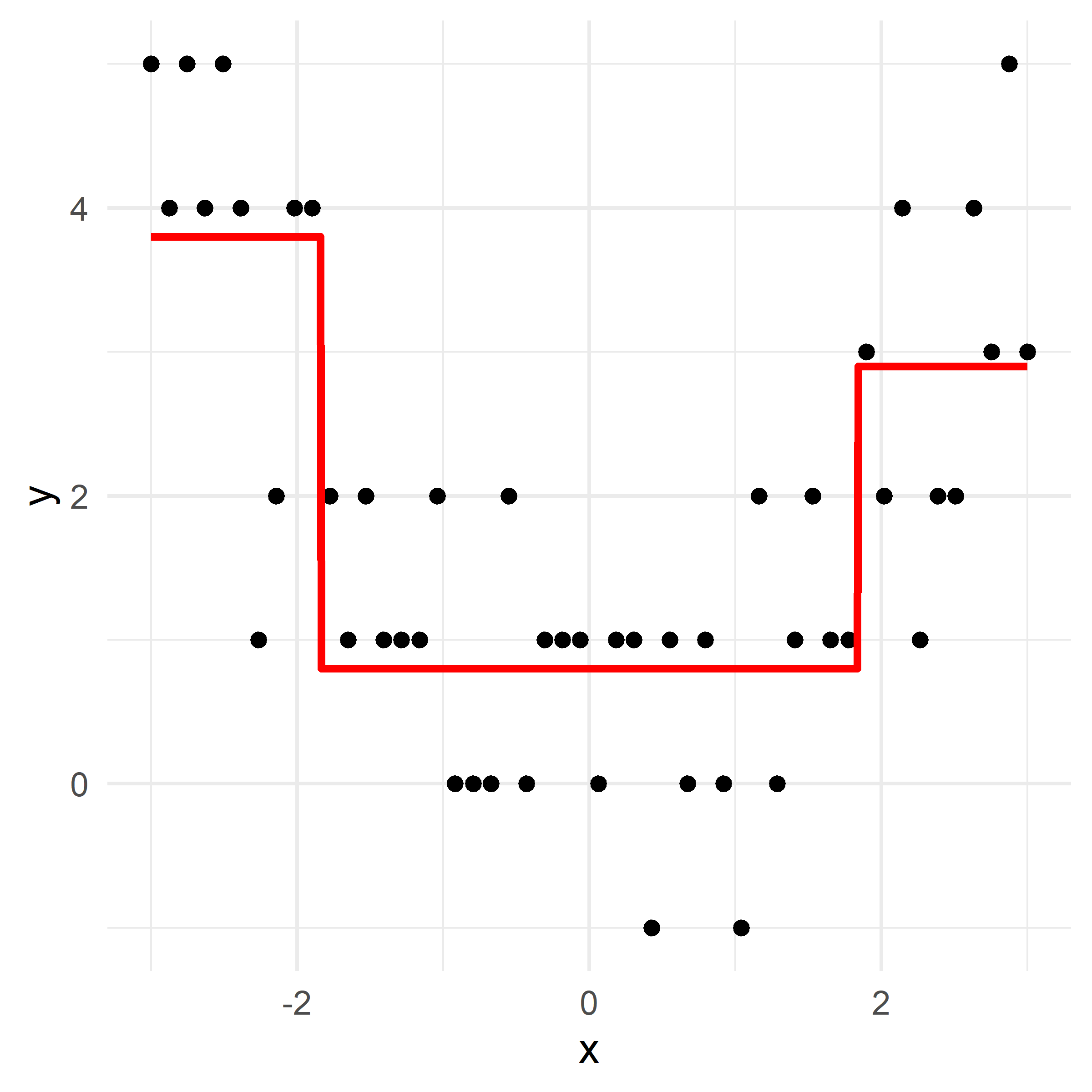

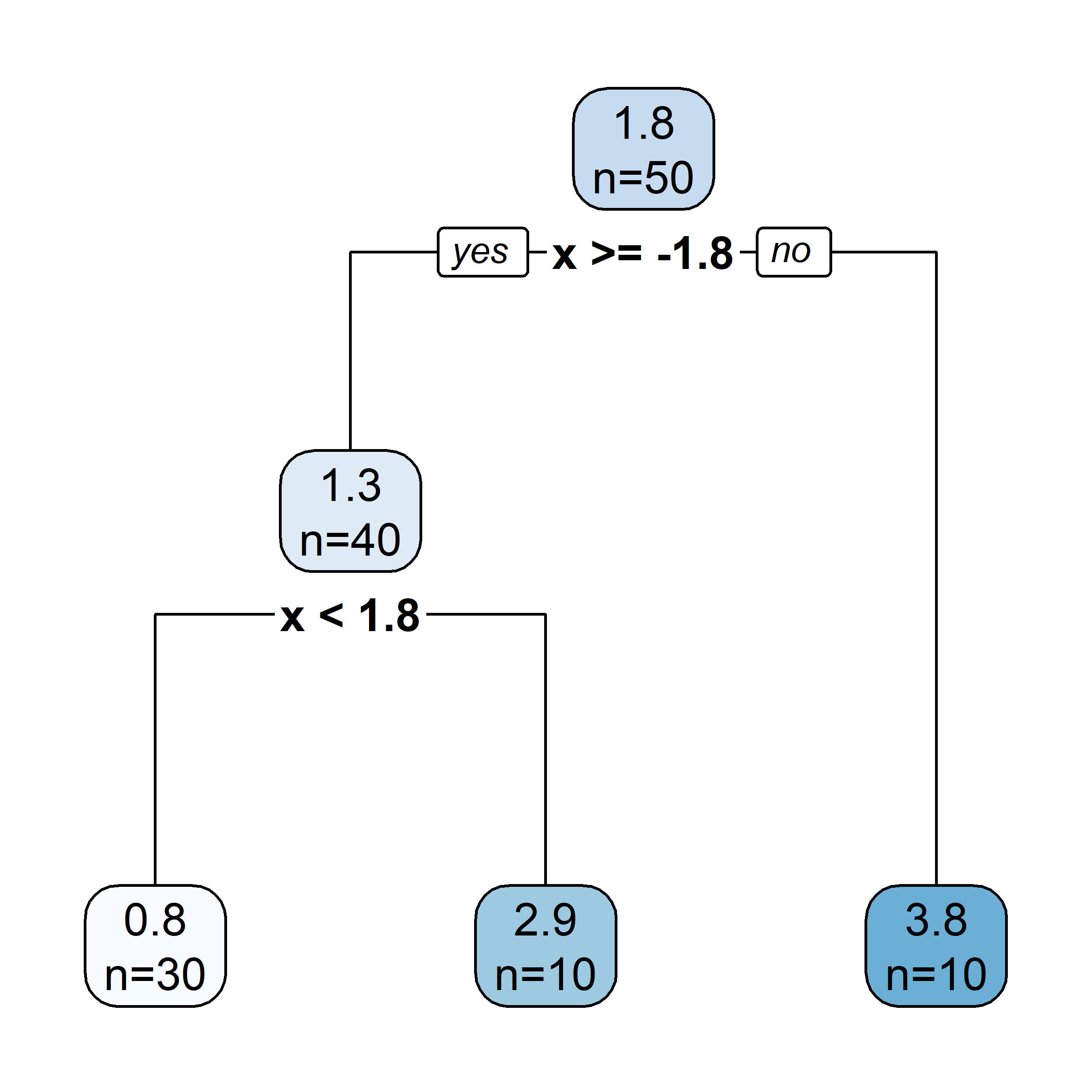

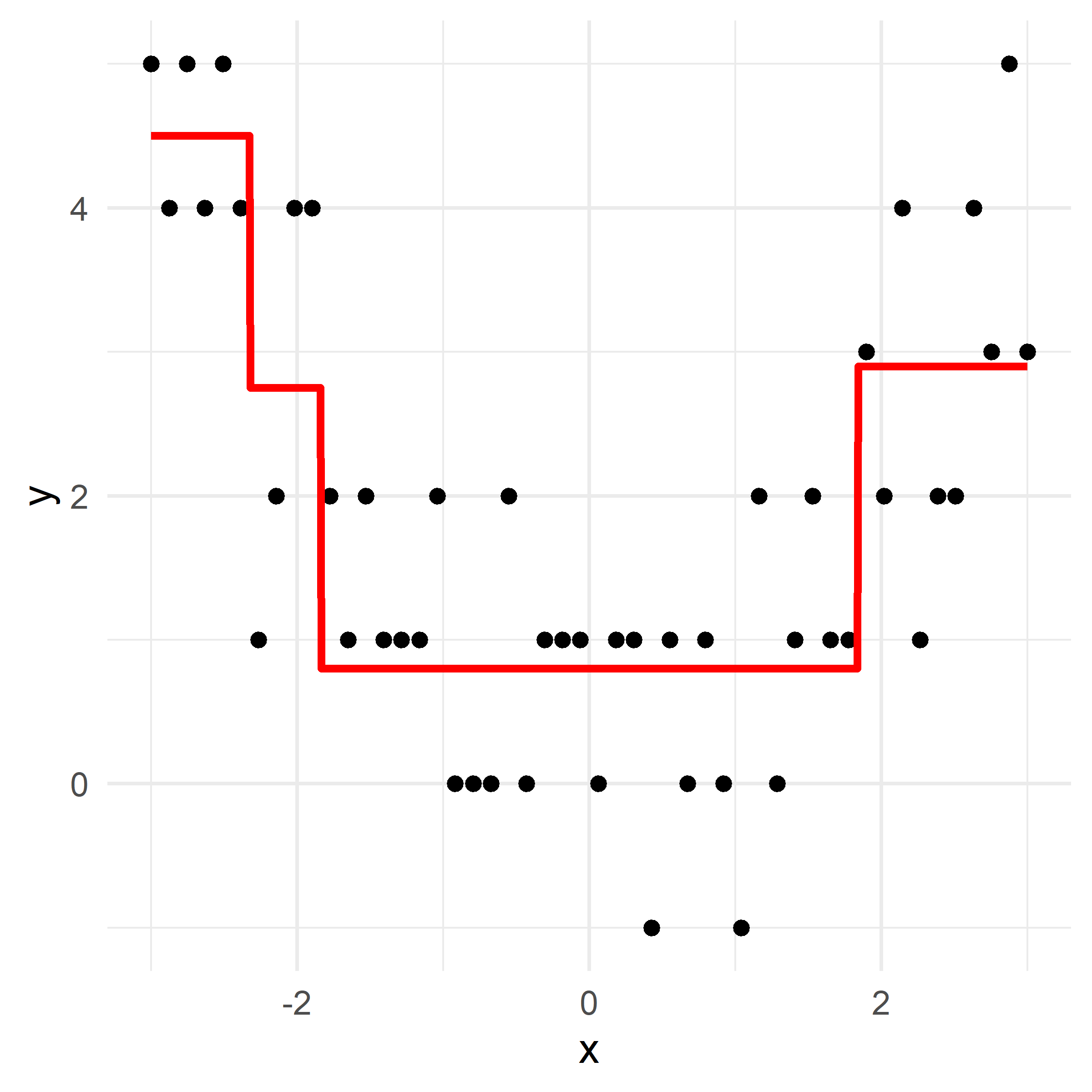

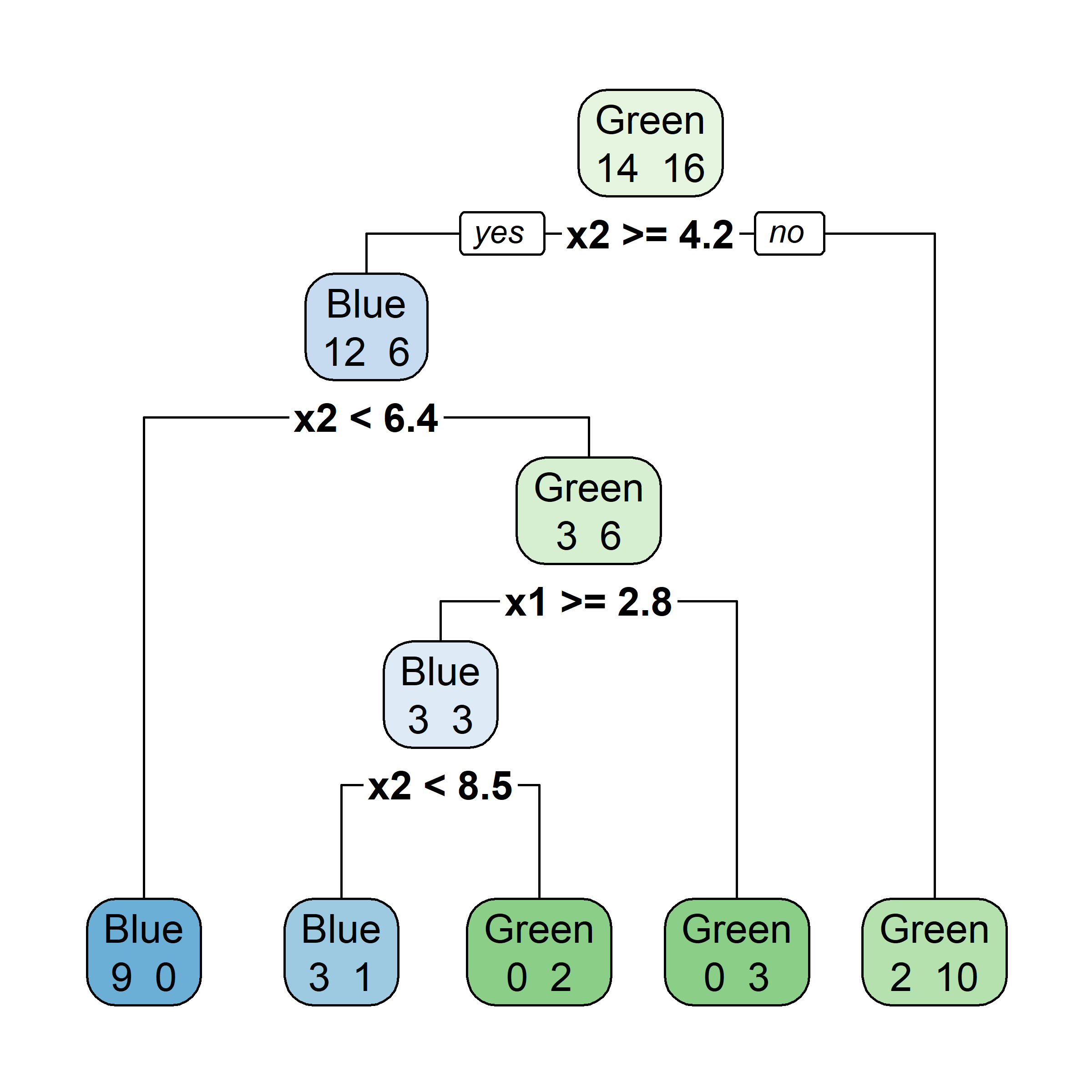

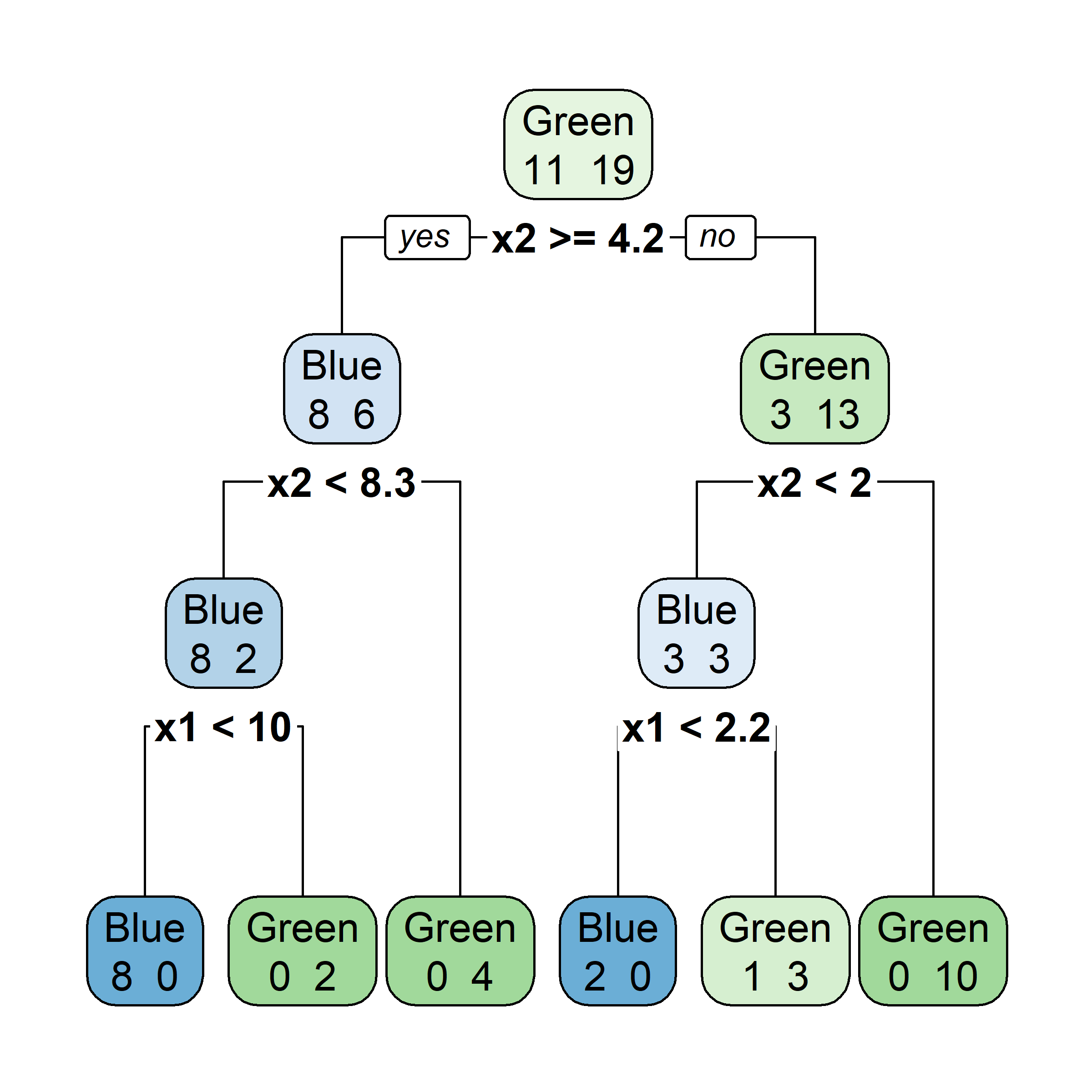

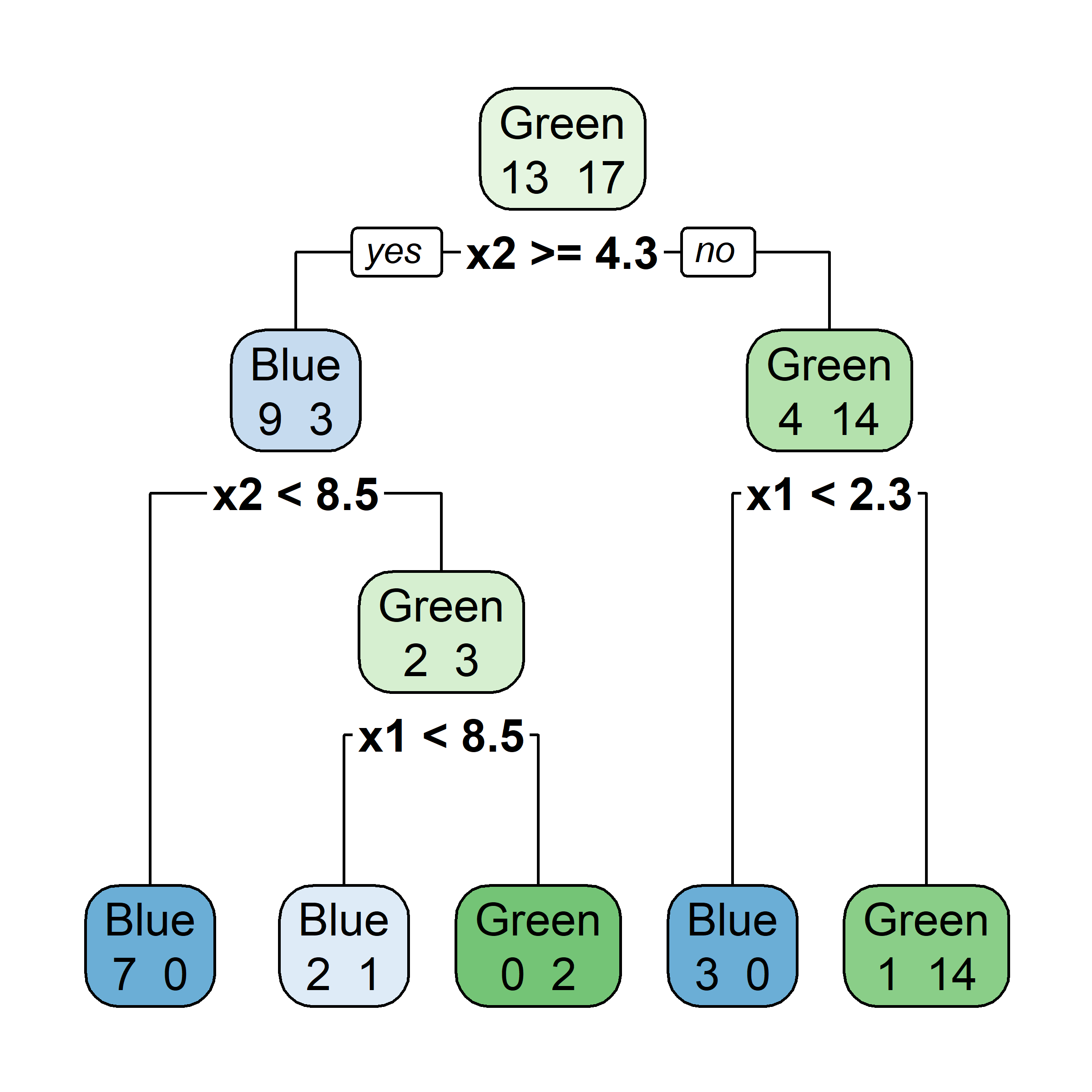

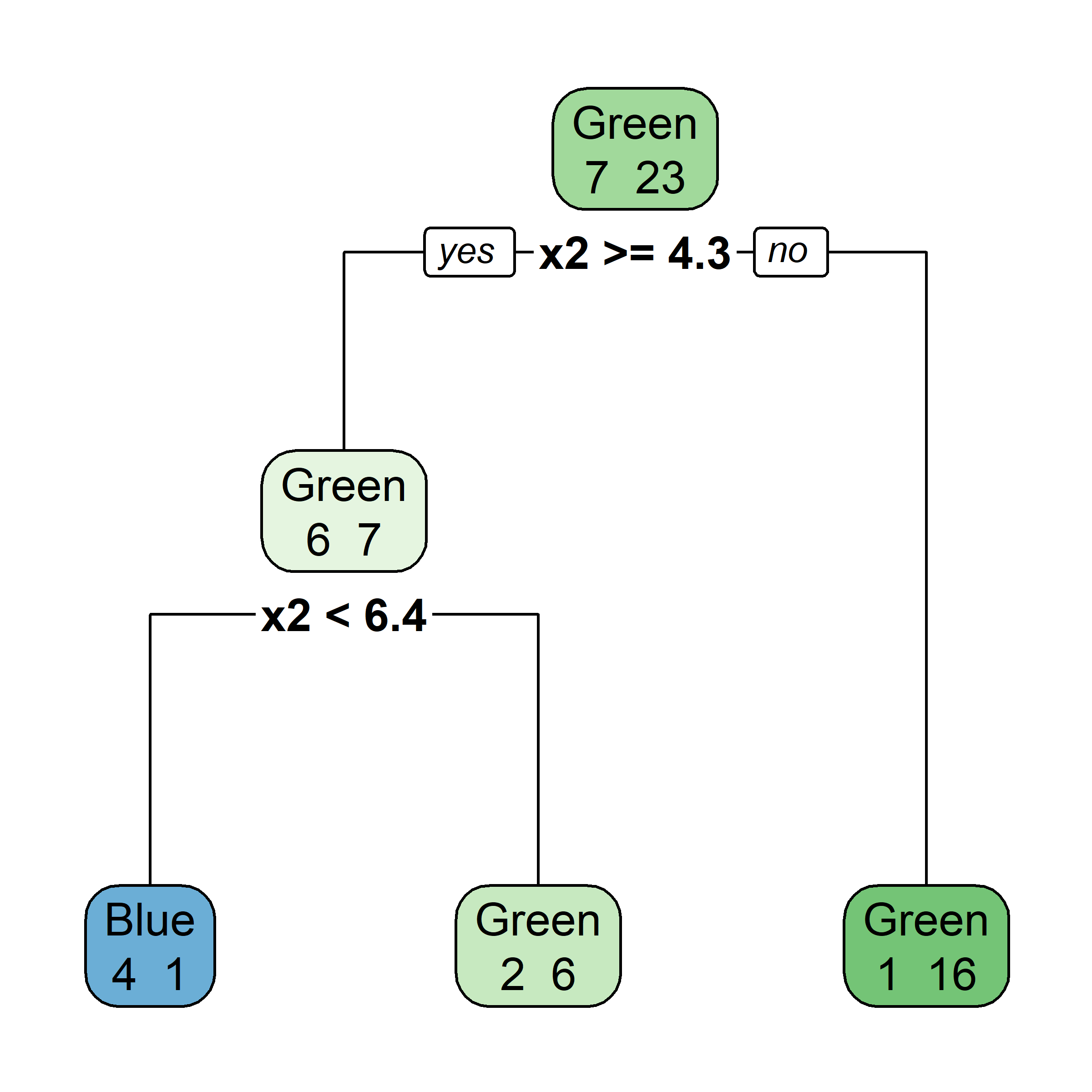

Illustraion with a synthetic regression dataset

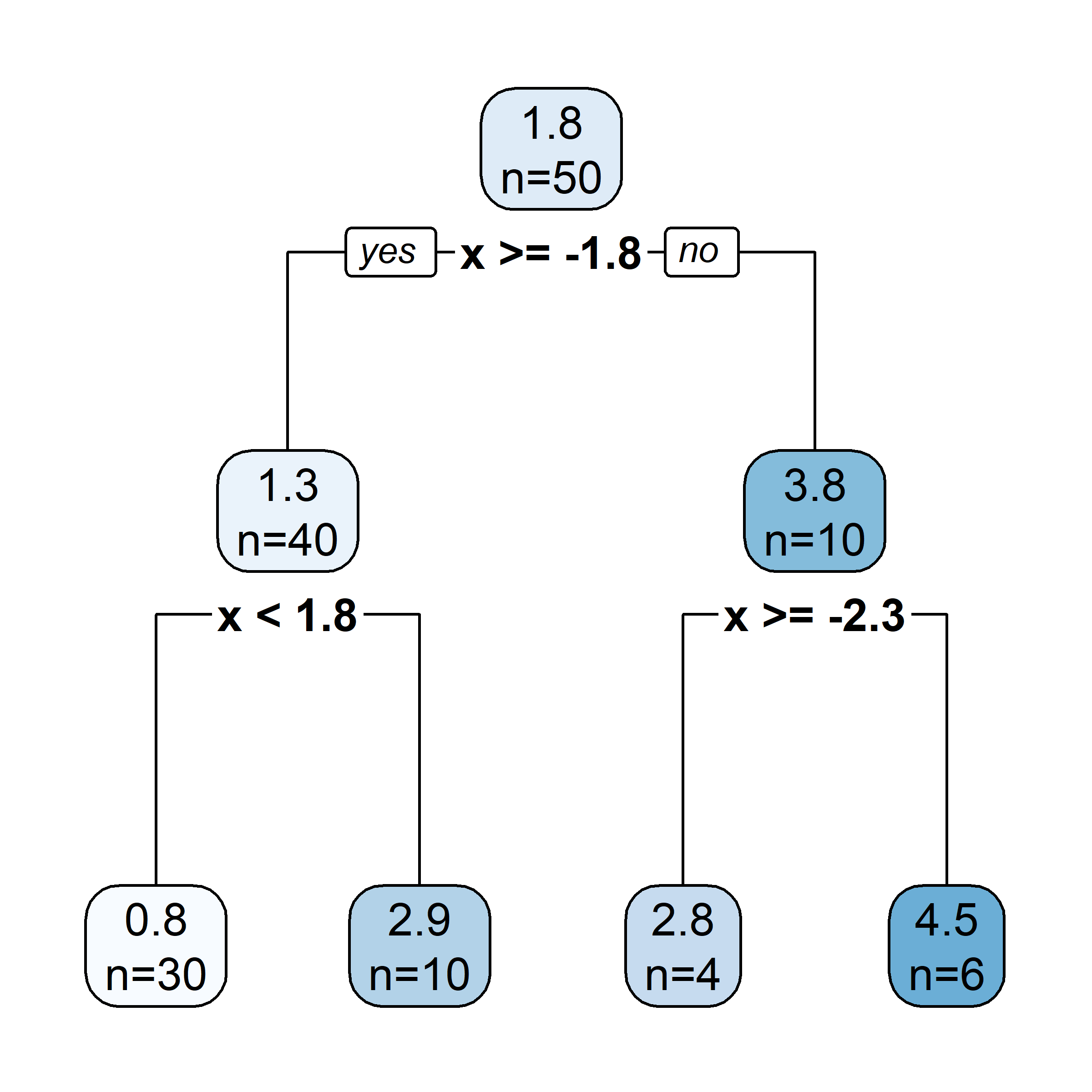

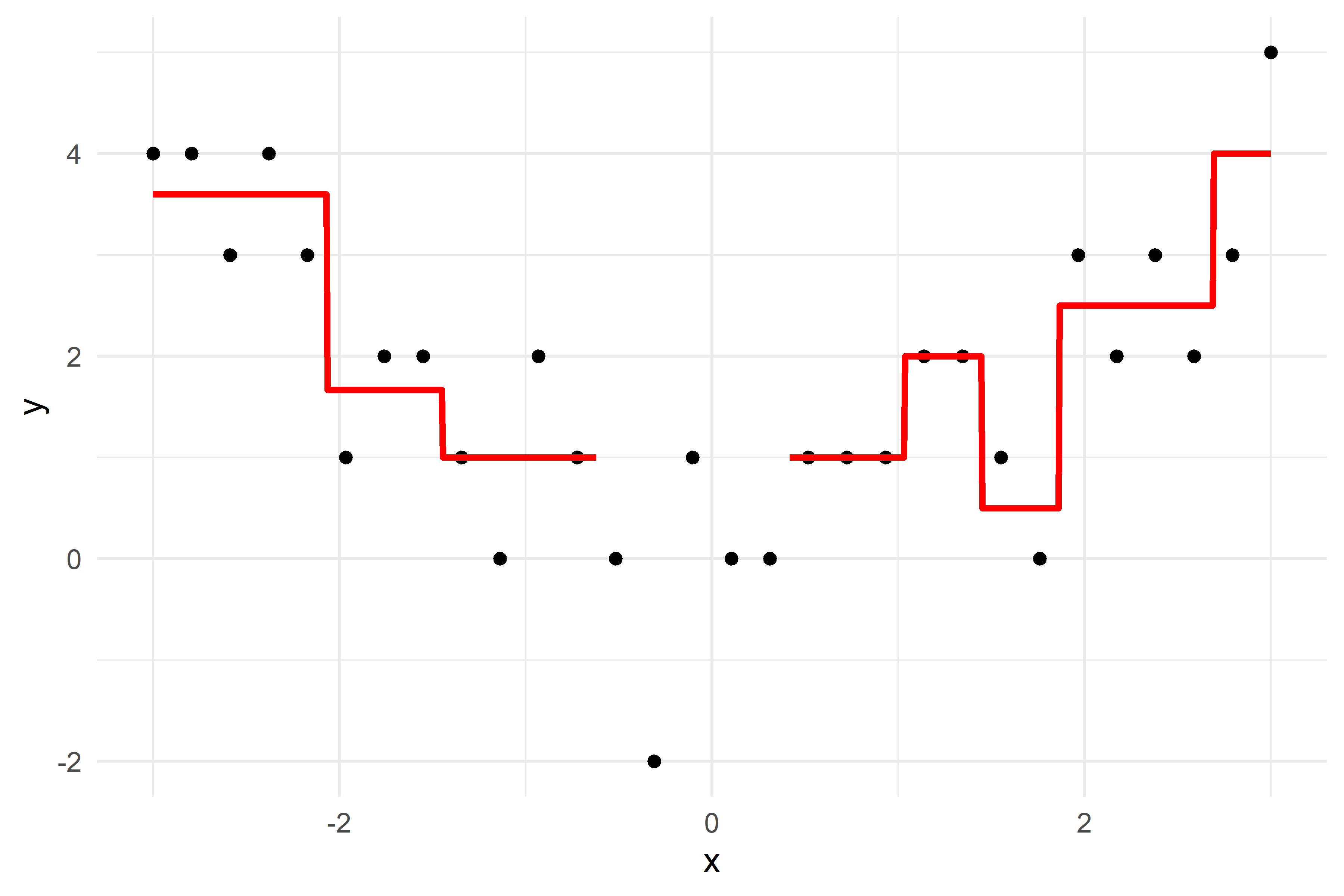

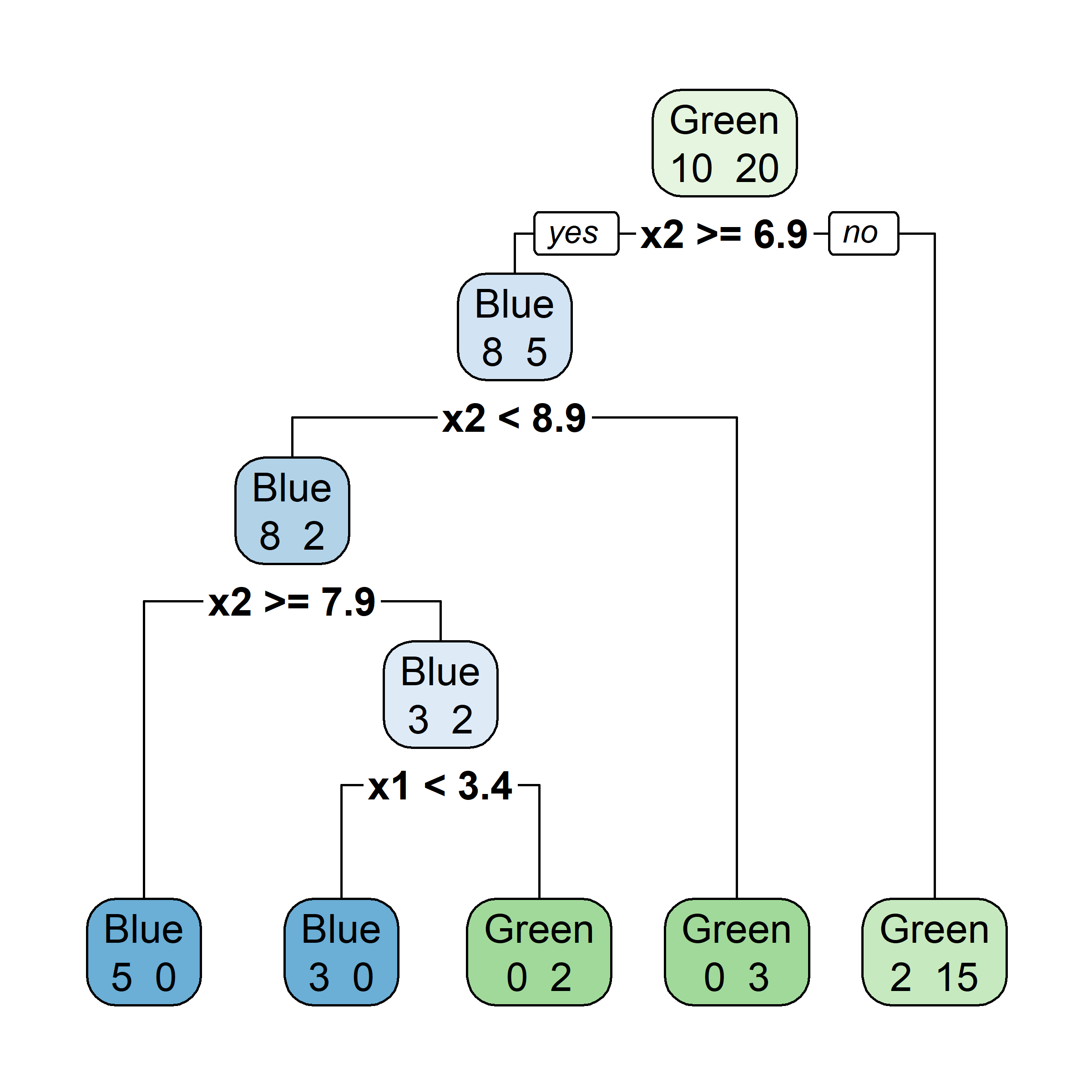

Growing a regression tree I

Growing a regression tree II

Growing a regression tree III

Growing a regression tree IV

2023 exam question

What would be the tree’s predicted value for y at x = 0?

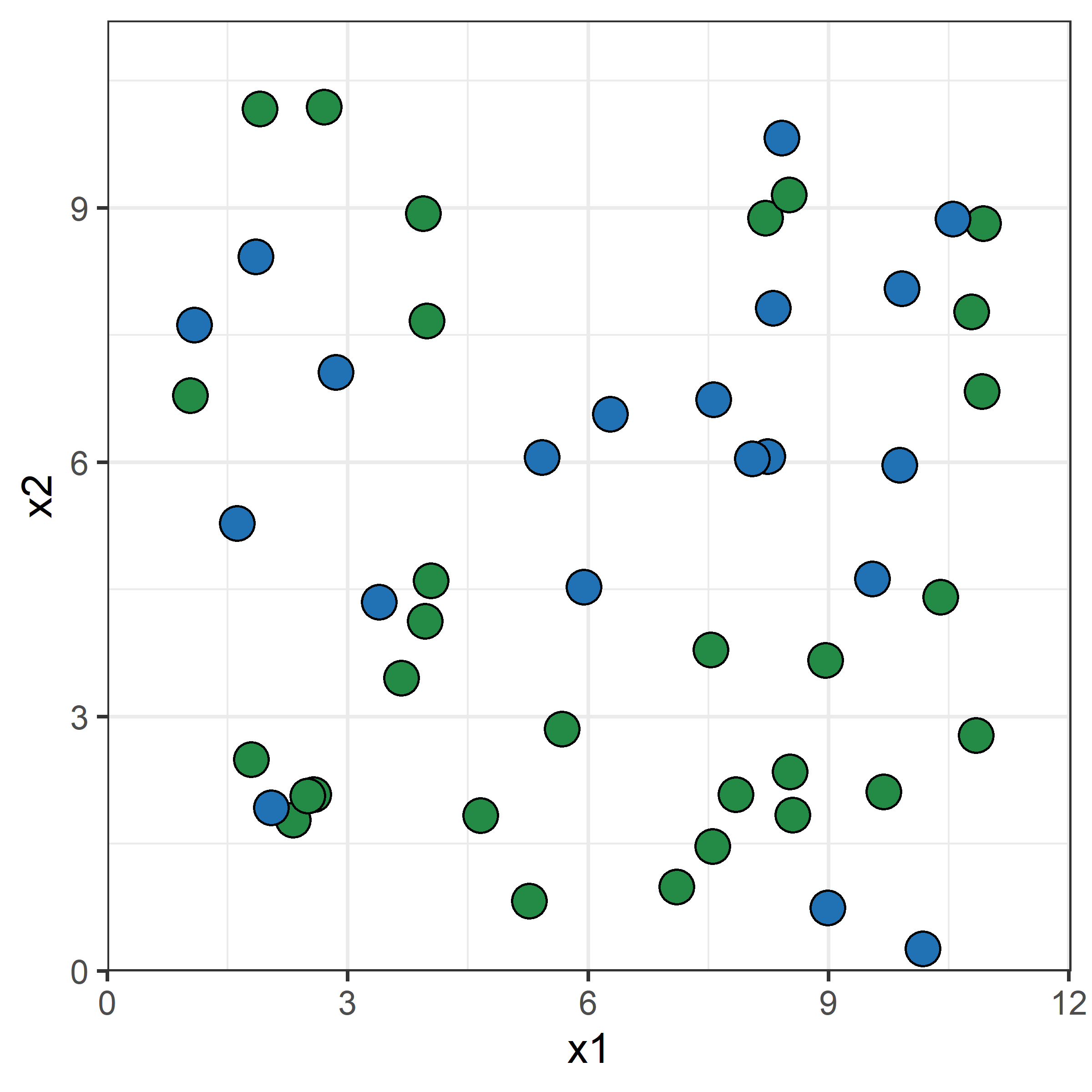

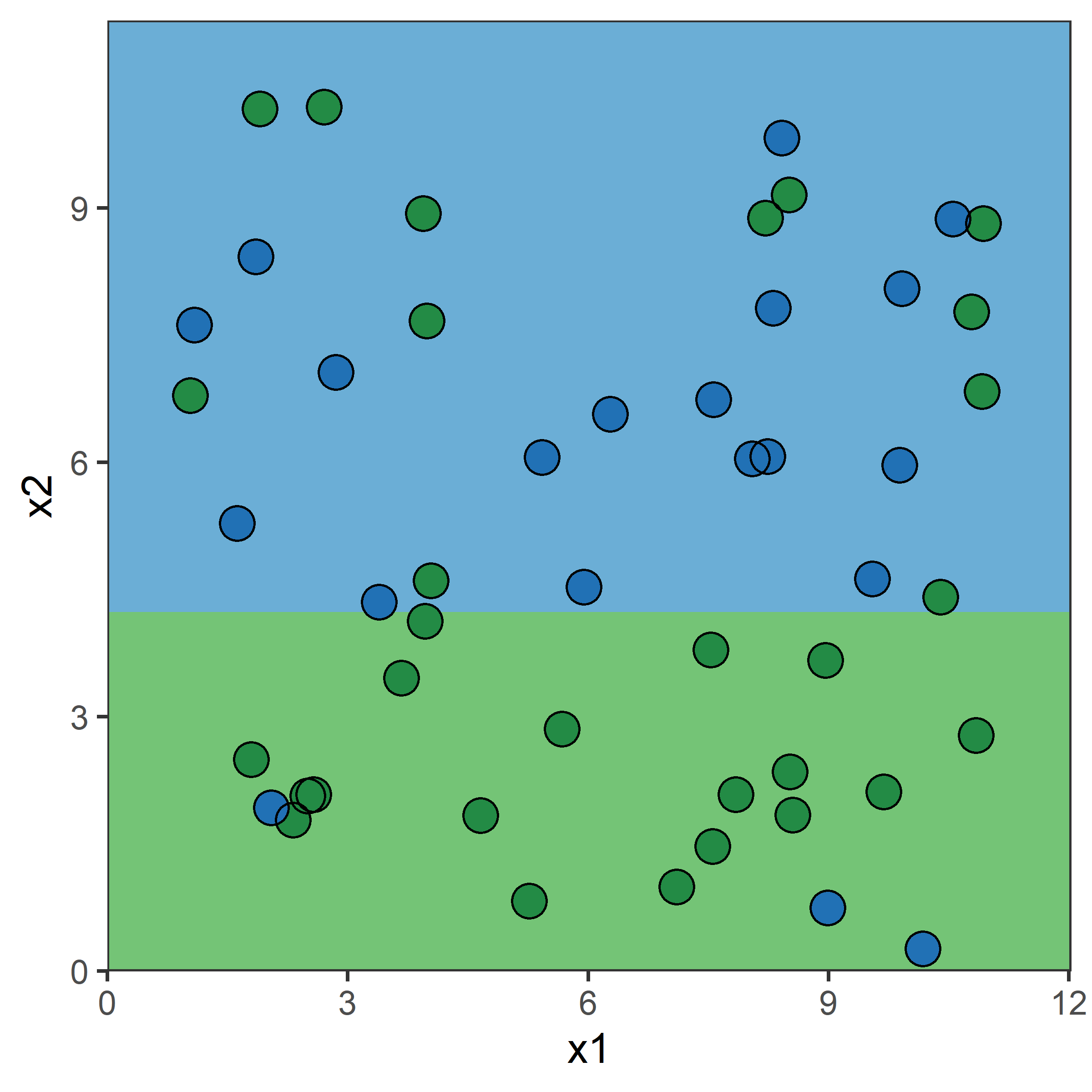

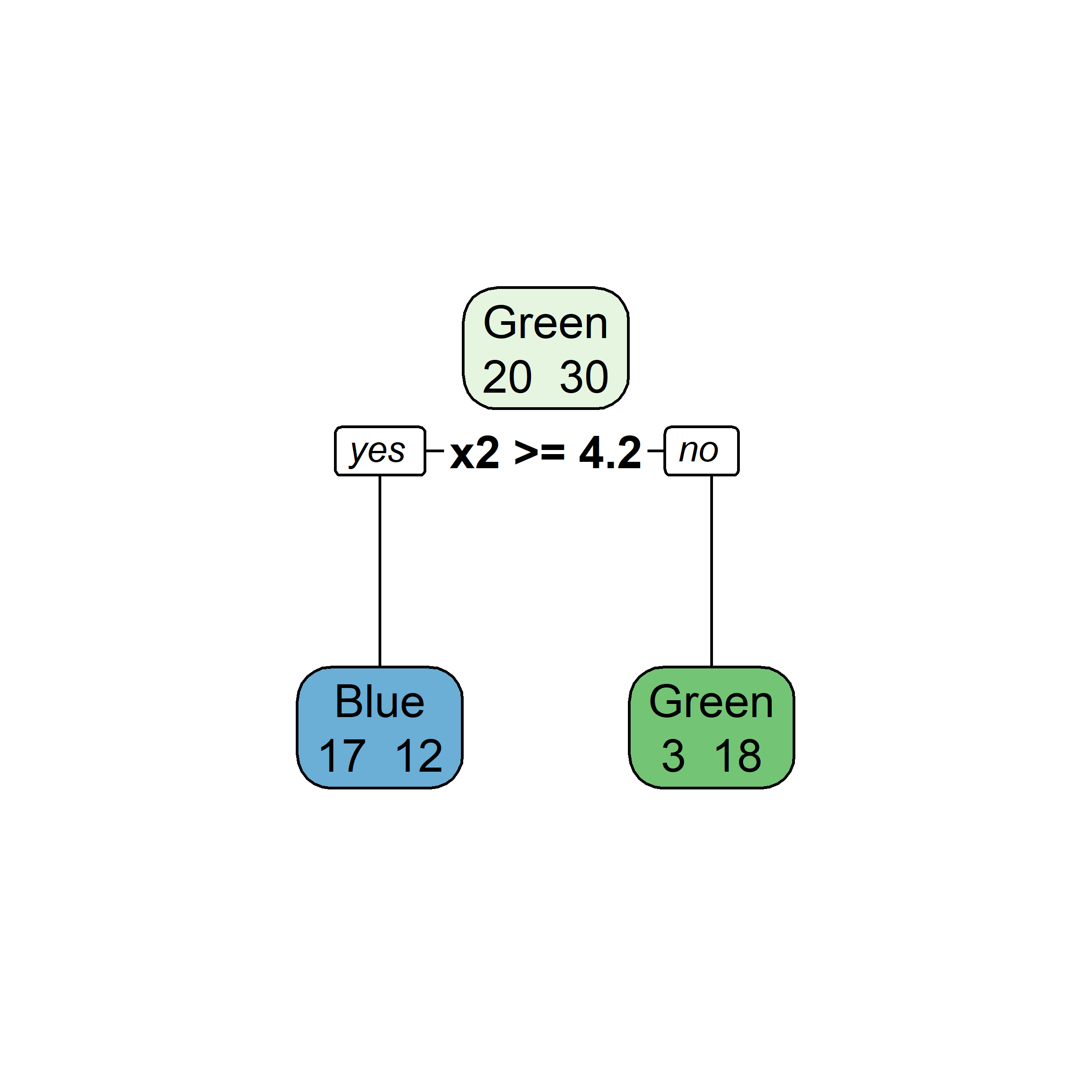

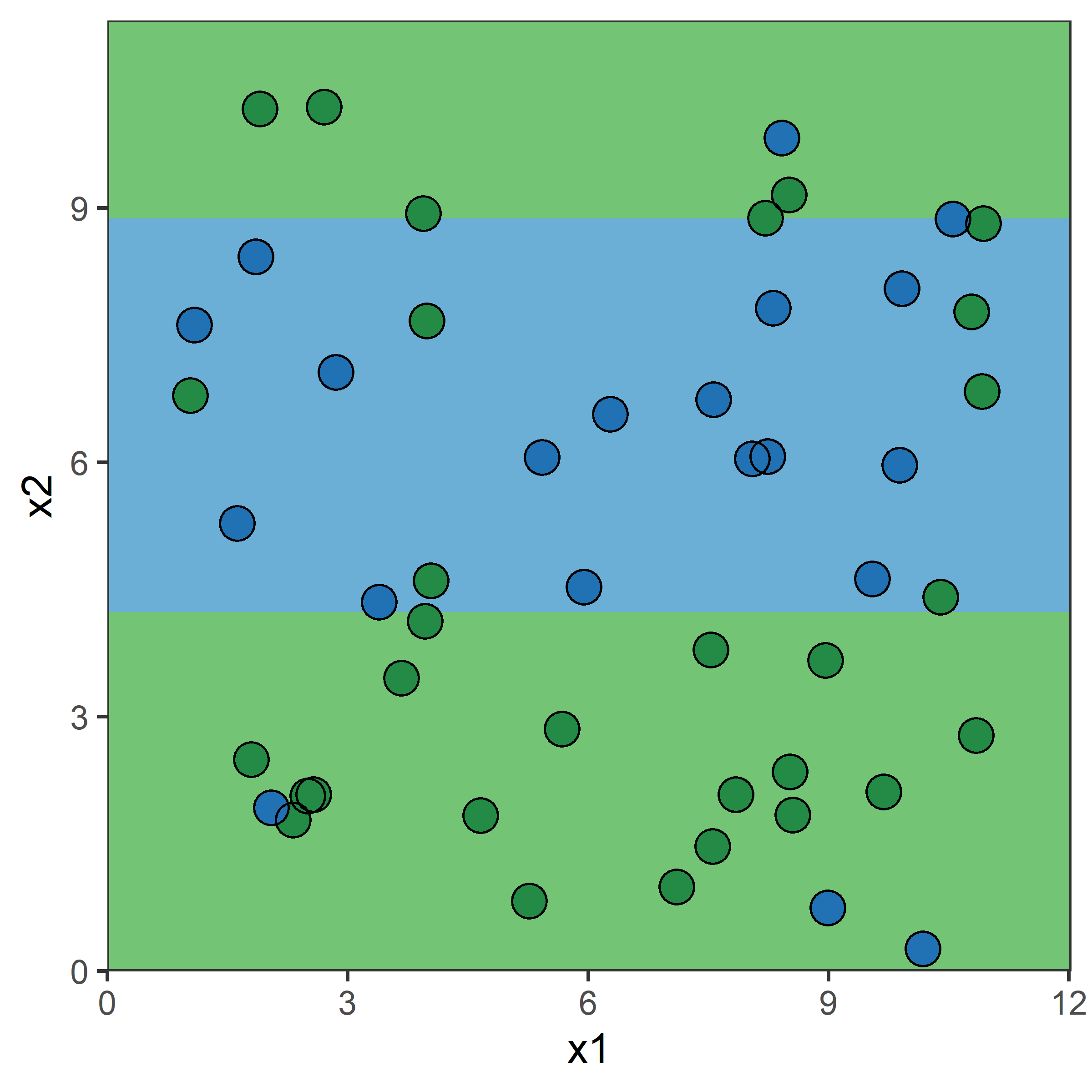

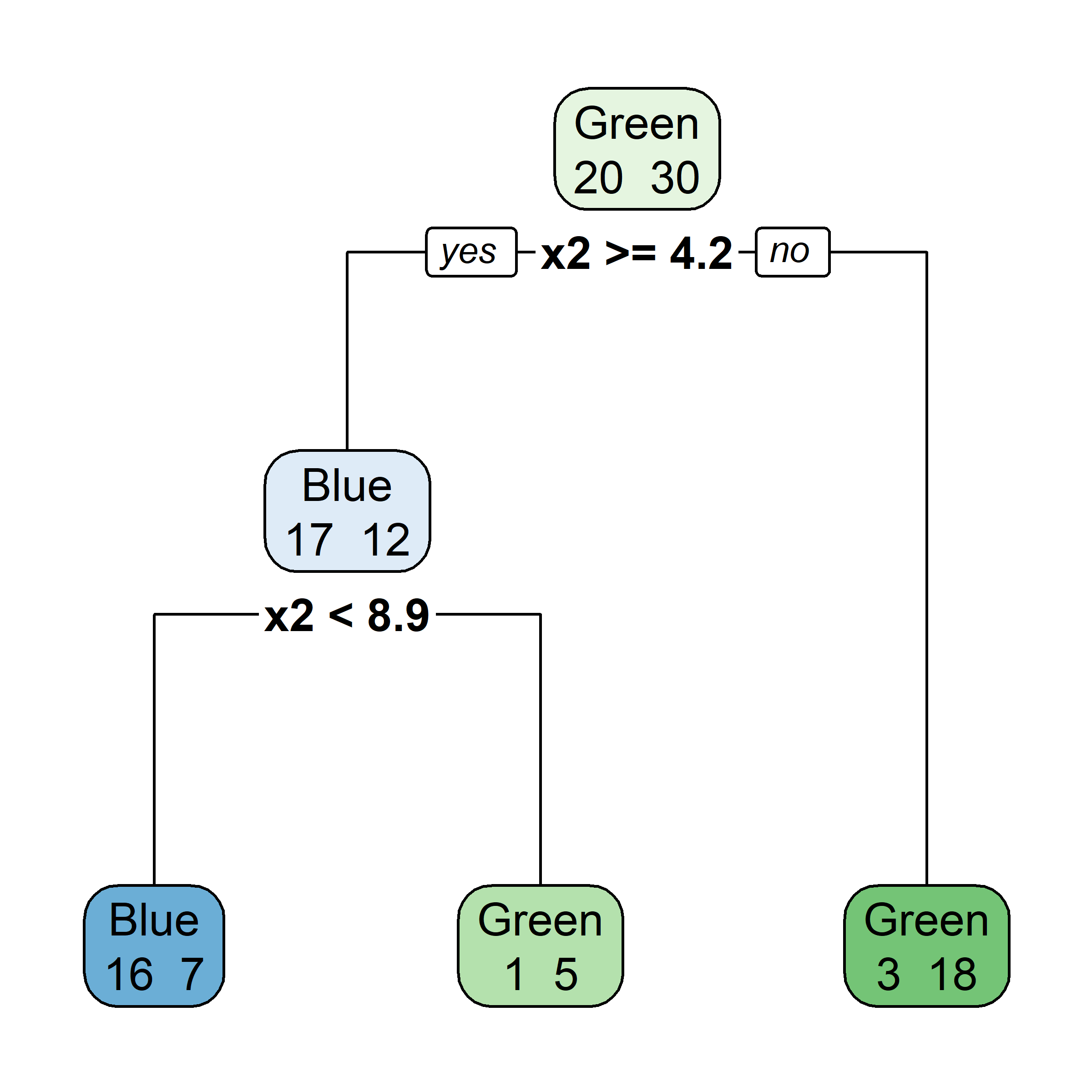

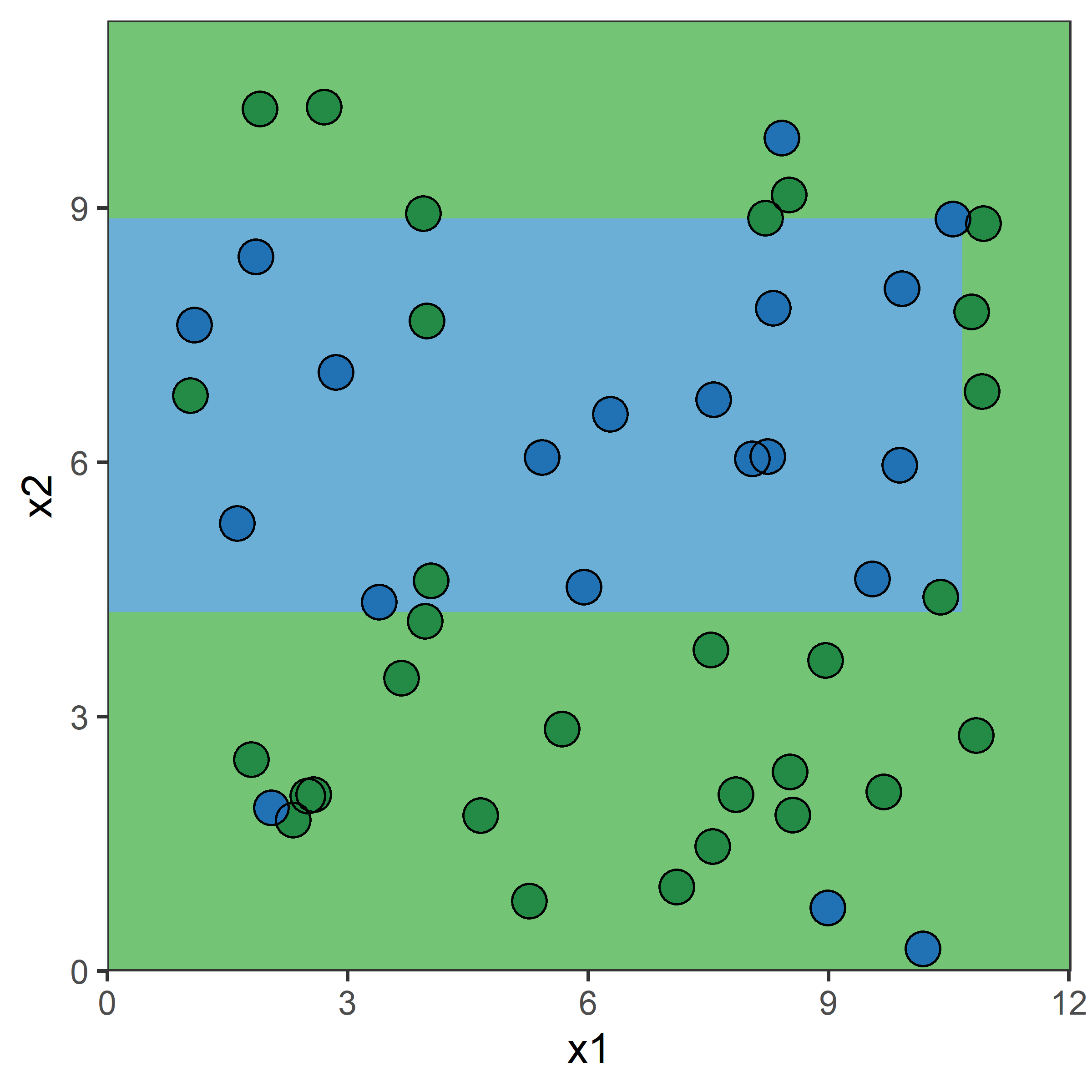

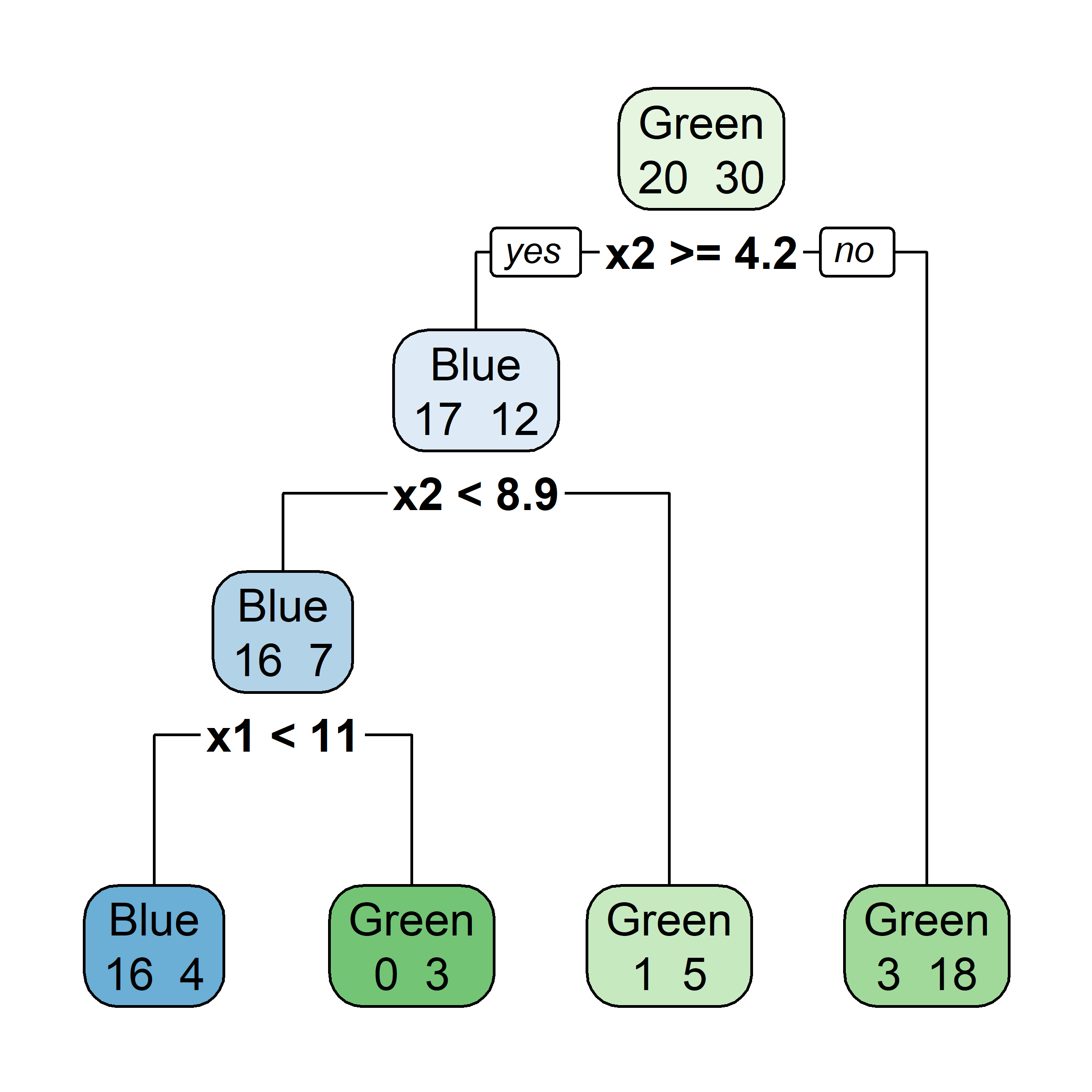

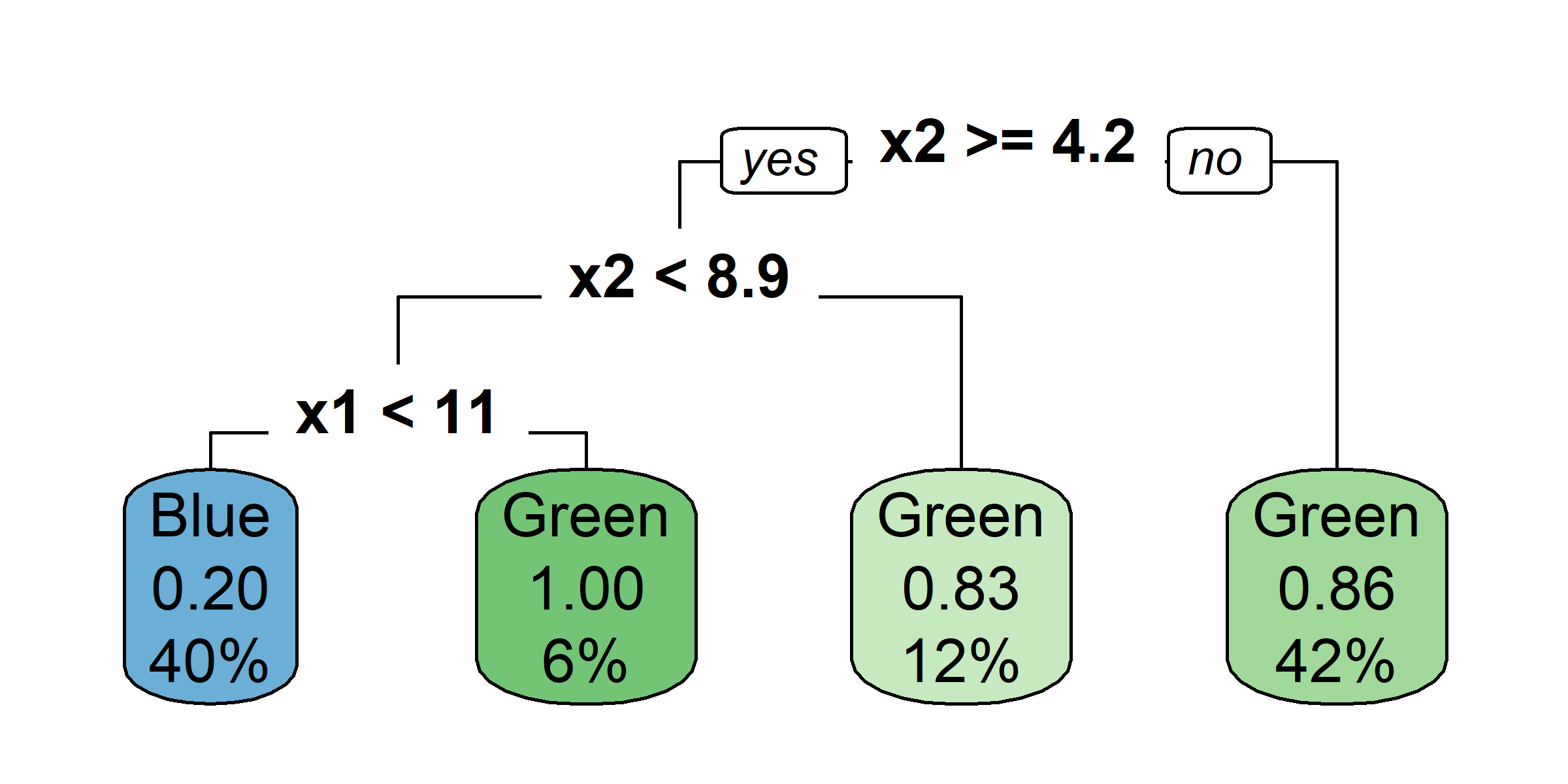

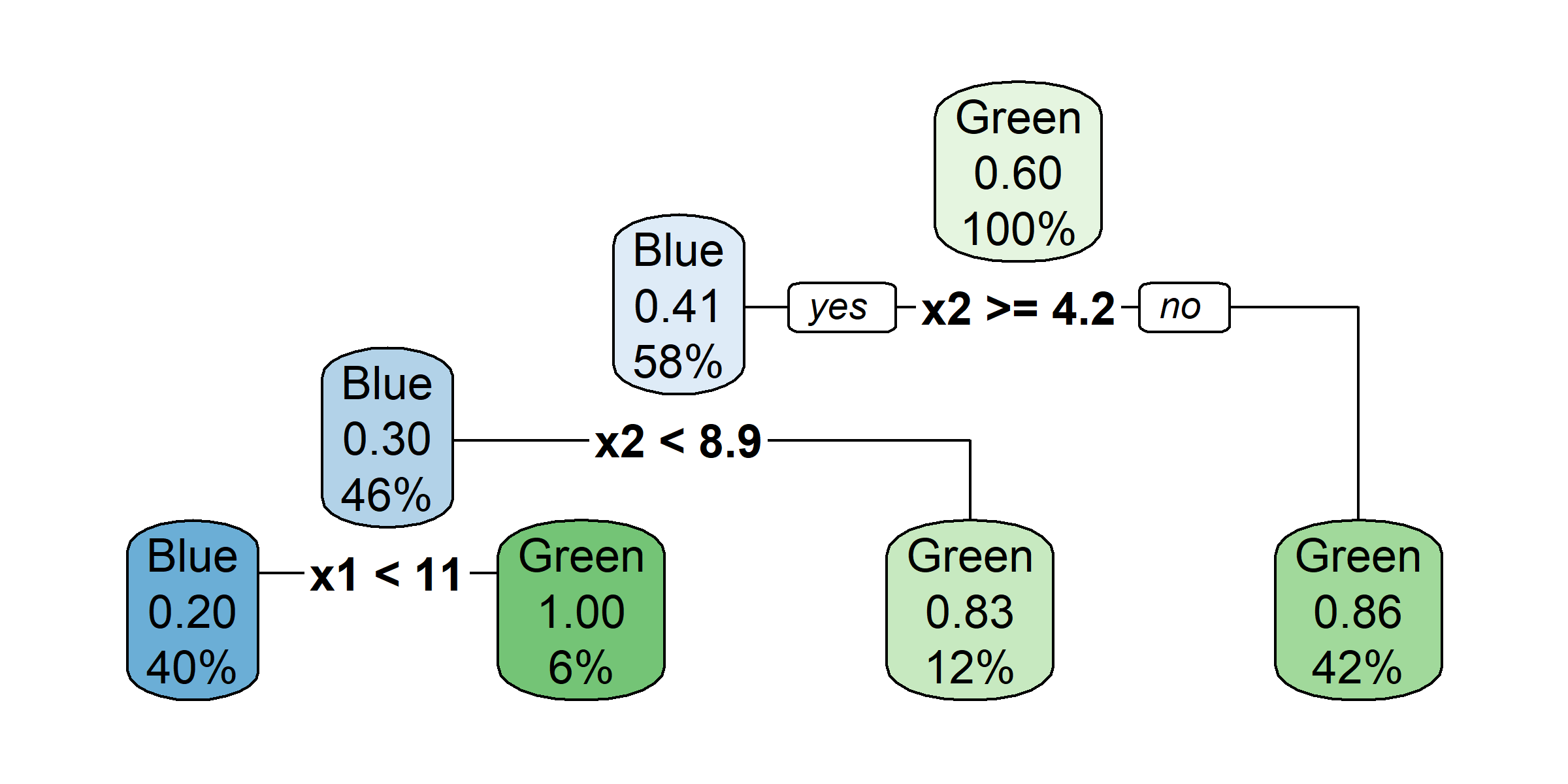

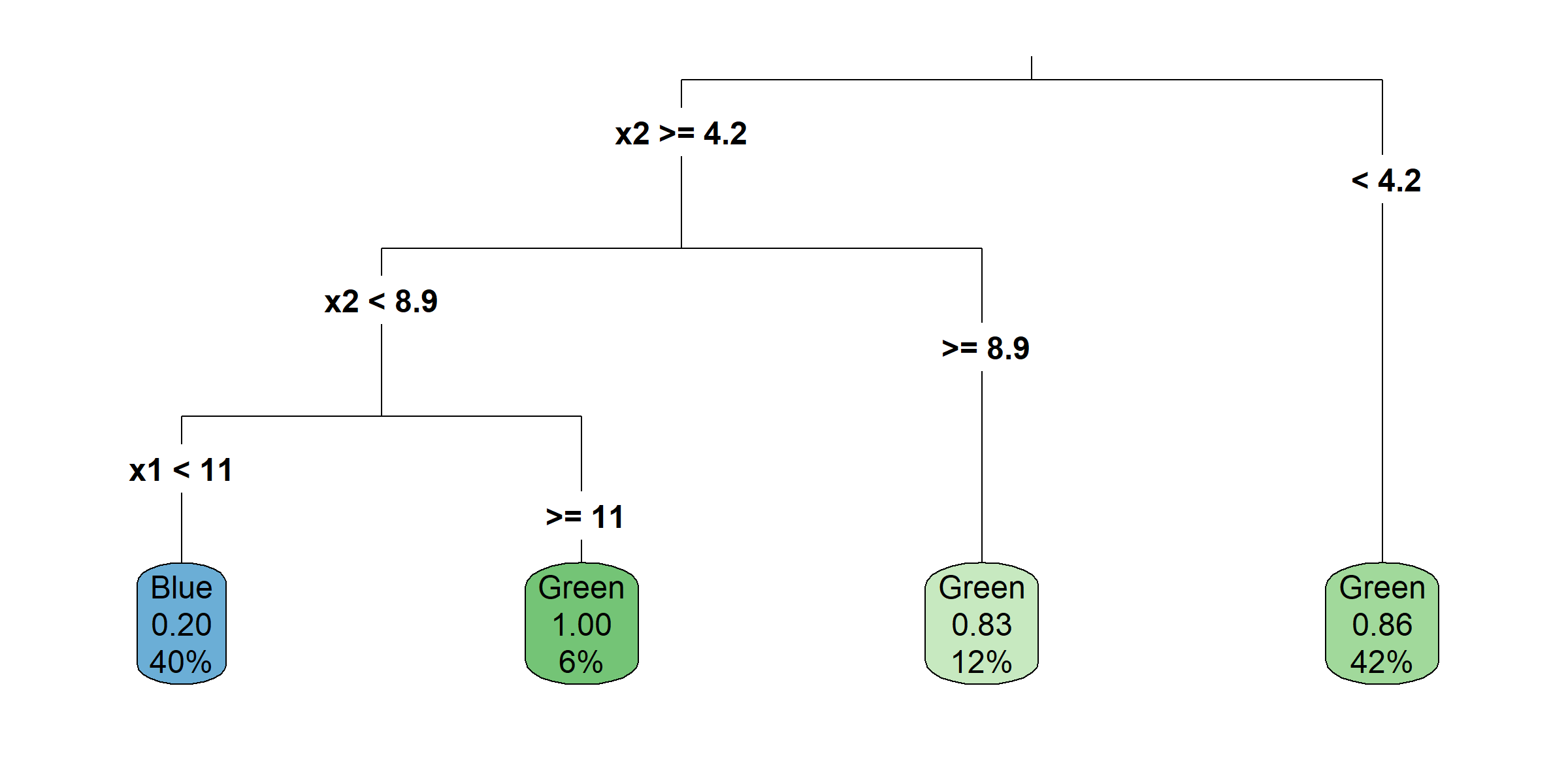

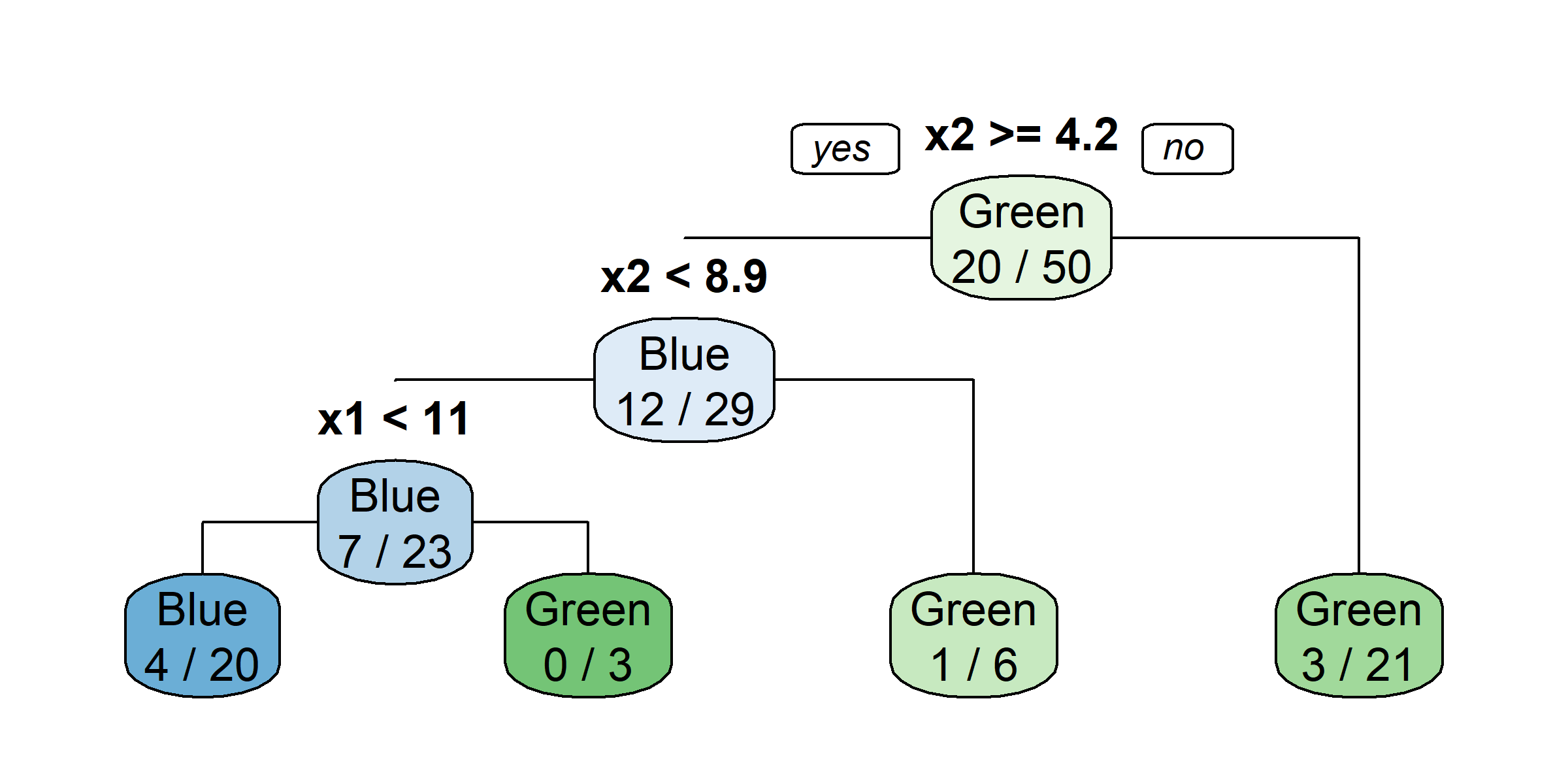

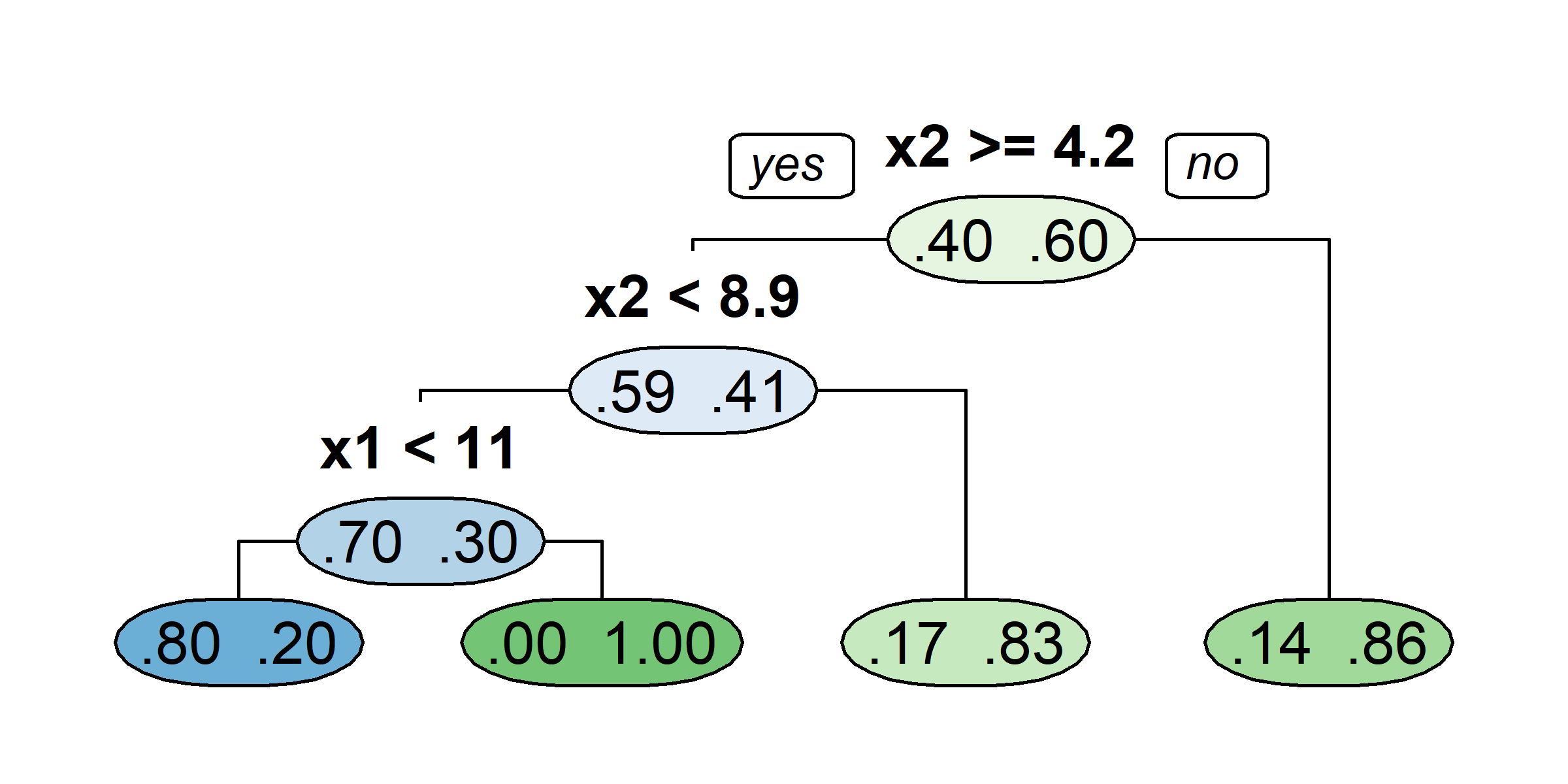

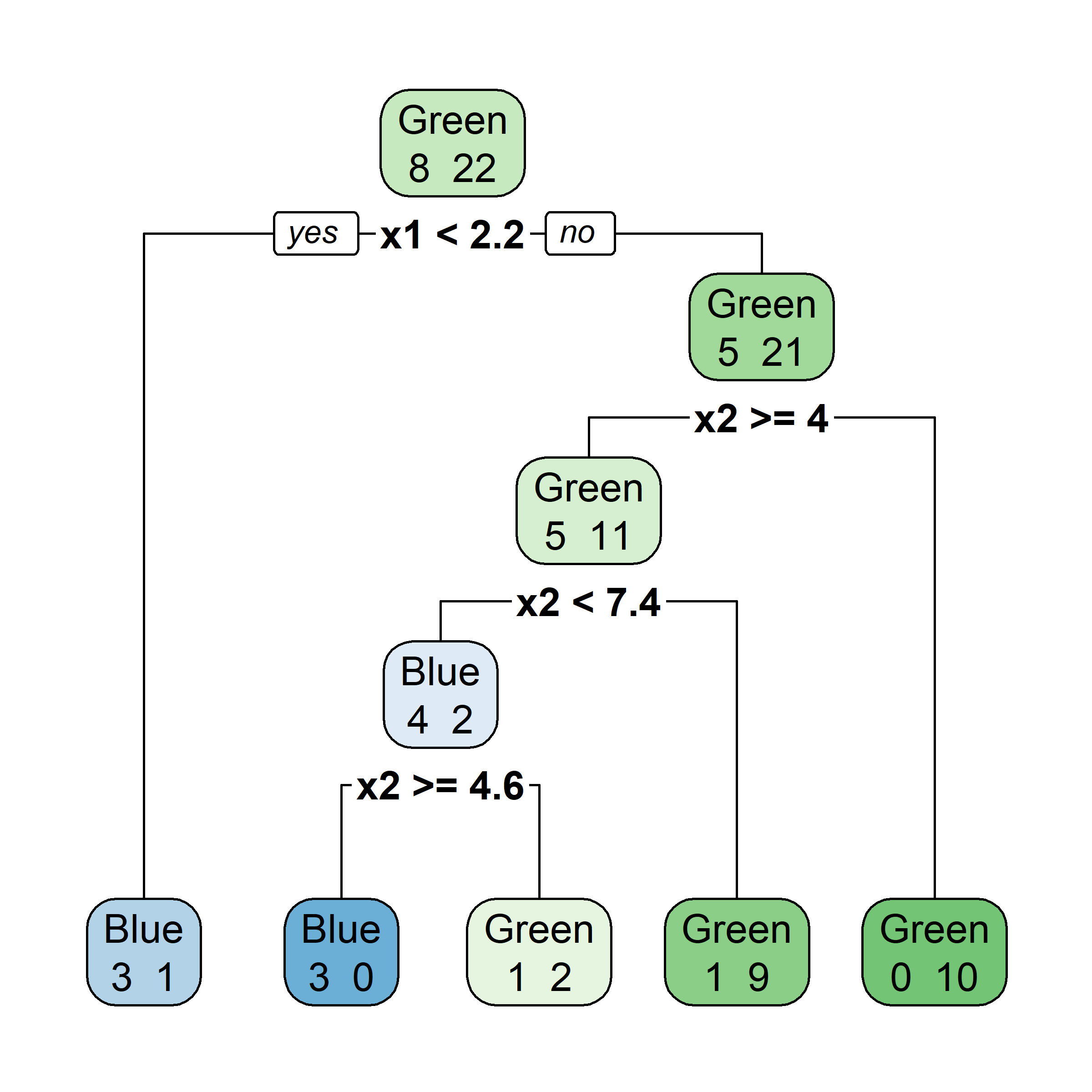

Growing a classification tree I

Growing a classification tree II

Growing a classification tree III

Growing a classification tree IV

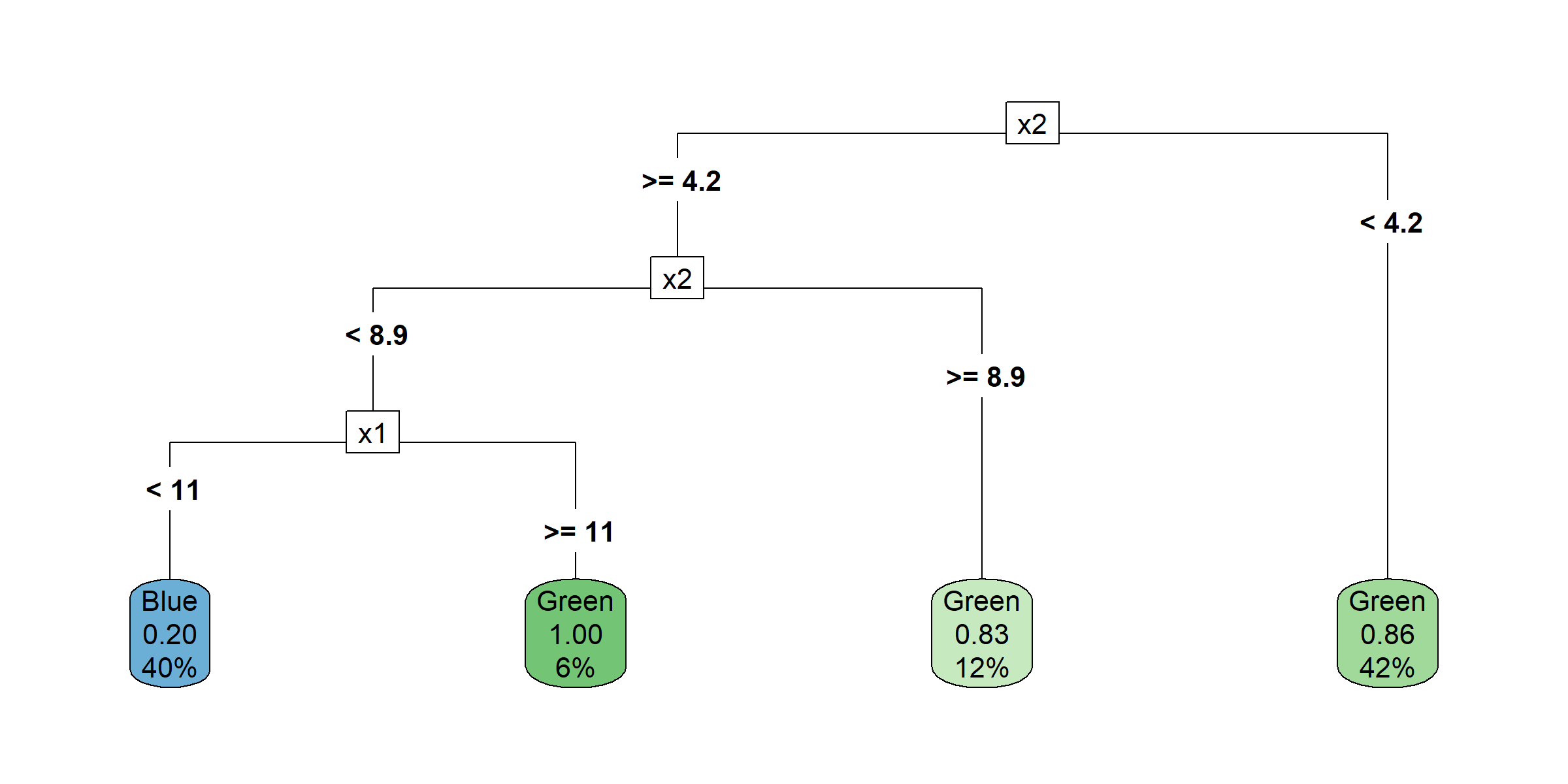

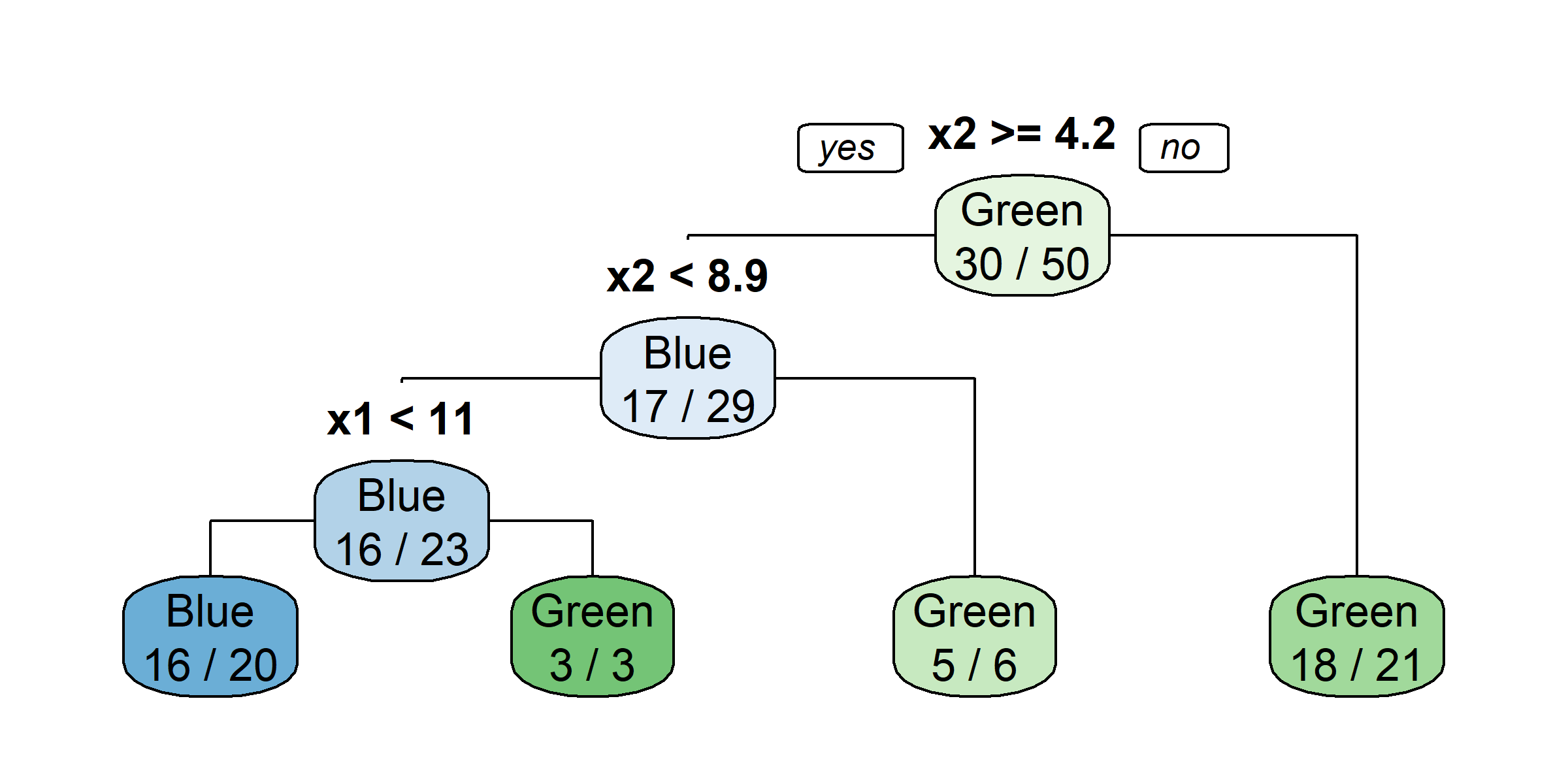

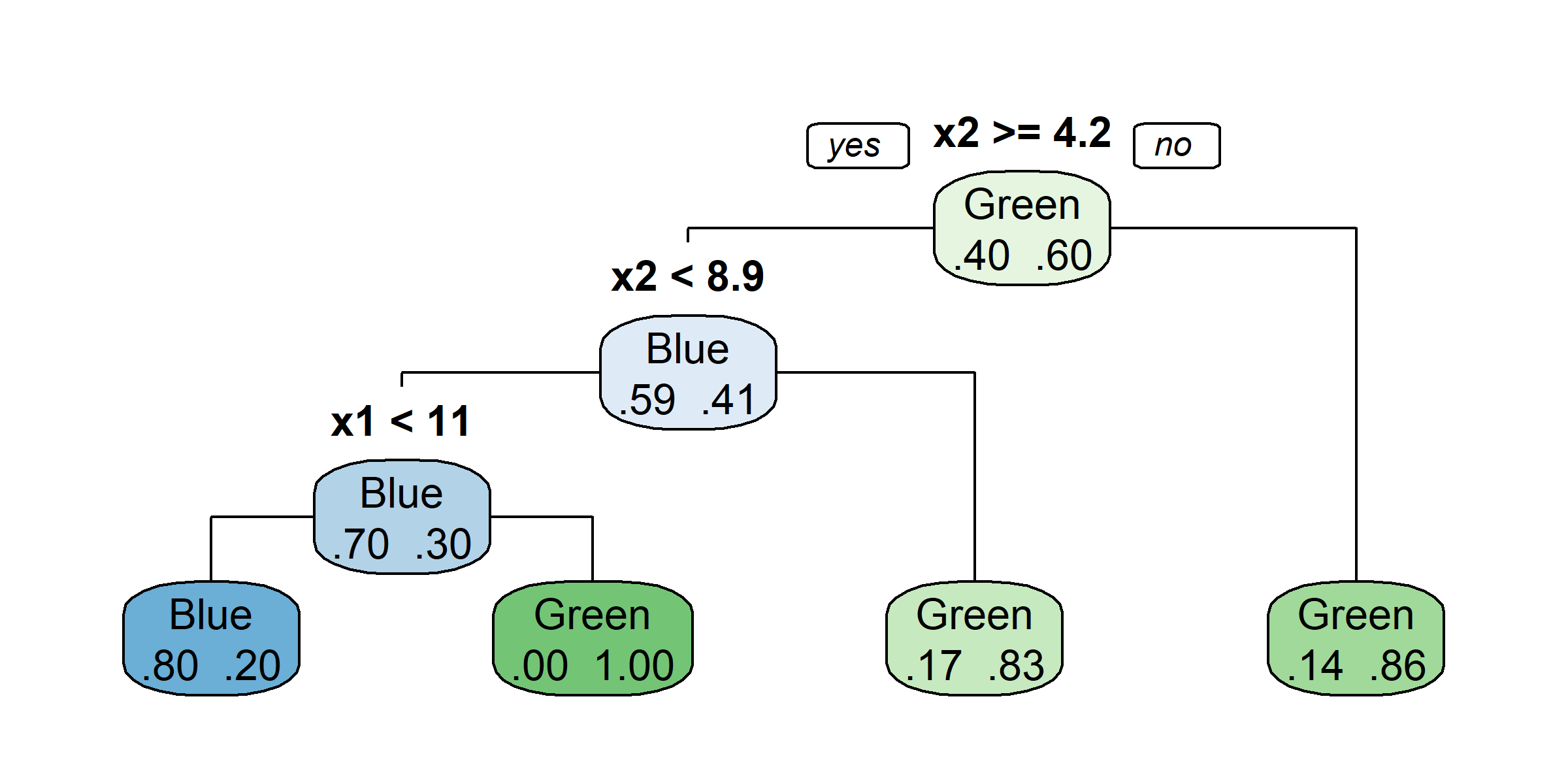

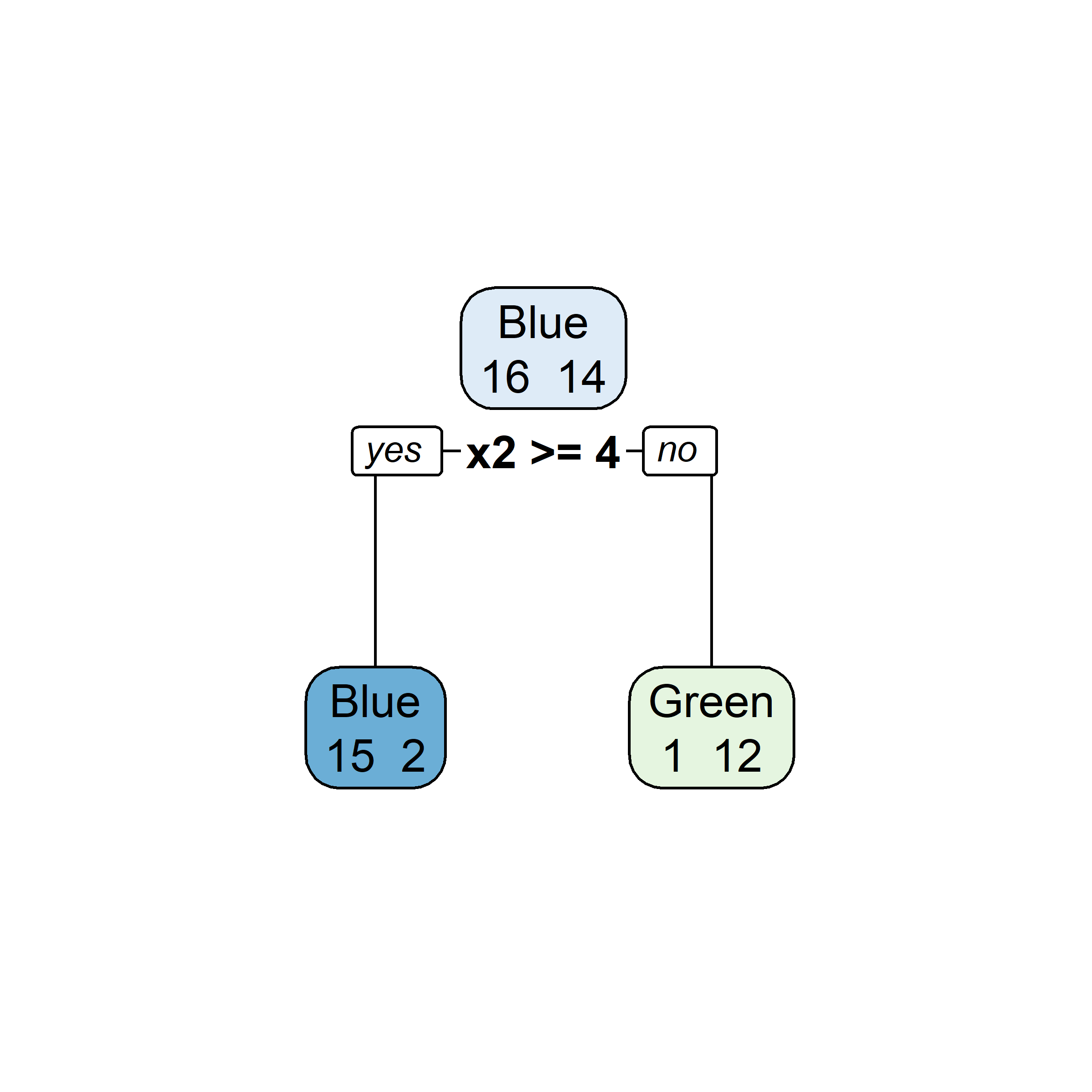

Multiple representations

Multiple representations II

National Flood Insurance Program

Available at OpenFEMA dataset.

National Flood Insurance Program (NFIP, image source)

First decision tree

Remove ID column

Dates to years and months

Code

claims$lossYear <- year(claims$lossDate)

claims$lossMonth <- month(claims$lossDate)

claims$lossDate <- NULL

claims$originalConstructionYear <- year(claims$originalConstructionDate)

claims$originalConstructionMonth <- month(claims$originalConstructionDate)

claims$originalConstructionDate <- NULL

claims$originalNBYear <- year(claims$originalNBDate)

claims$originalNBMonth <- month(claims$originalNBDate)

claims$originalNBDate <- NULL

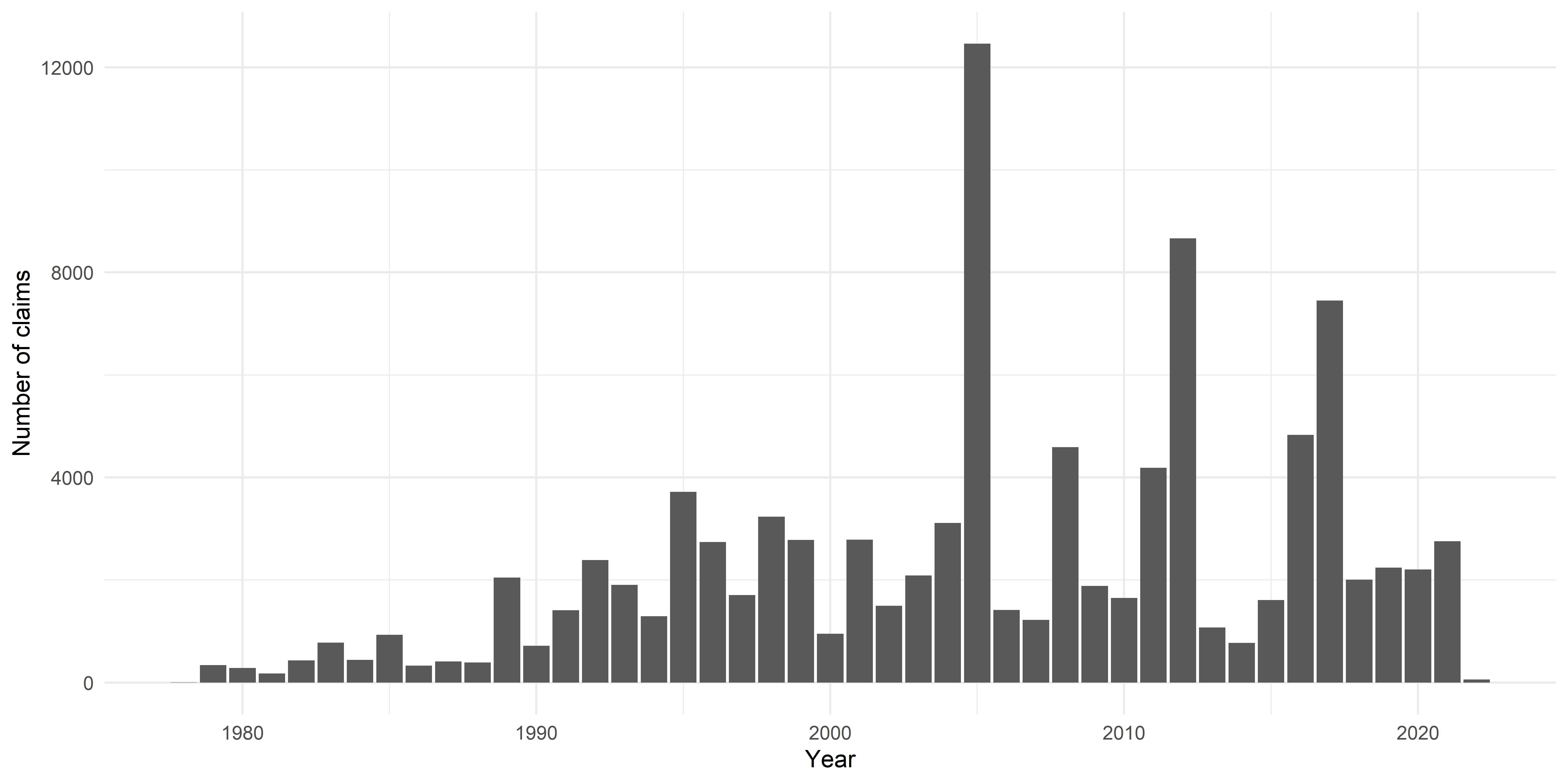

Plot claims by year

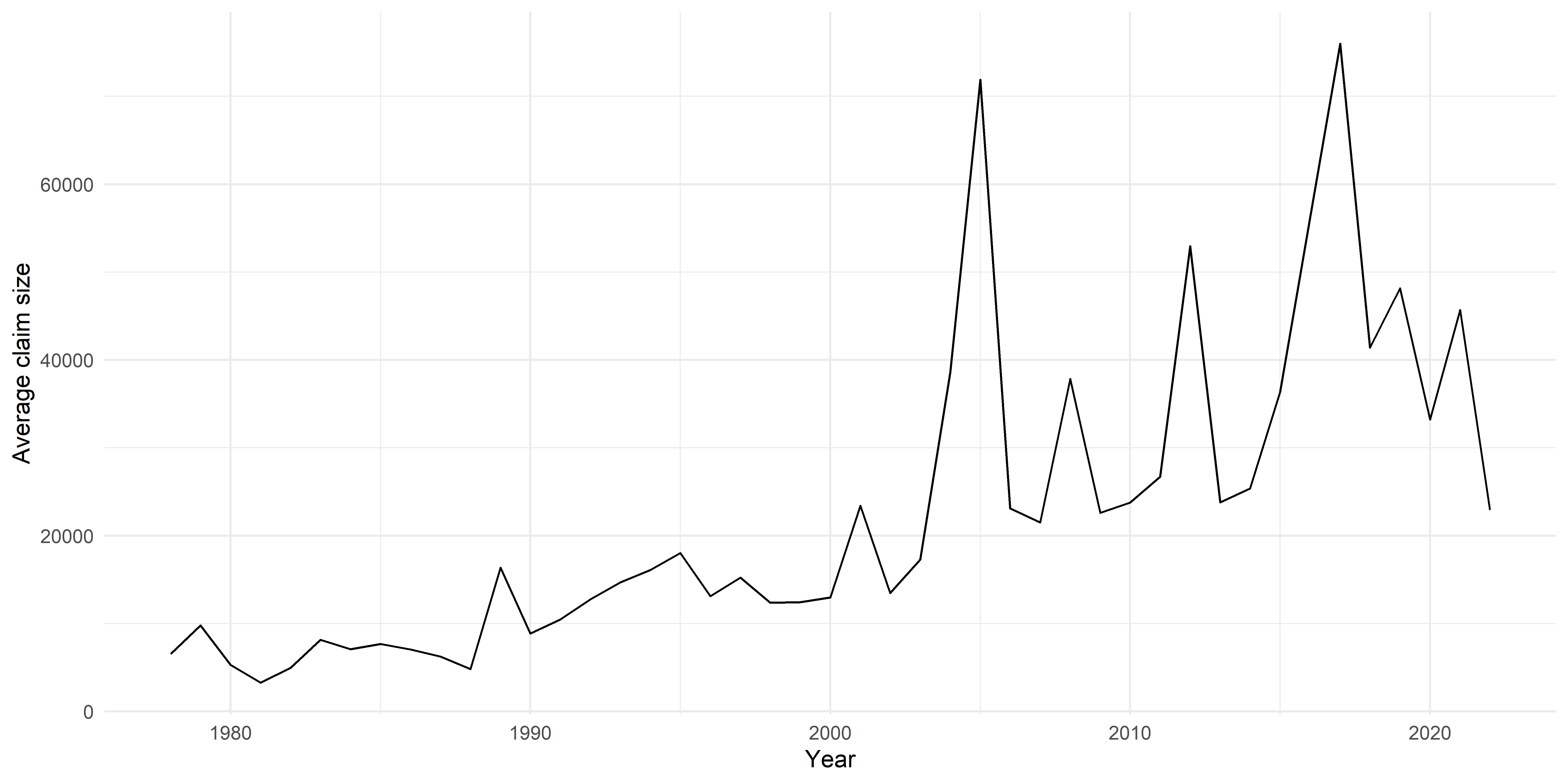

Plot average claim size by year

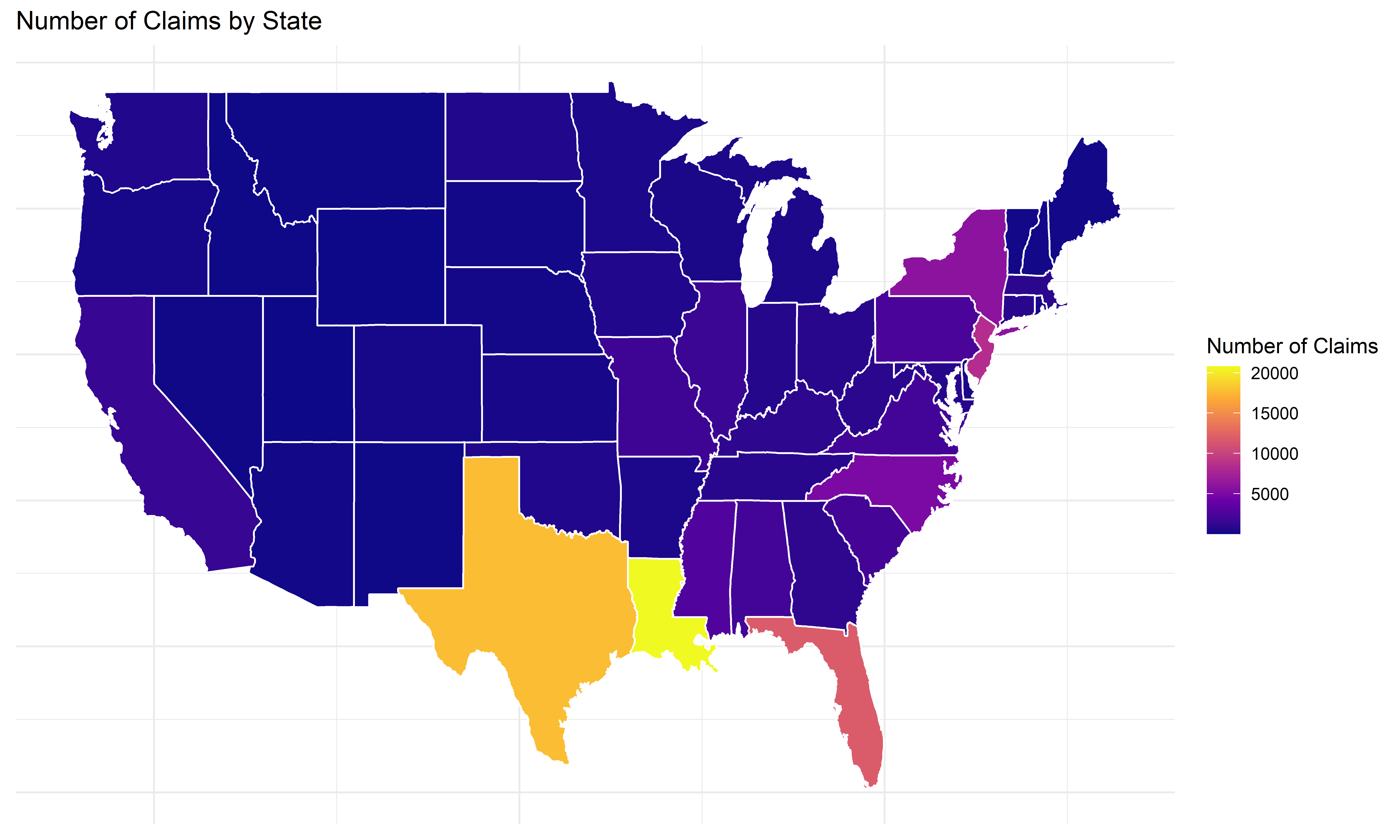

Number of claims by state

Prepare to make state-based maps for USA

claims$state_full <- state.name[match(claims$state, state.abb)]

state_claims <- claims %>%

group_by(state_full) %>%

summarise(num_claims = n(),

max_claim_size = max(amountPaidOnBuildingClaim),

common = num_claims >= nrow(claims) / 100)

claims$state_full <- NULL

# Merge with the map data

states_map <- map_data("state")

state_claims$region <- tolower(state_claims$state_full)

states_map <- left_join(states_map, state_claims, by = "region")Code

ggplot(states_map, aes(long, lat, group = group, fill = num_claims)) +

geom_polygon(color = "white") +

scale_fill_viridis_c(option = "C") +

labs(title = "Number of Claims by State",

fill = "Number of Claims") +

theme_minimal() +

theme(axis.title = element_blank(), axis.text = element_blank(), axis.ticks = element_blank())

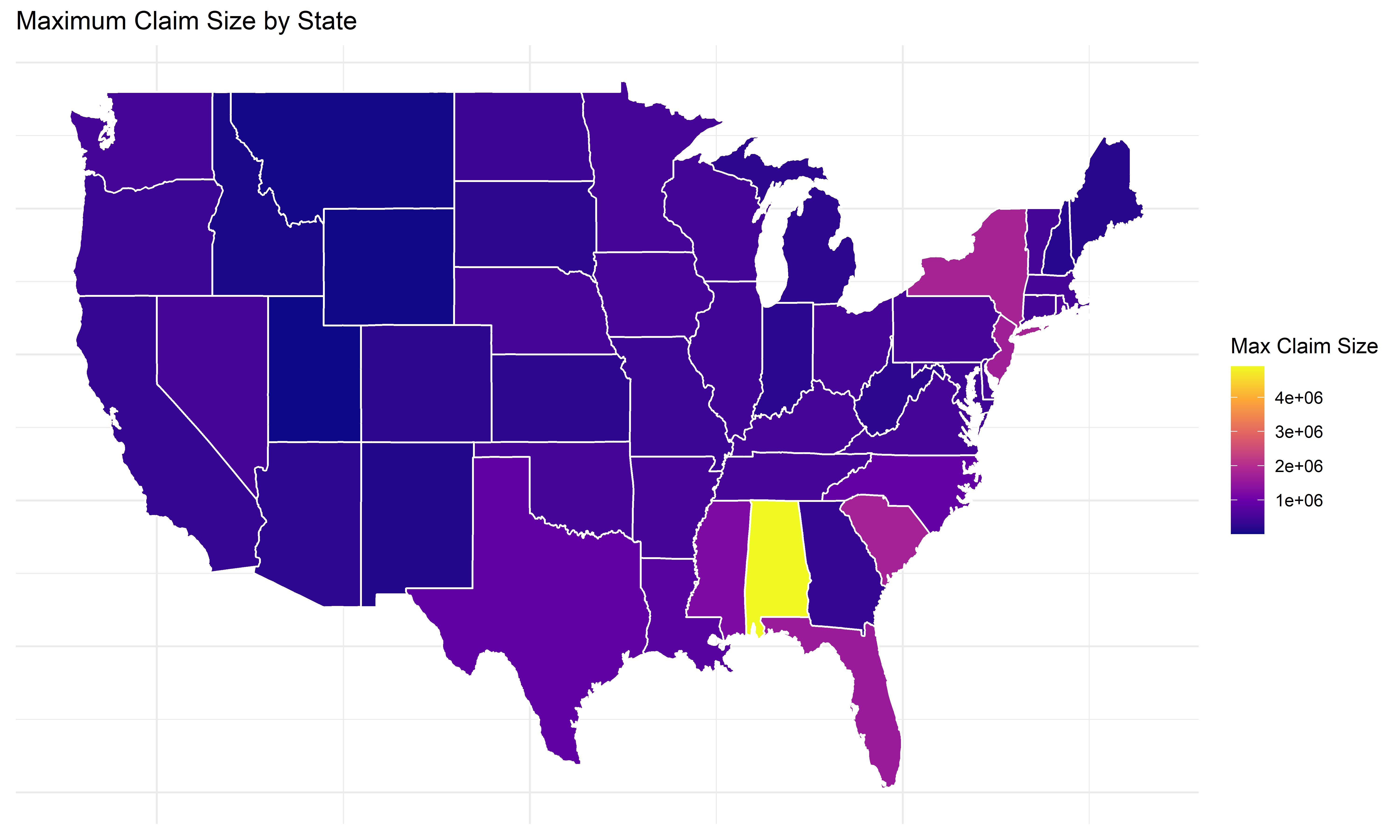

Max claim size by state

Code

# Plot maximum claim size by state

ggplot(states_map, aes(long, lat, group = group, fill = max_claim_size)) +

geom_polygon(color = "white") +

scale_fill_viridis_c(option = "C") +

labs(title = "Maximum Claim Size by State",

fill = "Max Claim Size") +

theme_minimal() +

theme(axis.title = element_blank(), axis.text = element_blank(), axis.ticks = element_blank())

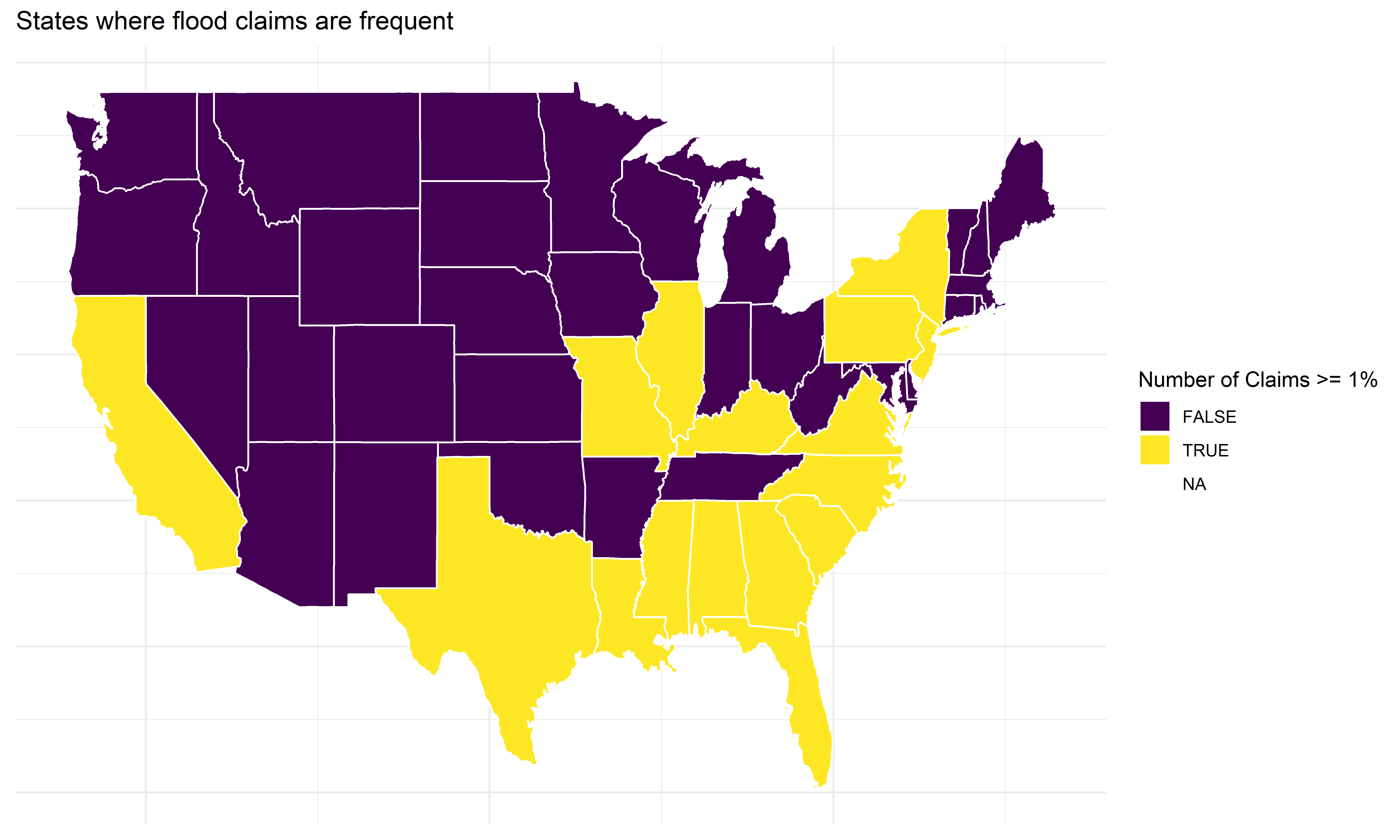

Some states have very few claims

Code

# Plot states where floods are common

ggplot(states_map, aes(long, lat, group = group, fill = common)) +

geom_polygon(color = "white") +

scale_fill_viridis_d() +

labs(title = "States where flood claims are frequent",

fill = "Number of Claims >= 1%") +

theme_minimal() +

theme(axis.title = element_blank(), axis.text = element_blank(), axis.ticks = element_blank())

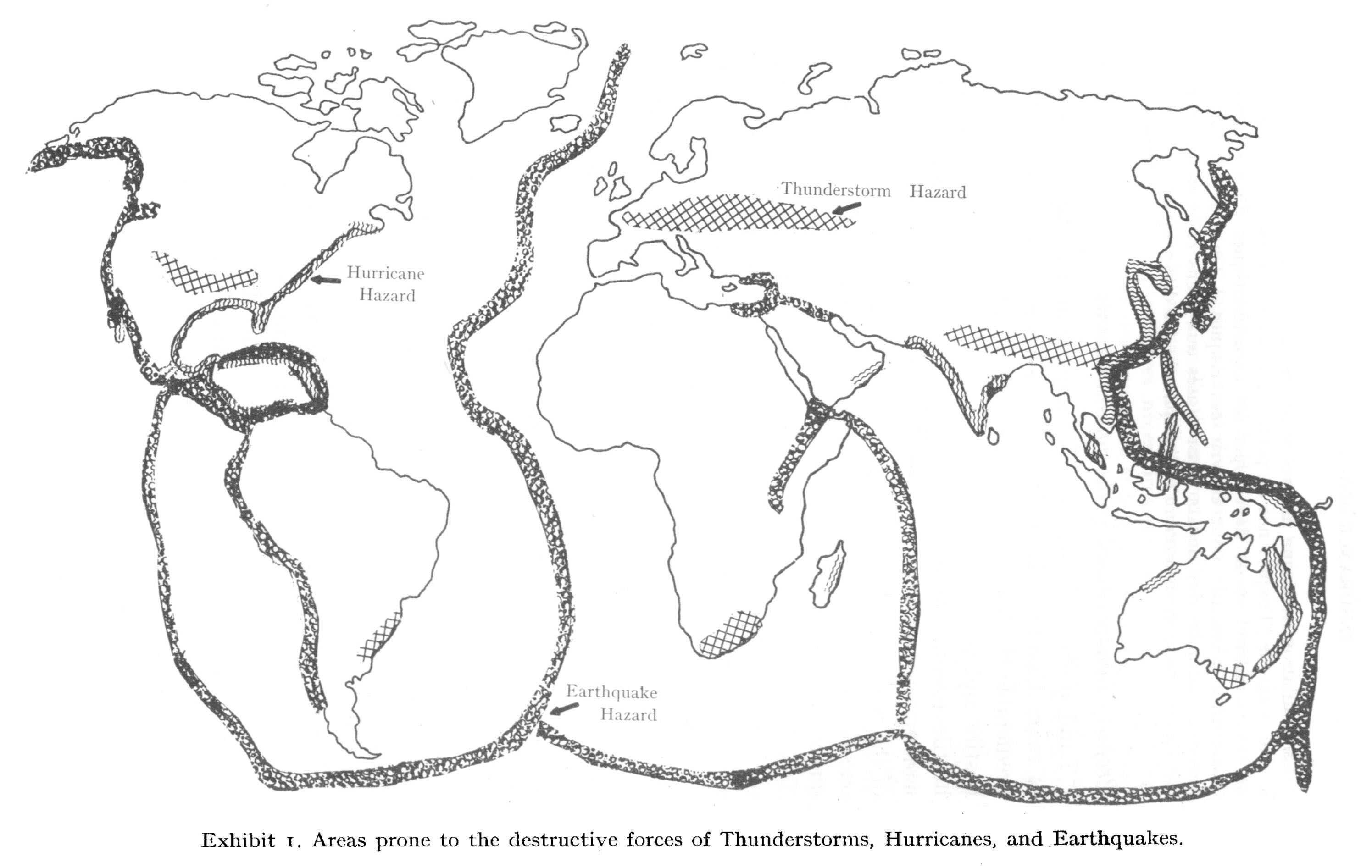

Geographical distribution of perils

Friedman Exhibit 1 (p. 10).

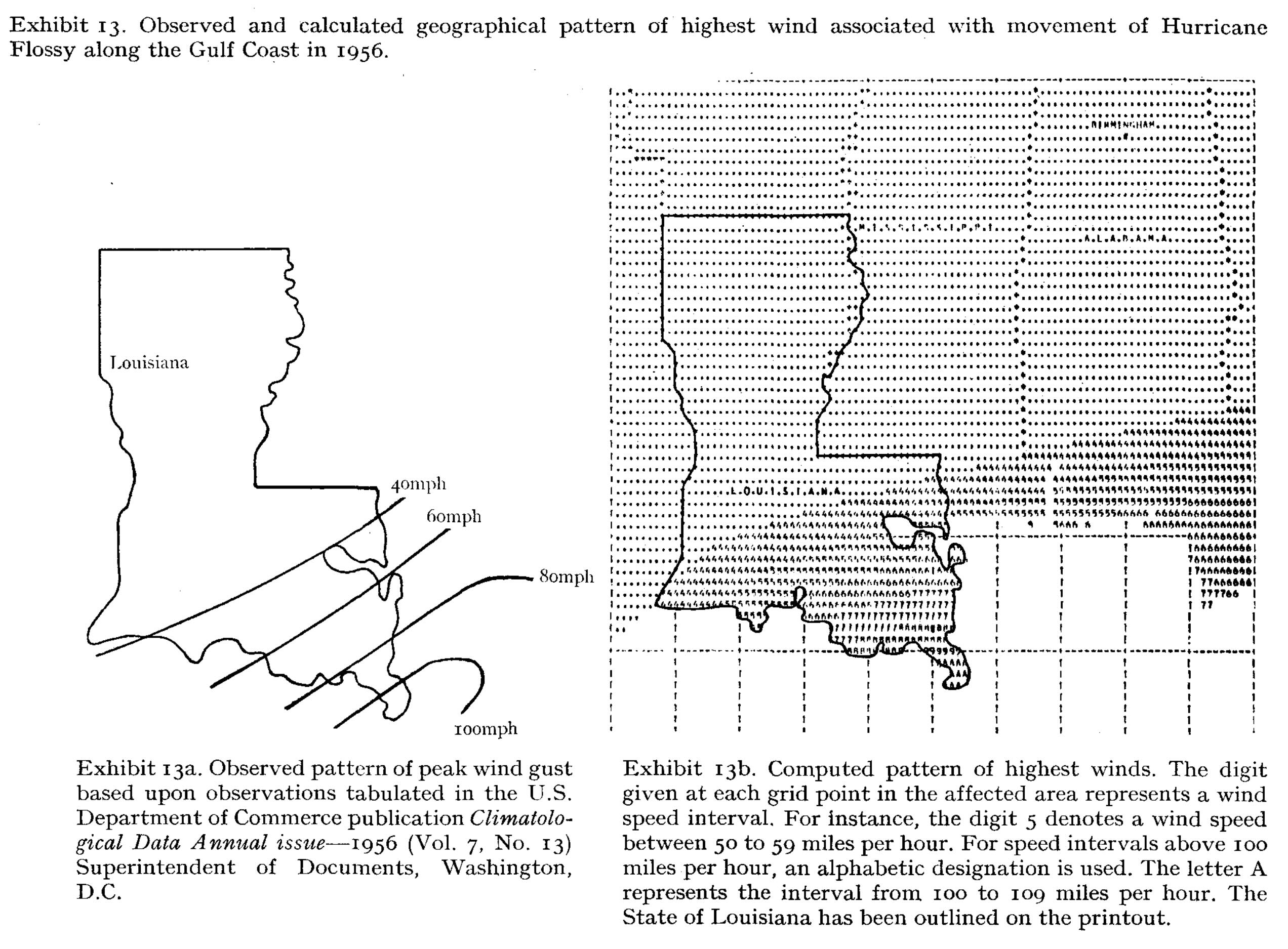

Hot spots

Friedman Exhibit 13 (p. 46).

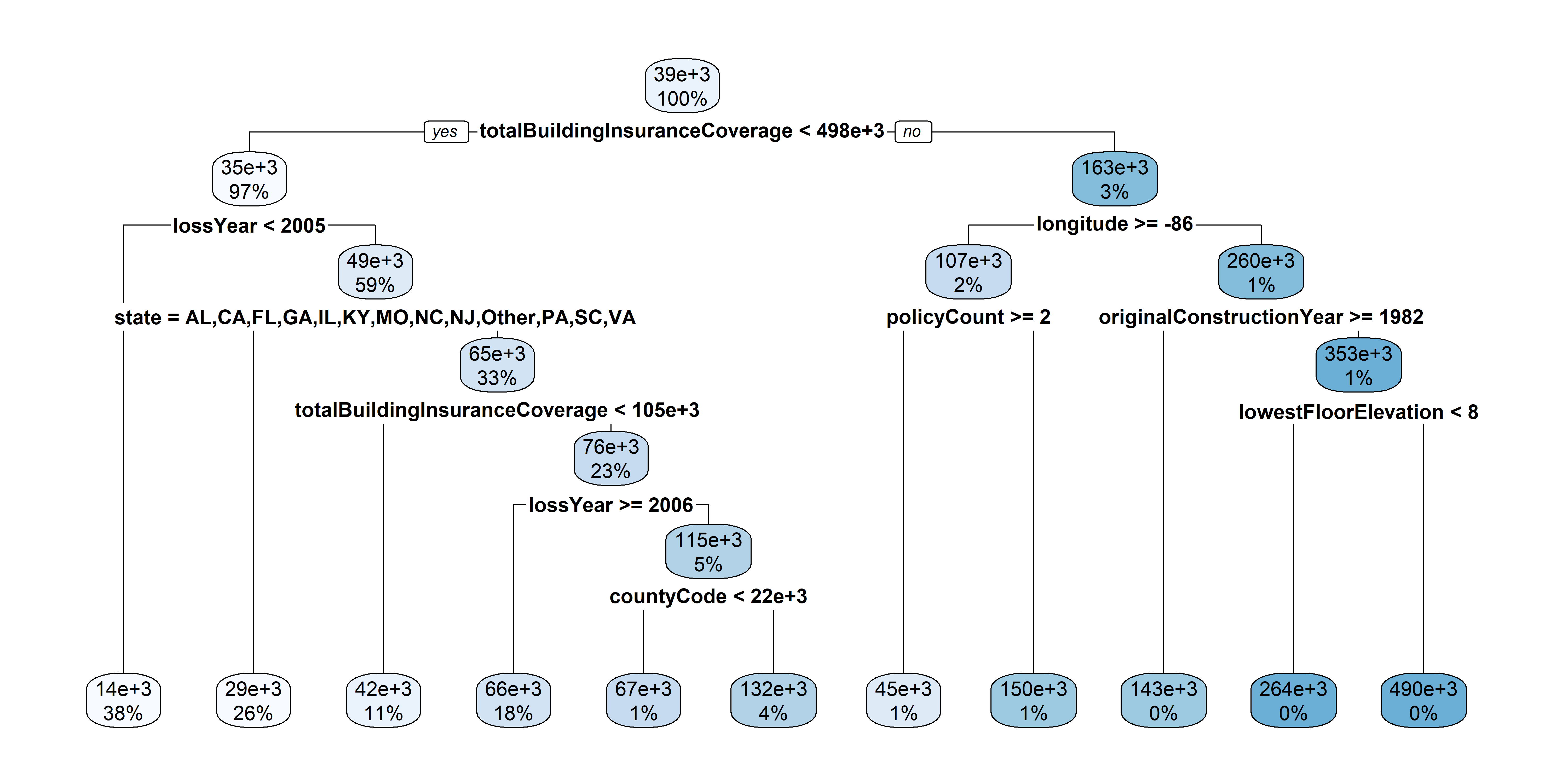

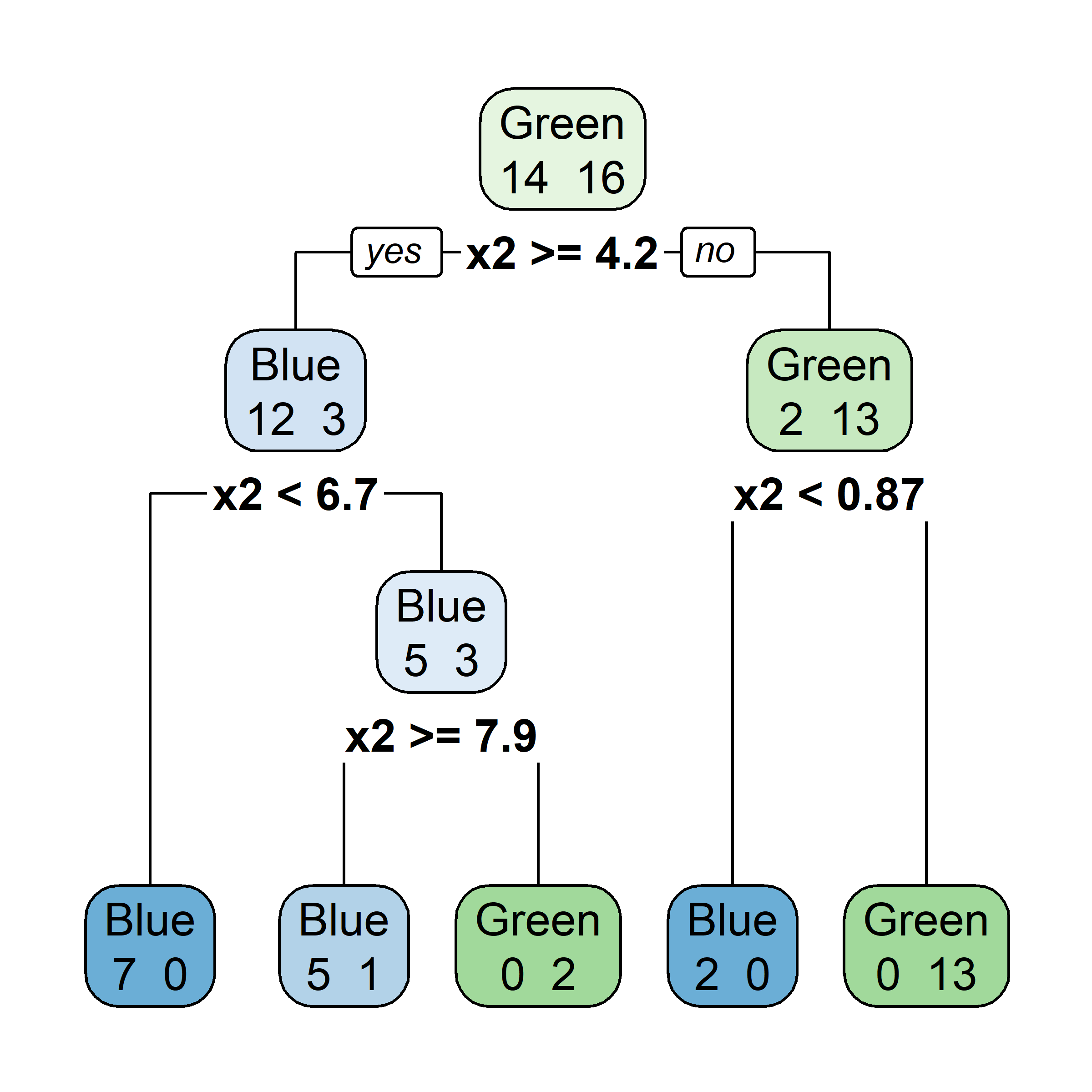

New tree

More data

What’s the best size of tree

The smallest tree is just a root node (no splits).

The upper limit is to grow until one observation in each region.

How large should we grow the tree?

- What’s wrong if the tree is too small?

- What’s wrong if the tree is too large?

A large tree for the flood insurance data

Code

# I have already shuffled this data

train_val_index <- 1:(0.8*nrow(claims))

train_val_set <- claims[train_val_index, ]

test_set <- claims[-train_val_index, ]

train_index <- 1:(0.75*nrow(train_val_set))

train_set <- train_val_set[train_index, ]

val_set <- train_val_set[-train_index, ]

# train_set$rateMethod <- factor(train_set$rateMethod)

train_set$state <- factor(train_set$state)

# val_set$rateMethod <- factor(val_set$rateMethod, levels = levels(train_set$rateMethod))

val_set$state <- factor(val_set$state, levels = levels(train_set$state))

# test_set$rateMethod <- factor(test_set$rateMethod, levels = levels(train_set$rateMethod))

test_set$state <- factor(test_set$state, levels = levels(train_set$state))

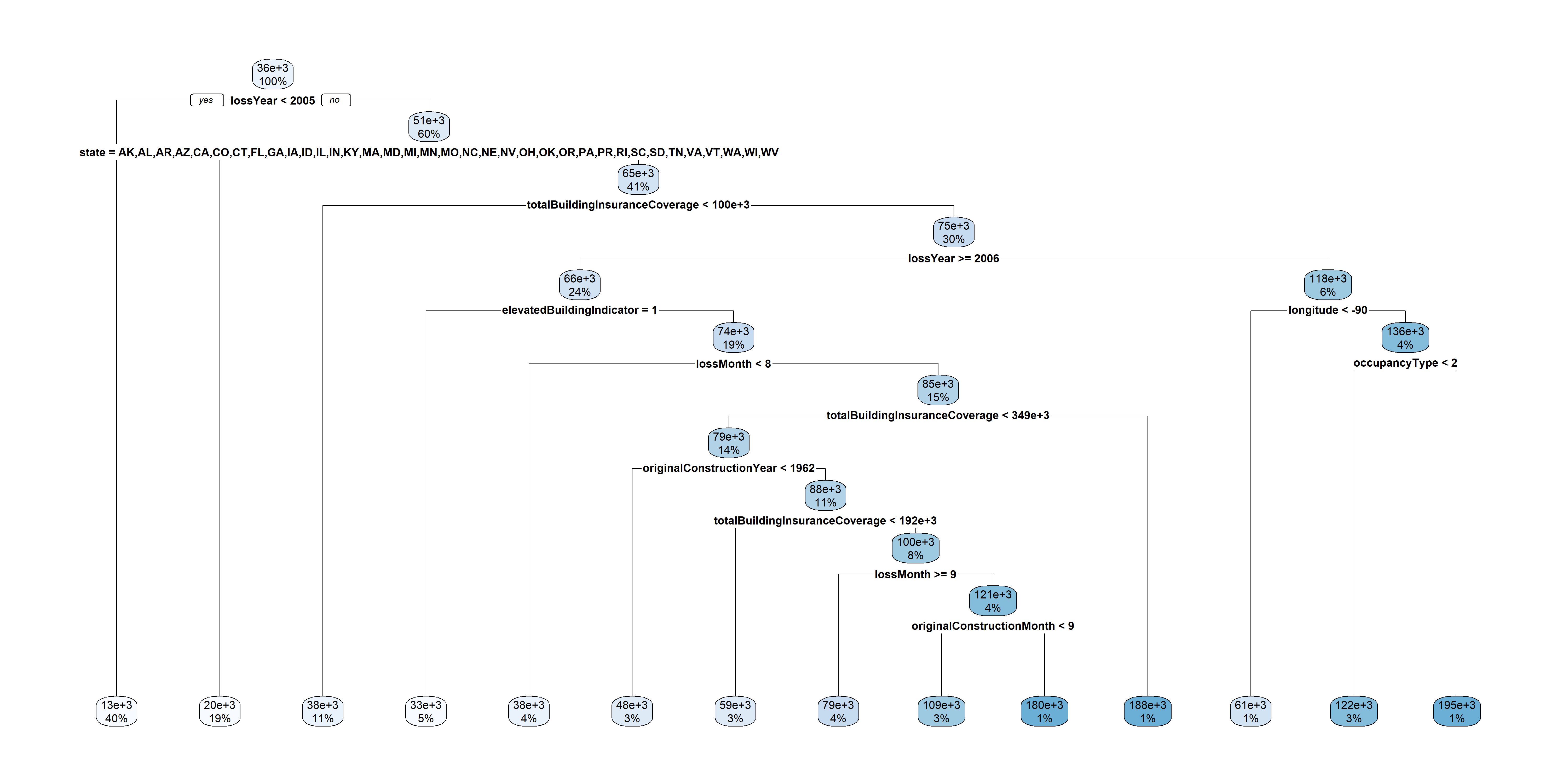

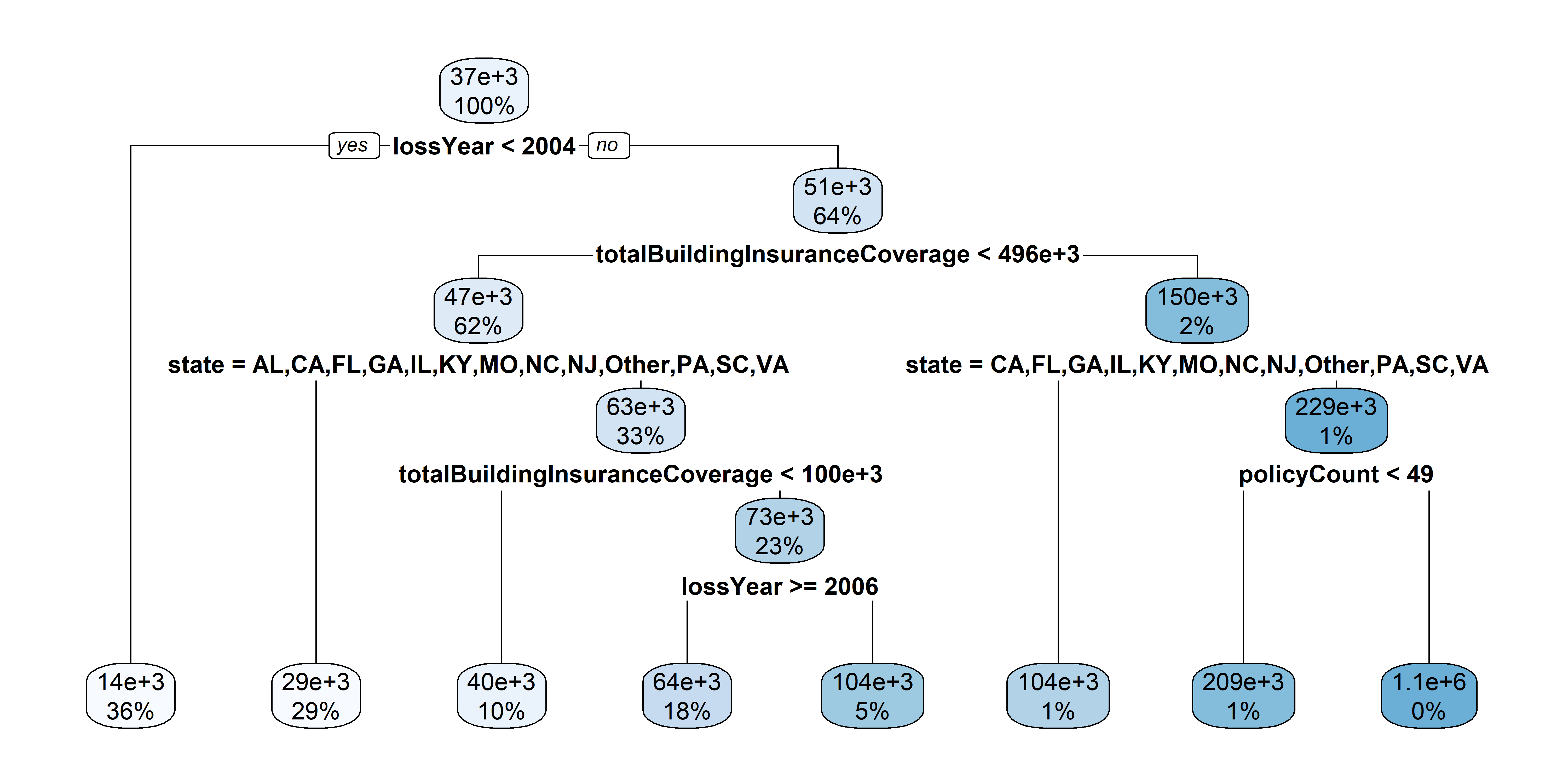

The full tree for train pricing

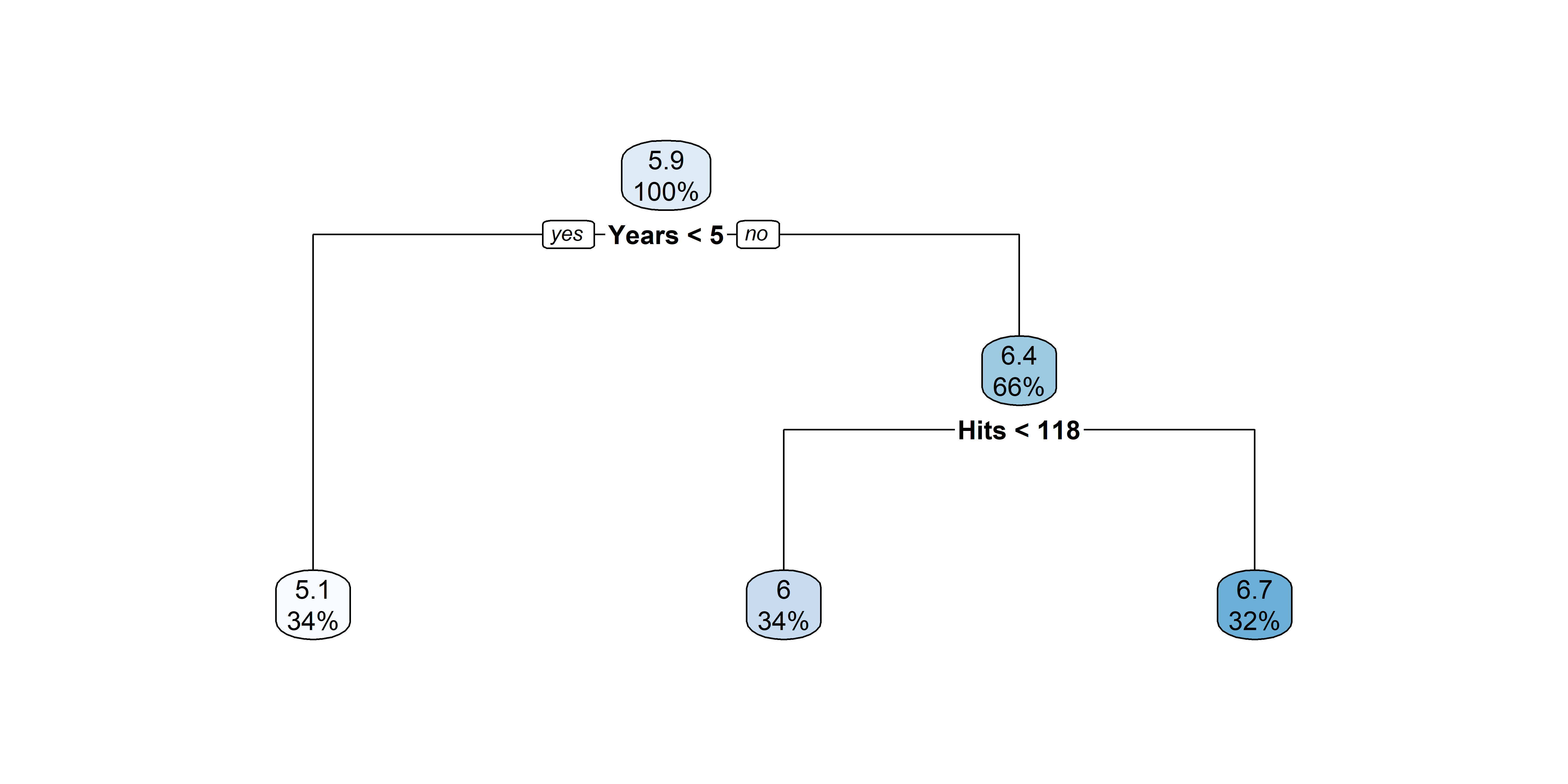

Unpruned Hitters tree: all predictors

The unpruned tree that results from top-down greedy splitting on the training data.

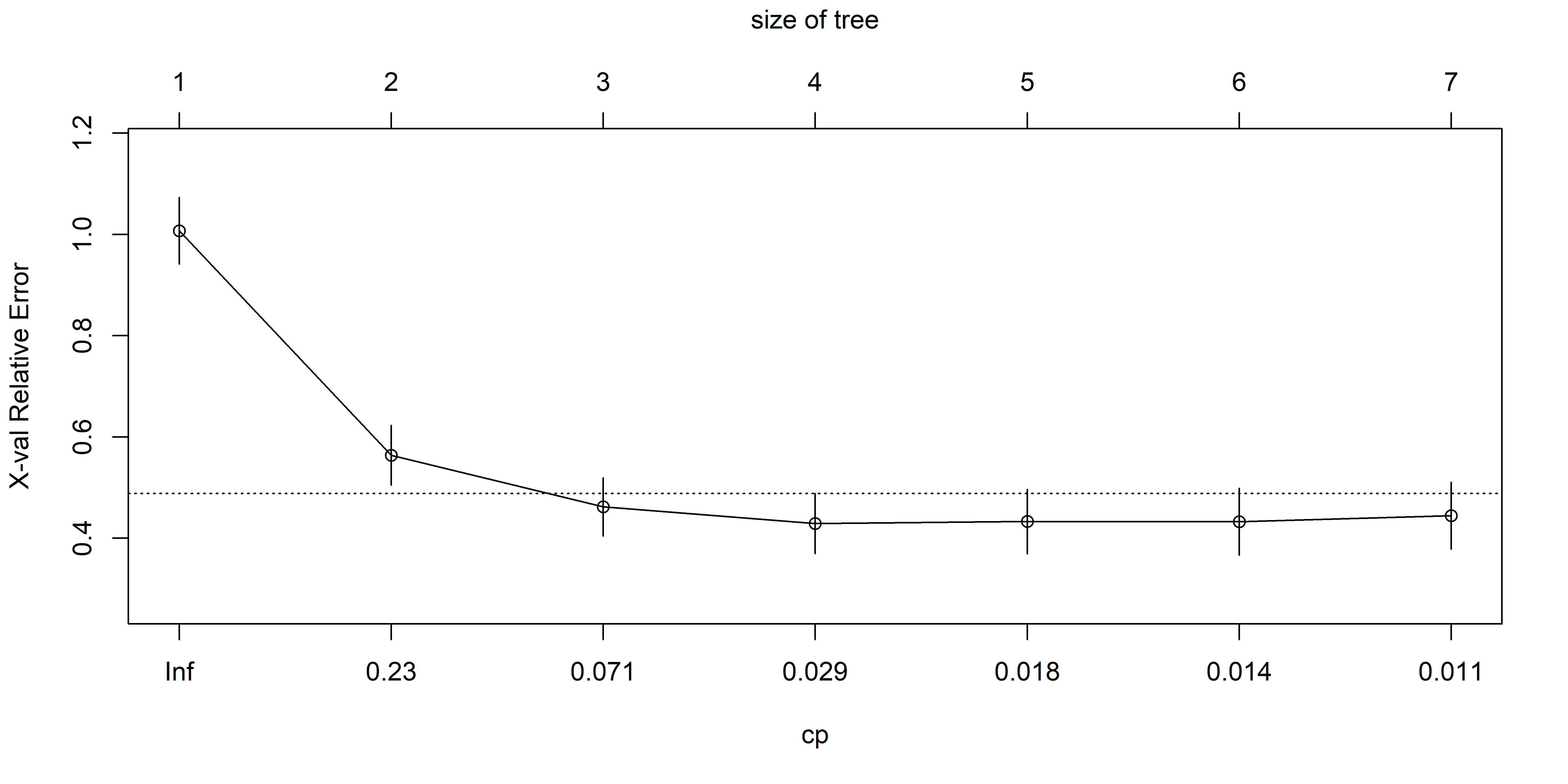

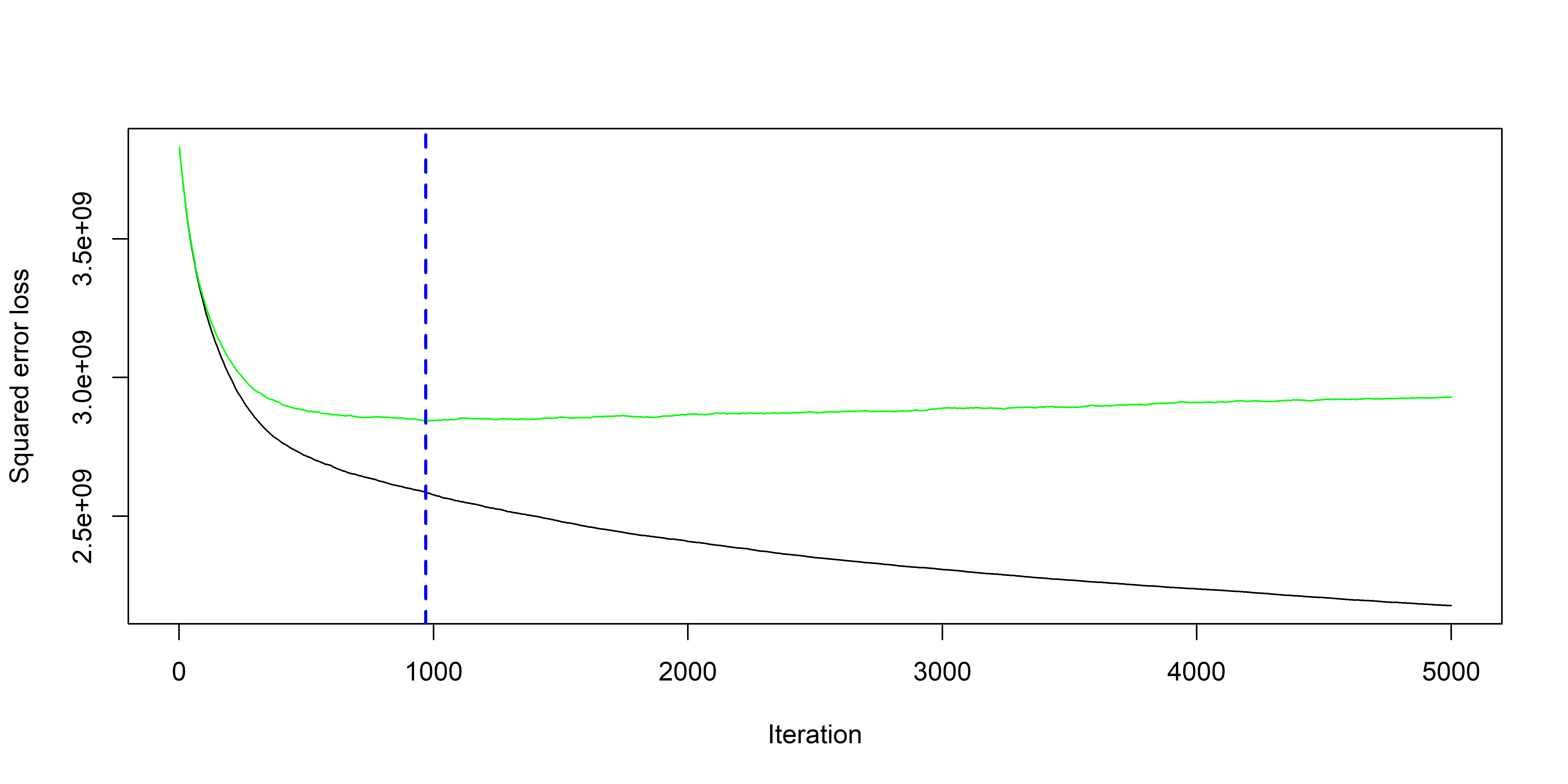

CV to pick \alpha (equiv., |T|)

The training, cross-validation, and test MSE are shown as a function of the number of terminal nodes in the pruned tree. Standard error bands are displayed. The minimum cross-validation error occurs at a tree of size three.

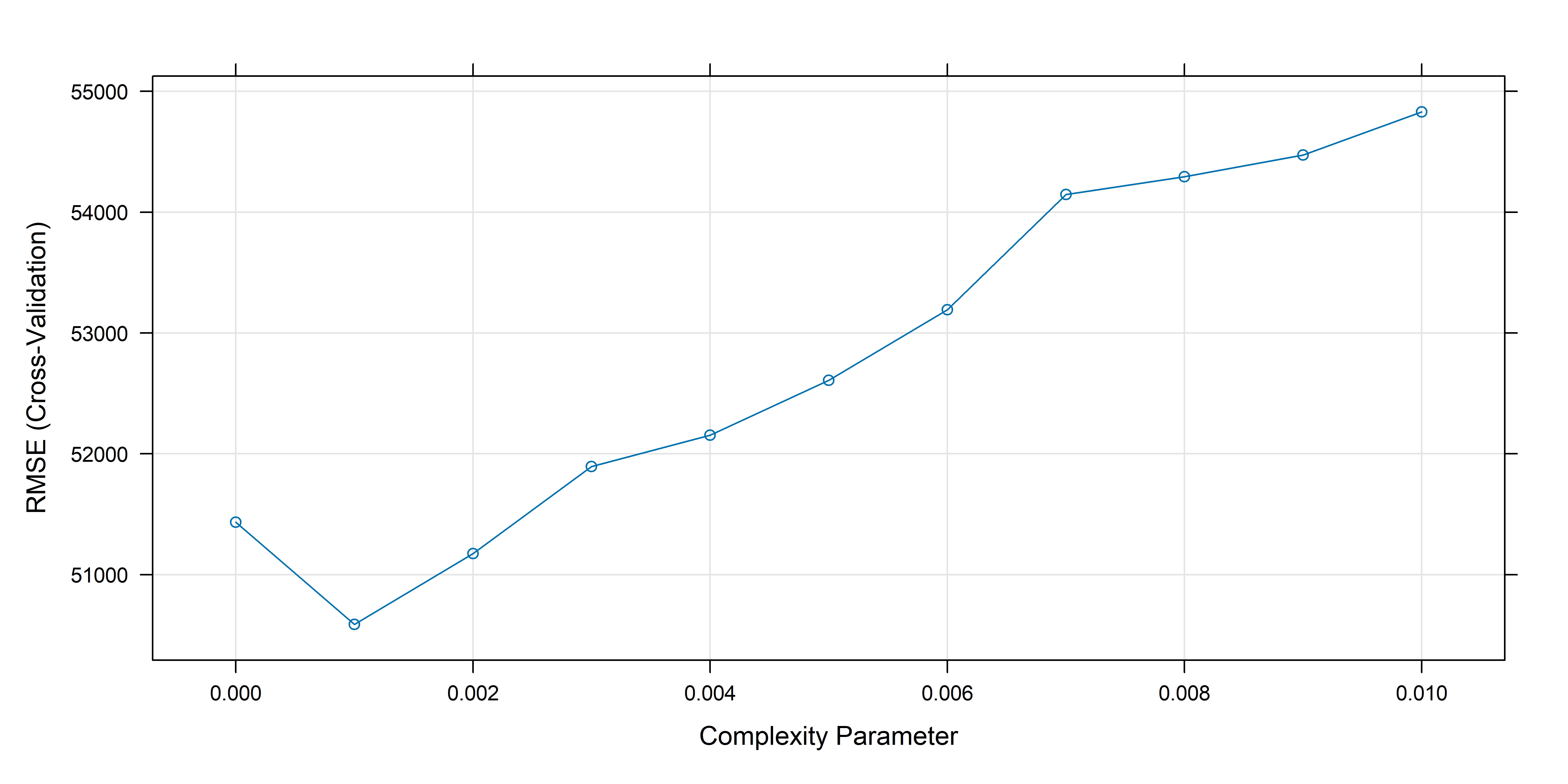

CV to prune NFIP tree

Cross-validation to prune the large NFIP tree

# Perform cross-validation to prune the tree

set.seed(123)

cv_tree <- train(

amountPaidOnBuildingClaim ~ .,

data=train_set,

method="rpart",

trControl=trainControl(method="cv", number=5),

tuneGrid=data.frame(cp=seq(0, 0.01, 0.001))

)

# Get the optimal cp value

optimal_cp <- cv_tree$bestTune$cp

plot(cv_tree)

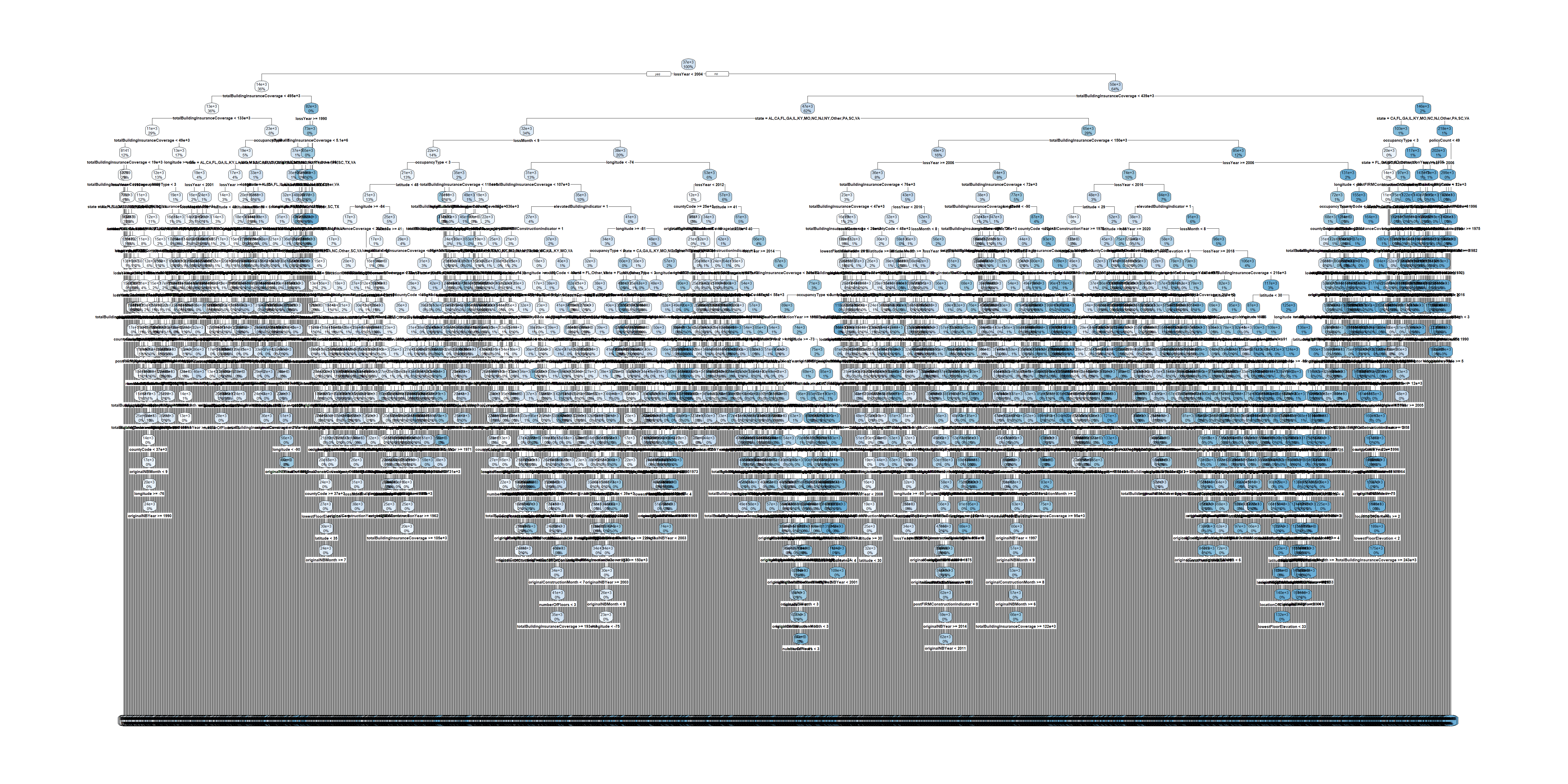

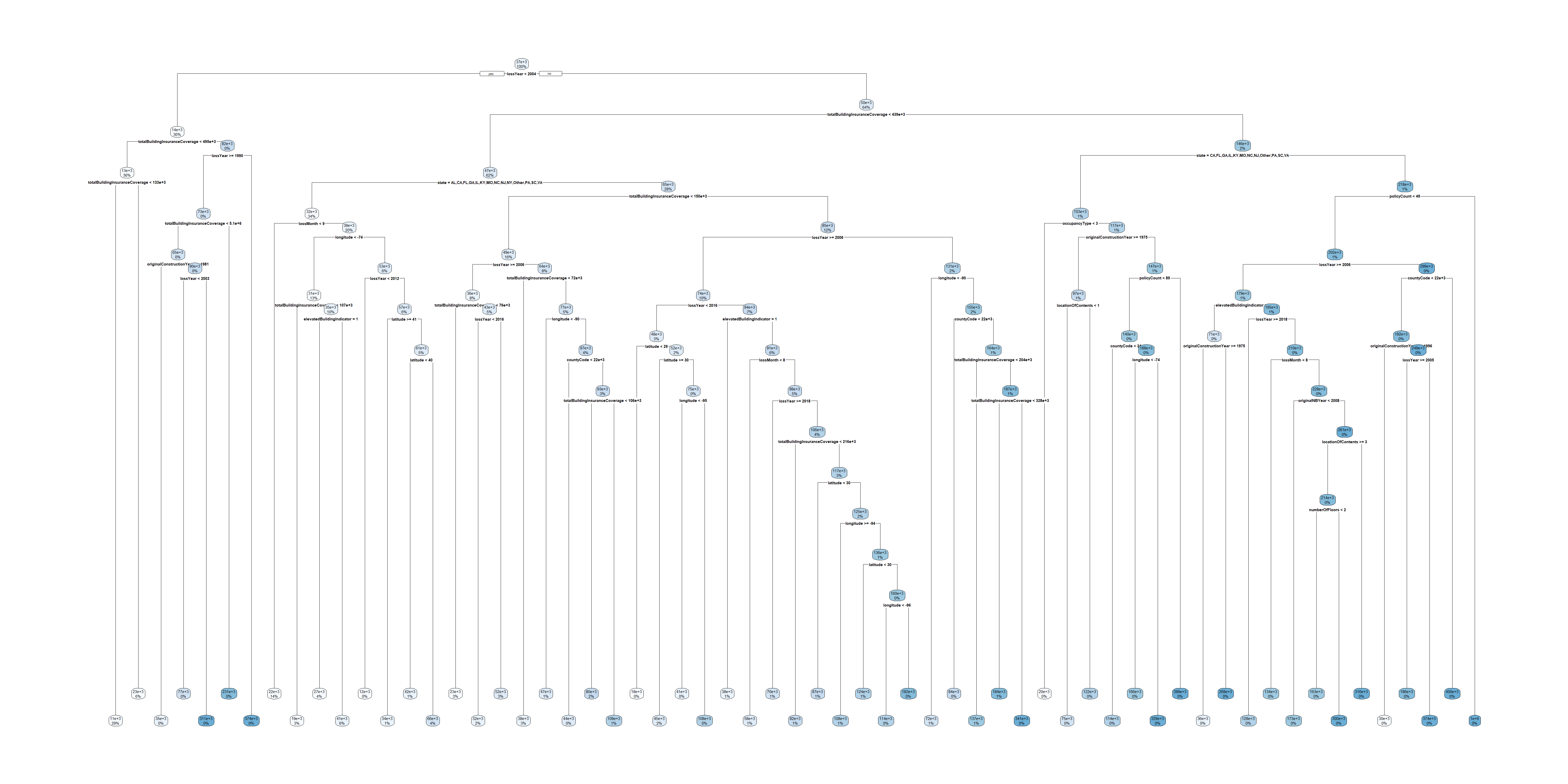

The pruned tree

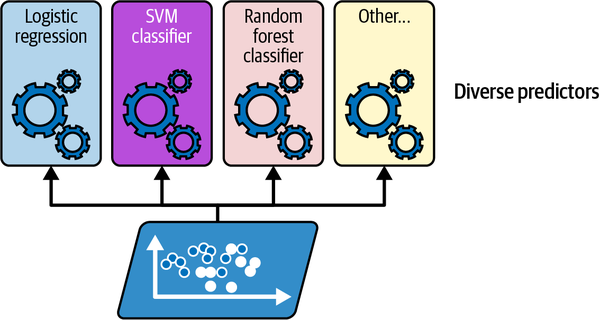

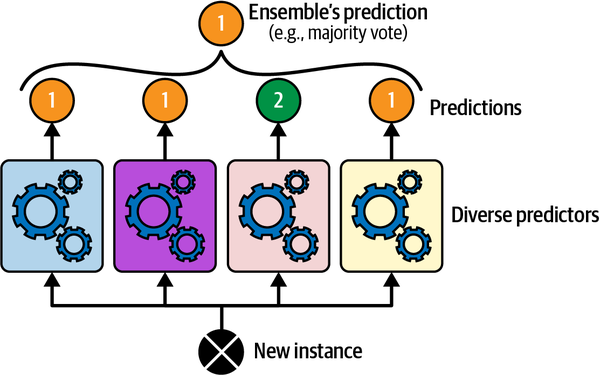

An ensemble is a group of models…

Training various different classifiers on the same dataset.

… & you combine their predictions

Make an overall prediction based on the majority vote of the models.

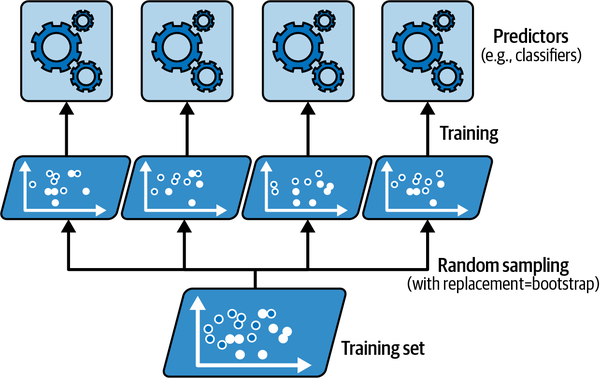

Bootstrapping

Train on different versions of the same data.

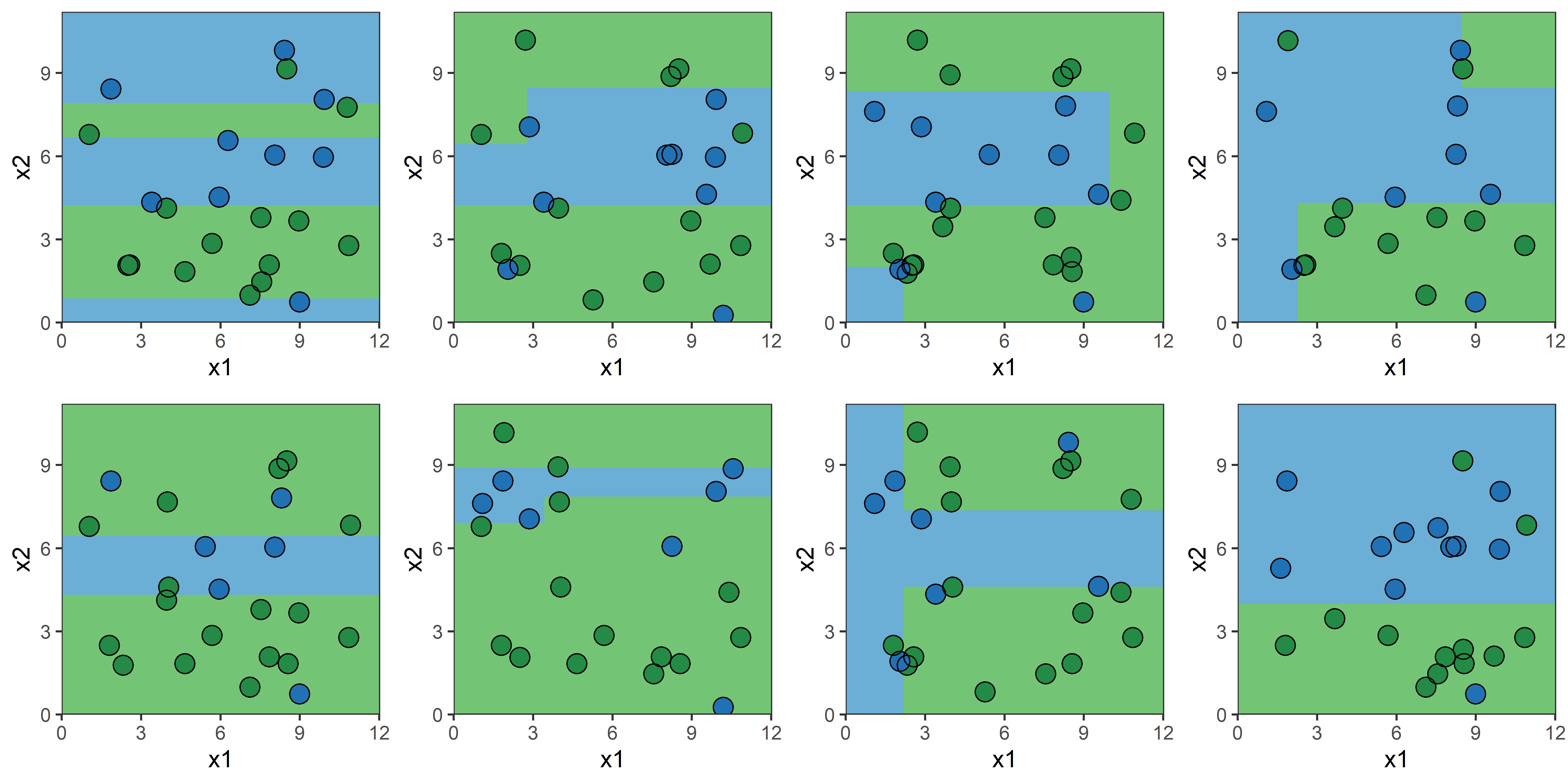

Bagging: Illustration

Bagging: Illustration

Random Forests

This is a forest (stock photo)

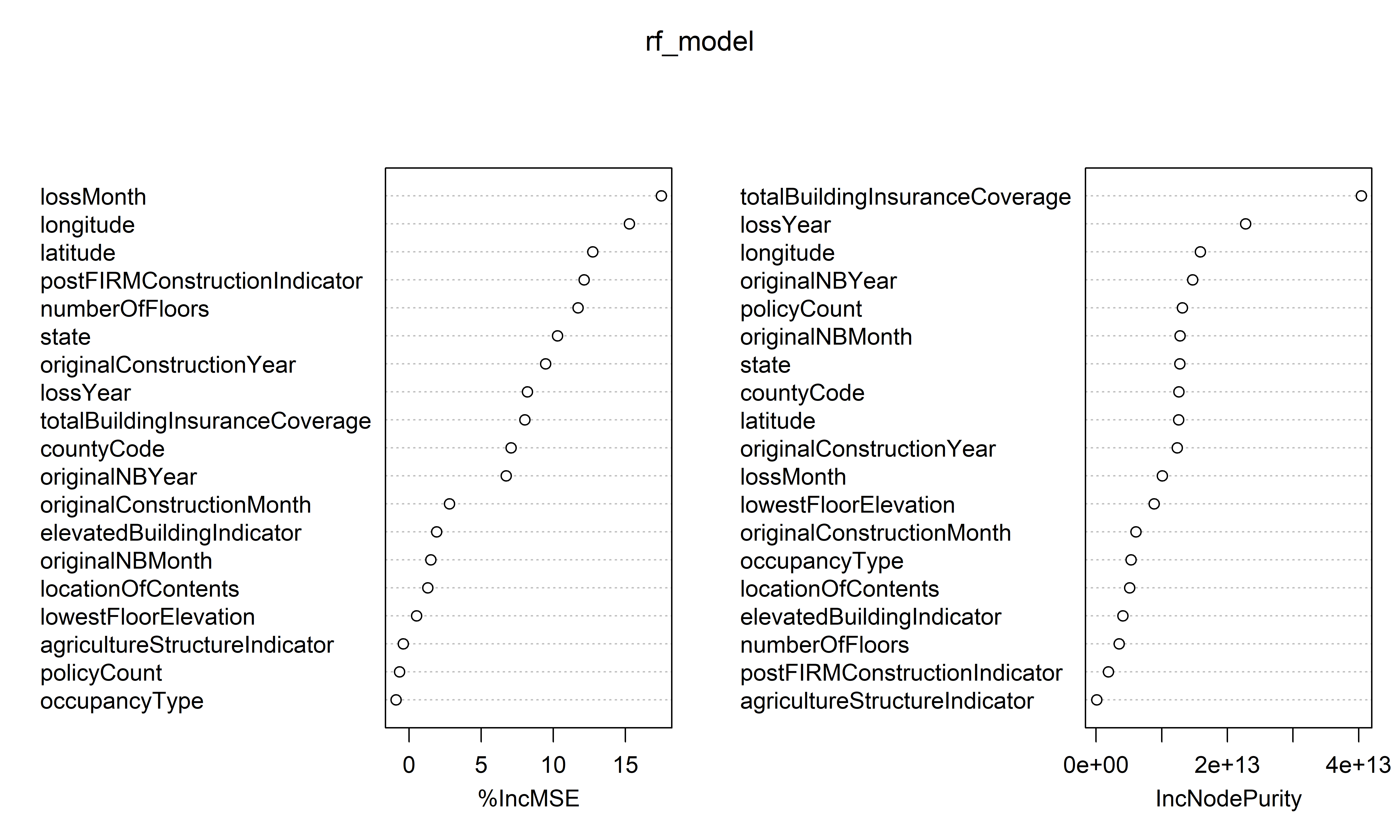

Variable importance plot

Fitting with package gbm

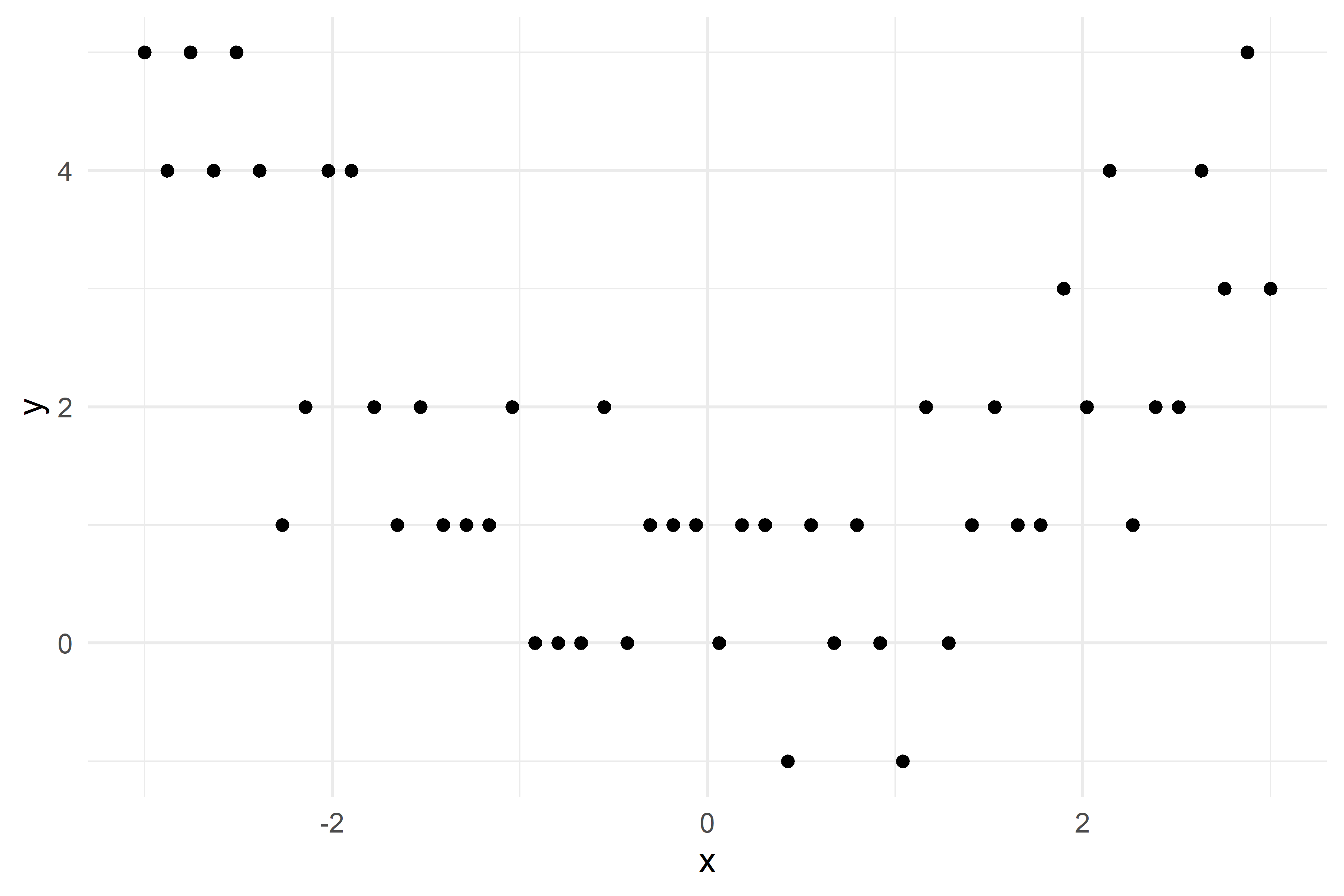

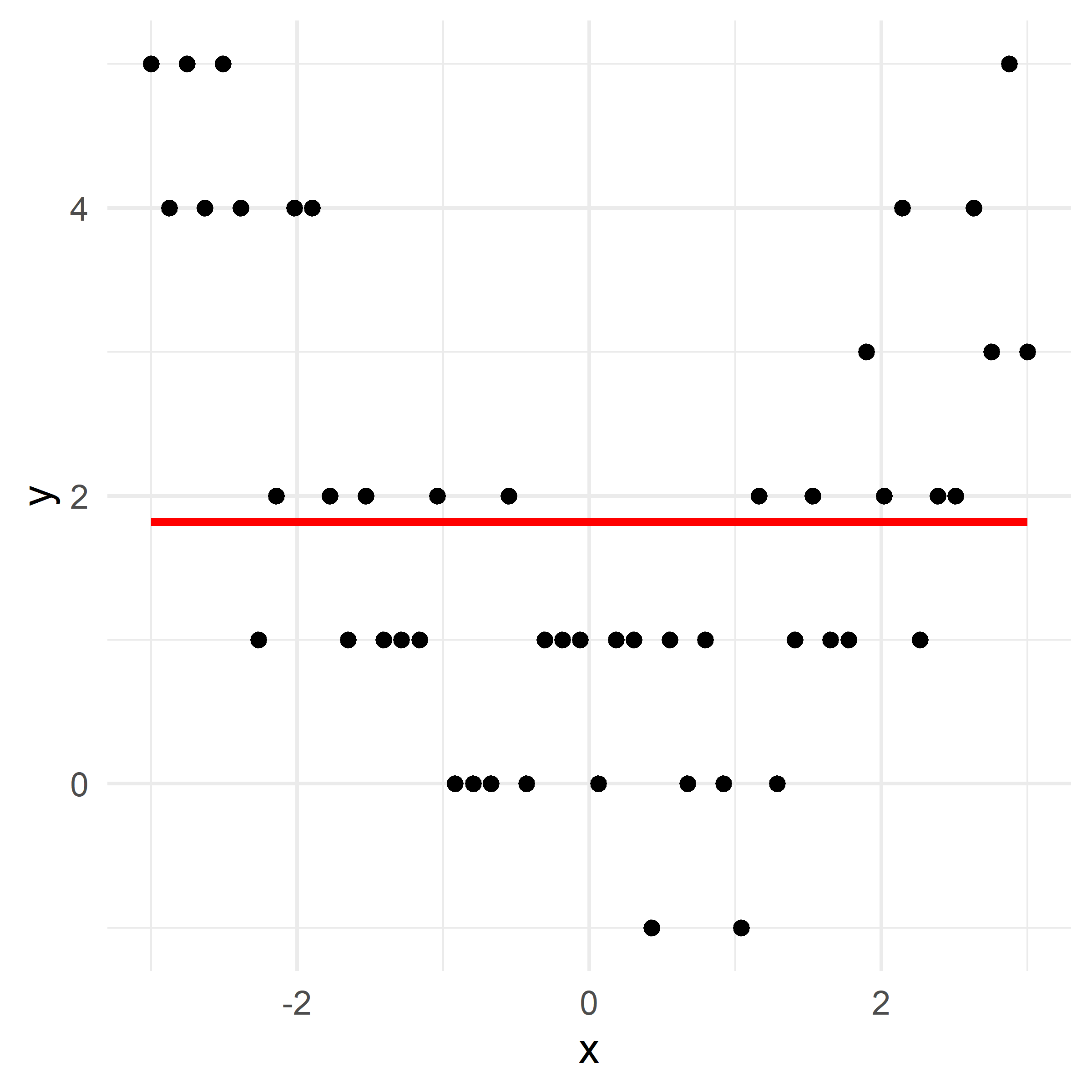

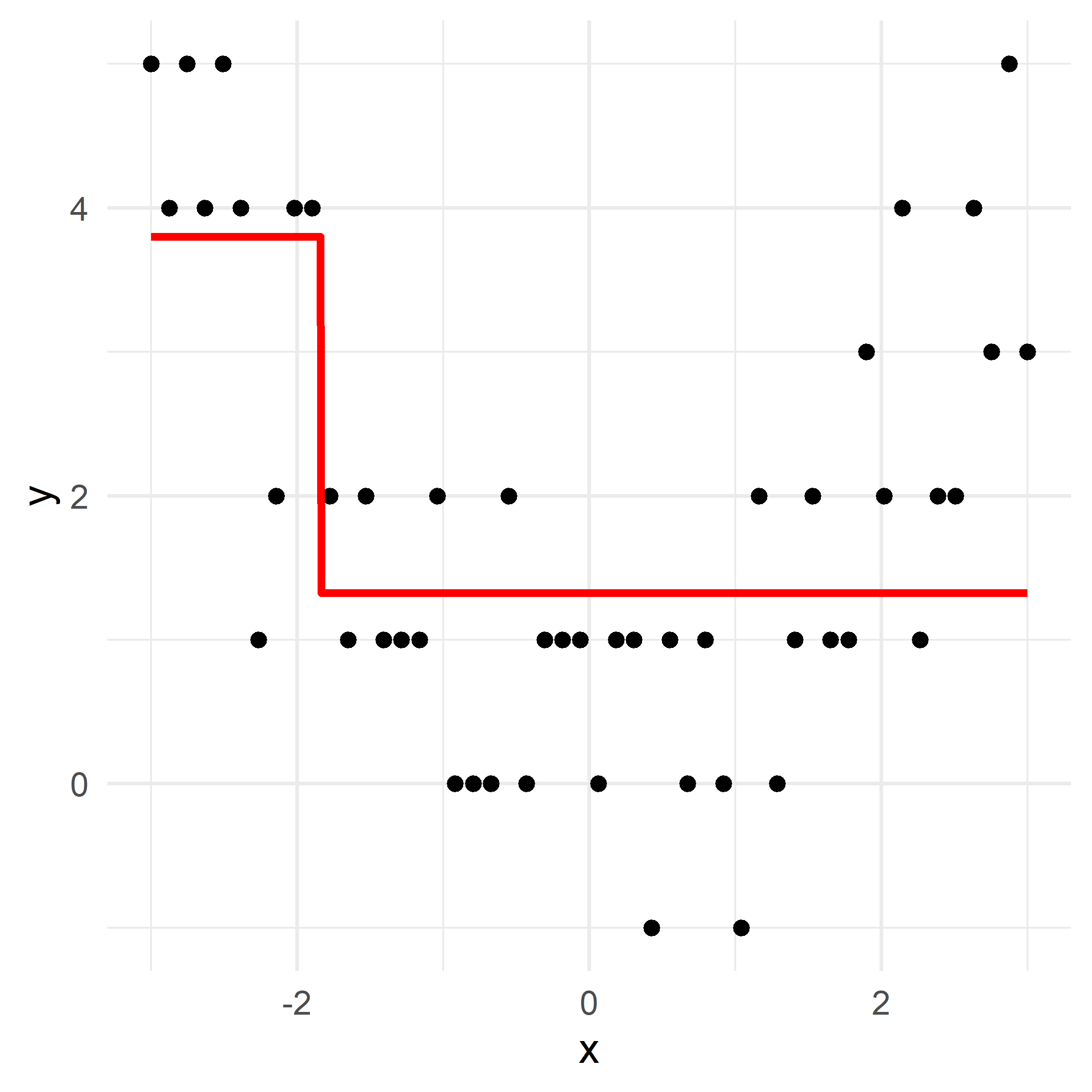

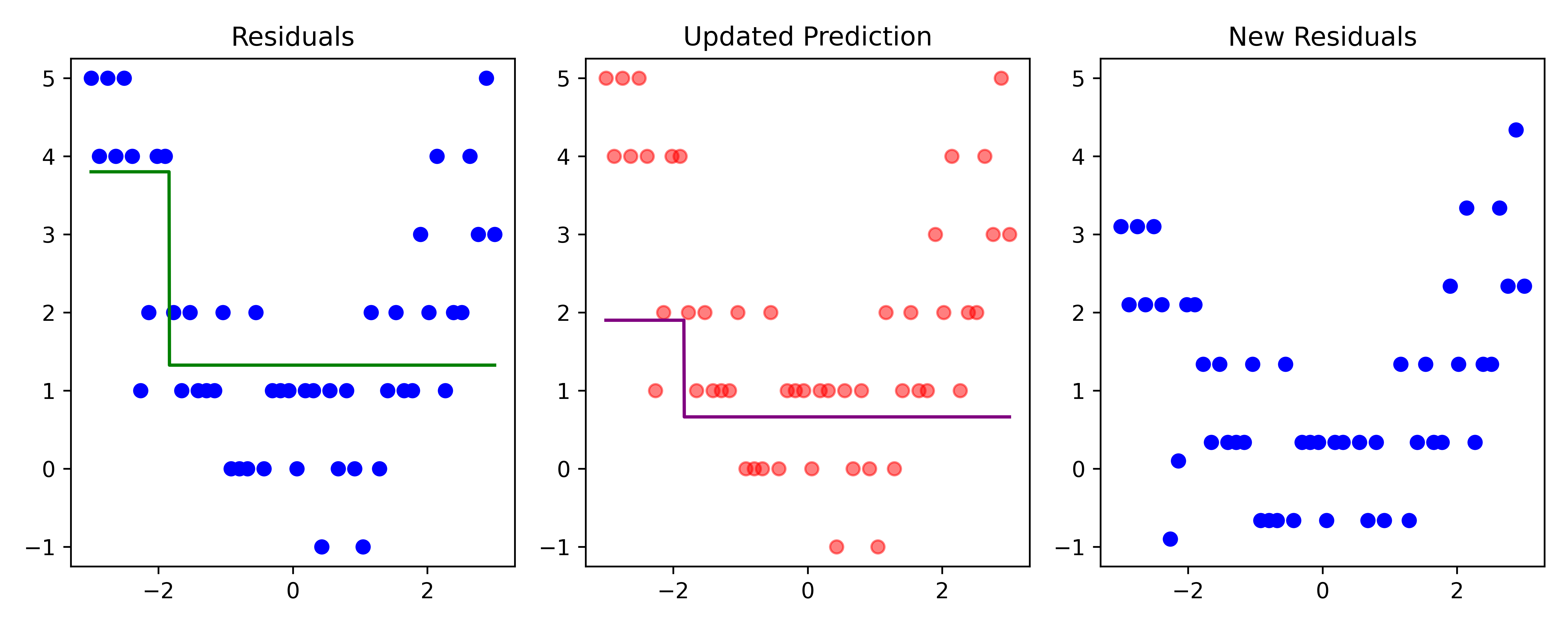

Boosting (iteration 1)

Code

x_obs = np.linspace(-3, 3, 50)

y_obs = [5, 4, 5, 4, 5, 4, 1, 2, 4, 4, 2, 1, 2, 1, 1, 1, 2, 0, 0, 0, 2, 0, 1, 1, 1, 0, 1, 1, -1, 1, 0, 1, 0, -1, 2, 0, 1, 2, 1, 1, 3, 2, 4, 1, 2, 2, 4, 3, 5, 3]

df = pd.DataFrame({'x': x_obs, 'y': y_obs})

# Parameters

d = 1 # number of splits

lambda_ = 0.5 # learning rate

# Higher resolution grid

x_obs = x_obs.reshape(-1, 1)

x_grid = np.linspace(-3, 3, 1000)

# Initial model

f_hat = np.zeros_like(df['y'], dtype=float)

residuals = df['y'].astype(float).copy()

# Store predictions for the grid

f_hat_grid = np.zeros_like(x_grid, dtype=float)

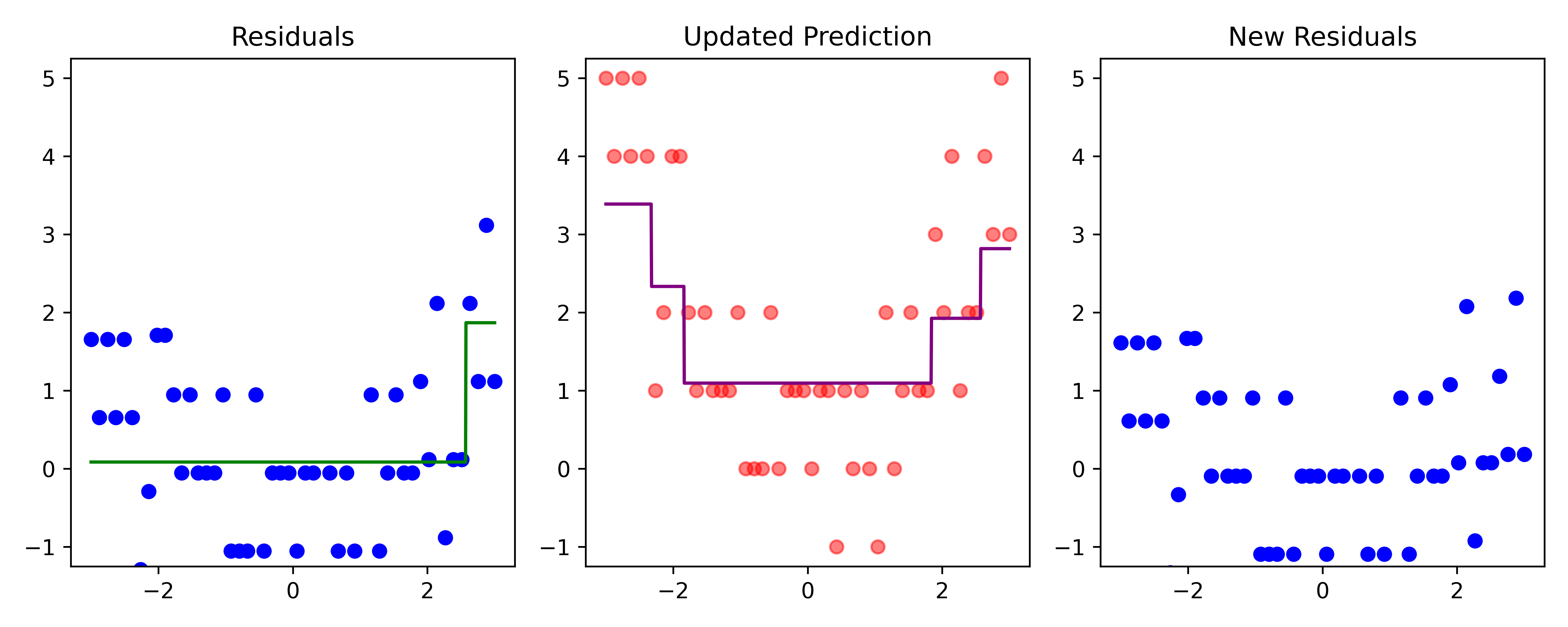

def plot_boosting_iteration(df, x_grid, f_hat, residuals, f_hat_grid, d, lambda_):

fig, axes = plt.subplots(1, 3, figsize=(10, 4))

# Plot residuals

axes[0].scatter(df['x'], residuals, color='blue', label='Residuals')

axes[0].plot(x_grid, f_b_grid, color='green', label='New Tree')

axes[0].set_ylim(-1.25, 5.25)

axes[0].set_title(f"Residuals")

# Plot updated model prediction

axes[1].plot(x_grid, f_hat_grid, color='purple')

axes[1].scatter(df['x'], df['y'], color='red', alpha=0.5)

axes[1].set_ylim(-1.25, 5.25)

axes[1].set_title(f"Updated Prediction")

# Plot new residuals

axes[2].scatter(df['x'], df['y'] - f_hat, color='blue', label='Residuals')

axes[2].set_ylim(-1.25, 5.25)

axes[2].set_title(f"New Residuals")

plt.tight_layout()Code

# Fit a tree to residuals

tree = DecisionTreeRegressor(max_depth=d)

tree.fit(x_obs, residuals);

f_b = tree.predict(x_obs)

f_b_grid = tree.predict(x_grid.reshape(-1, 1))

# Update model

f_hat += lambda_ * f_b

f_hat_grid += lambda_ * f_b_grid

plot_boosting_iteration(df, x_grid, f_hat, residuals, f_hat_grid, d, lambda_)

# Update residuals

residuals -= lambda_ * f_b

Here, \lambda=\frac12 is the learning rate.

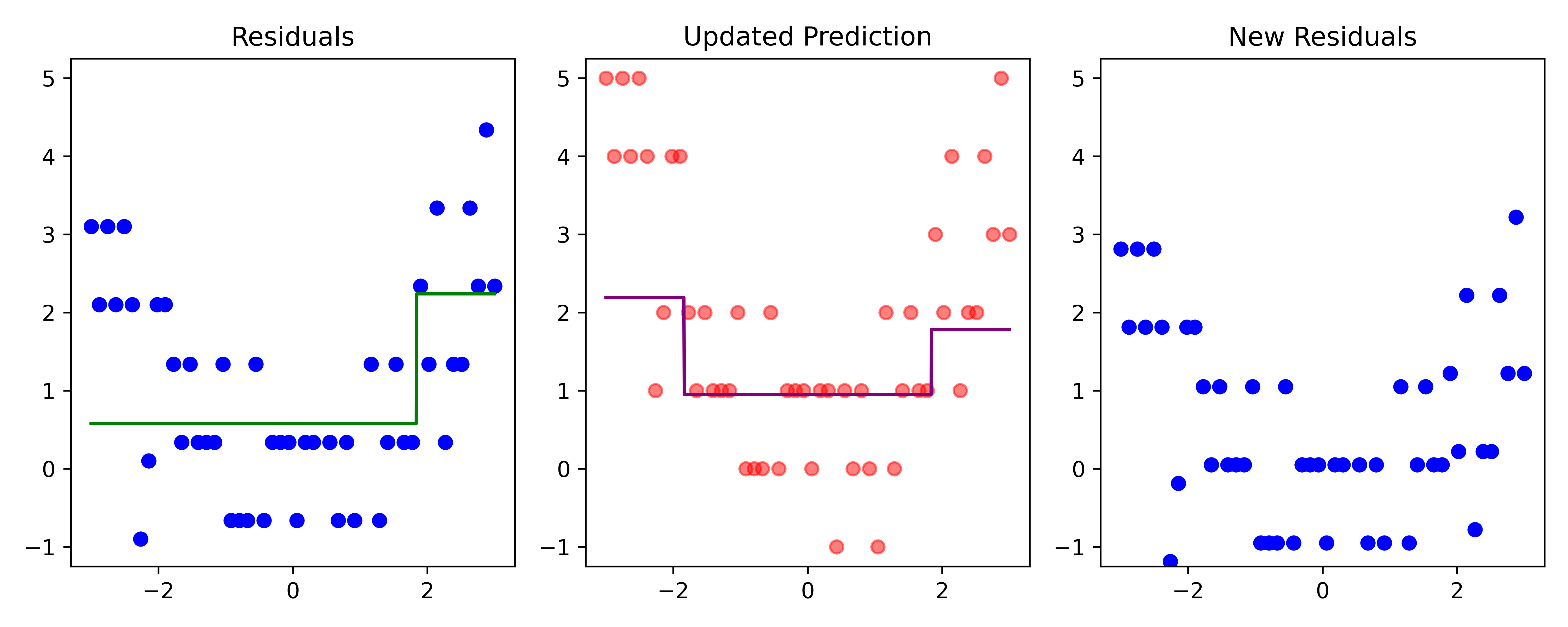

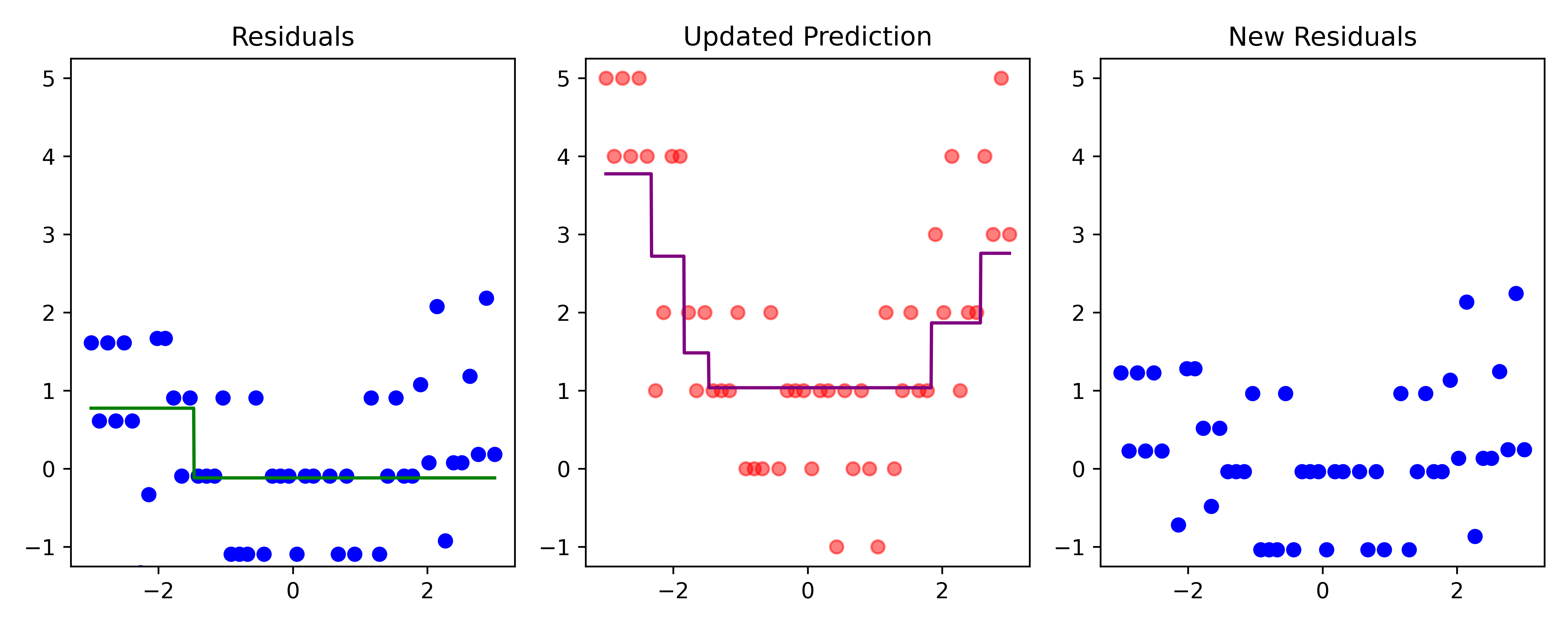

Boosting (iteration 2)

Code

# Fit a tree to residuals

tree = DecisionTreeRegressor(max_depth=d)

tree.fit(x_obs, residuals);

f_b = tree.predict(x_obs)

f_b_grid = tree.predict(x_grid.reshape(-1, 1))

# Update model

f_hat += lambda_ * f_b

f_hat_grid += lambda_ * f_b_grid

plot_boosting_iteration(df, x_grid, f_hat, residuals, f_hat_grid, d, lambda_)

# Update residuals

residuals -= lambda_ * f_b

Here, \lambda=\frac12 is the learning rate.

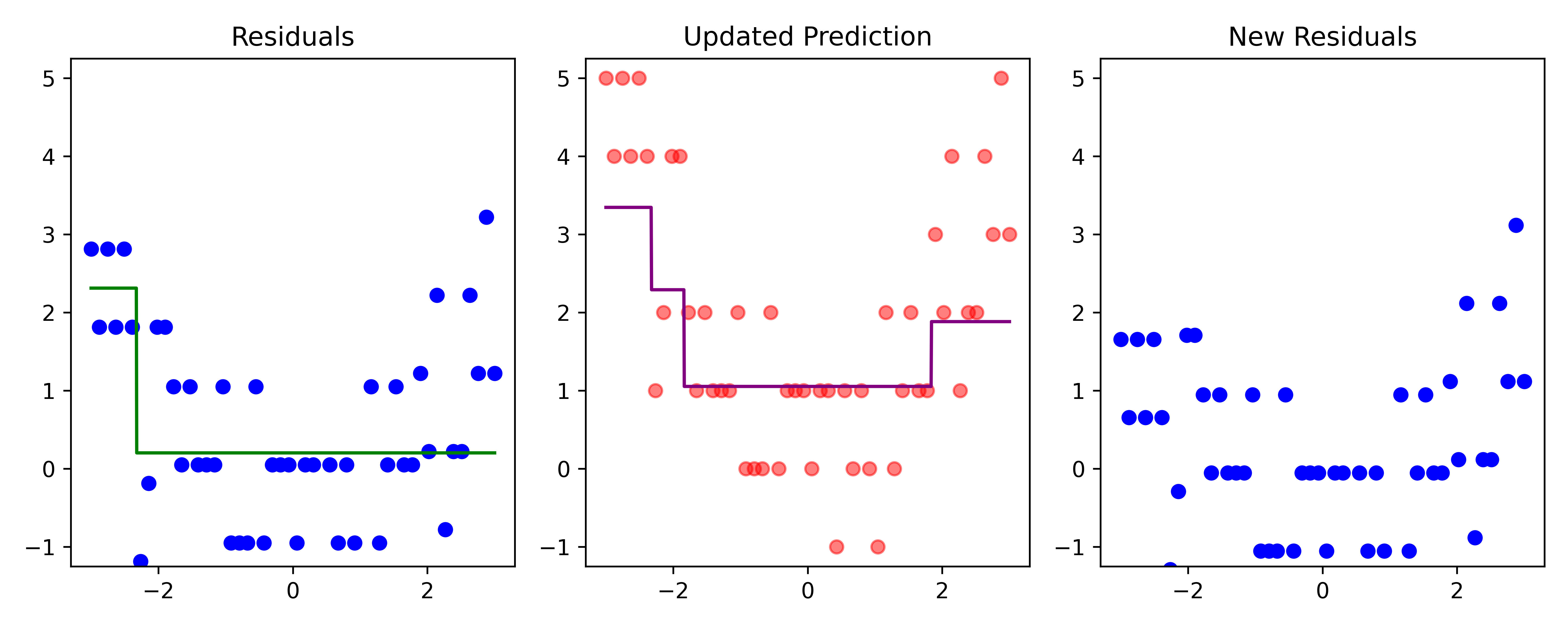

Boosting (iteration 3)

Code

# Fit a tree to residuals

tree = DecisionTreeRegressor(max_depth=d)

tree.fit(x_obs, residuals);

f_b = tree.predict(x_obs)

f_b_grid = tree.predict(x_grid.reshape(-1, 1))

# Update model

f_hat += lambda_ * f_b

f_hat_grid += lambda_ * f_b_grid

plot_boosting_iteration(df, x_grid, f_hat, residuals, f_hat_grid, d, lambda_)

# Update residuals

residuals -= lambda_ * f_b

Here, \lambda=\frac12 is the learning rate.

Boosting (iteration 4)

Code

# Fit a tree to residuals

tree = DecisionTreeRegressor(max_depth=d)

tree.fit(x_obs, residuals);

f_b = tree.predict(x_obs)

f_b_grid = tree.predict(x_grid.reshape(-1, 1))

# Update model

f_hat += lambda_ * f_b

f_hat_grid += lambda_ * f_b_grid

plot_boosting_iteration(df, x_grid, f_hat, residuals, f_hat_grid, d, lambda_)

# Update residuals

residuals -= lambda_ * f_b

Here, \lambda=\frac12 is the learning rate.

Boosting (iteration 5)

Code

# Fit a tree to residuals

tree = DecisionTreeRegressor(max_depth=d)

tree.fit(x_obs, residuals);

f_b = tree.predict(x_obs)

f_b_grid = tree.predict(x_grid.reshape(-1, 1))

# Update model

f_hat += lambda_ * f_b

f_hat_grid += lambda_ * f_b_grid

plot_boosting_iteration(df, x_grid, f_hat, residuals, f_hat_grid, d, lambda_)

# Update residuals

residuals -= lambda_ * f_b

Here, \lambda=\frac12 is the learning rate.

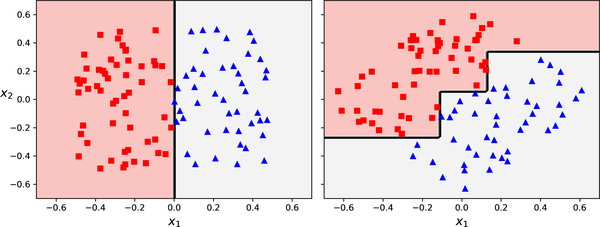

Sensitivity to training data orientation

An example of a dataset which is rotated and fit to decision trees.